Coverage Expansion

170 likes | 297 Views

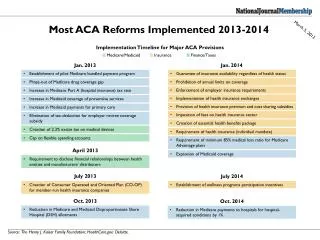

The 2013 Medicaid expansion in Michigan aimed to cover over 1.1 million uninsured residents, addressing healthcare access amidst resistance to the ACA and substantial state debt. This initiative proposed a $1.5 billion appropriation with federal waivers for design changes, requiring state leaders to navigate term limits and stakeholder engagement. The enrollment process, launching on October 1, 2013, relied on a coalition of providers and certified counselors to assist low-income individuals in obtaining coverage. Healthcare systems played a crucial role in outreach, education, and facilitating the enrollment process.

Coverage Expansion

E N D

Presentation Transcript

Coverage Expansion Laura Appel

Political setting 2013 • Term limits – more than 90 state lawmakers with ≤ 4 yrs. exp. • Medicare and Medicaid account for half of avg. hospital revenue • More than 1.1 million people uninsured in Michigan • More than 1.8 million people in Medicaid, 167,000 eligible but not enrolled and 400,000 people projected to be added in 2013

Medicaid Expansion • Why do it? • Why not do it? resistance to Obamacare, $17 trillion in debt What’s in the expansion legislation? • $1.5 billion appropriation • Waiver requirements • Personal responsibility requirements • Health plan requirements • Reduced general fund expenditure • No immediate effect

Medicaid Expansion—next steps • Spending appropriated funds contingent on waiver approval • Federal waiver for new Medicaid design including health savings account • Initiate Medicaid beneficiary enrollment program • Expand Medicaidcoalition to assist with enrollment process • Effective date of HB 4714: end of first quarter 2014 • Enrollment/eligibility for new Medicaid population is dependent on waiver approval

The Insurance Mall (online) • Health Insurance Marketplace opened October 1 for enrollment • 12 insurers offering products online • Variety of plans—162 in Michigan • Variety of premiums—depends on plan selected • Variety of subsidies—depends on income • Coverage begins January 1, 2014

Coverage • Single application for all • No denial for pre-existing conditions • Insurers must cover a minimum set of services called essential health benefits • Must organize their plan offerings into five levels of patient cost-sharing from least to most protective • Catastrophic for those 30 and under • Bronze • Silver • Gold • Platinum

Example Most enrollees will pay a lower monthly premium than the unsubsidized rates presented above. For example, a 40-year-old with an income of 250 percent of the federal poverty level (roughly $29,000 per year) would pay about 8 percent of his or her income or $193 per month to enroll in the second-lowest-cost silver plan, regardless of the rating area.

Who can receive a subsidy? • Anyone with income between 100 and 400 percent of the federal poverty level • People with incomes between 100 and 133 percent of the FPL may choose between a product on the exchange (insurance mall) or a Medicaid managed care plan • Plans available through Medicaid are likely to be lower cost—co-pays, deductibles and premiums will apply to some Medicaid enrollees

Michigan Qualified Plans Filed for Health Insurance Exchange

Premium information available at DIFS http://www.michigan.gov/difs/0,5269,7-303-12902_35510_66707-313356--,00.html#noprint

Outreach and Enrollment • Medicaid expansion + Subsidy-eligible population = More than 1 million people • Health literacy among public is low • Many are lower income workers who need assistance applying for coverage • Exchange opened Oct. 1, continues through March 31, 2014 • Coverage begins at different times

Who is Helping People Apply? • Insurance agents • Navigators • DHS • Certified Application Counselors (CACs): voluntary, 5+ hours training (all online) • Who can be CACs? Hospitals, health centers, community-based organizations, physician offices, volunteers • http://www.getcoveredamerica.org/page/event/search_simple • www.enrollmichigan.com • www.michigan.gov/hicap

Available Role for Providers • Opportunity to significantly decrease the number of uninsured people • Fewer uncompensated ER visits • Greater ability to connect people with preventive care • Maintain healthy population/productive workforce • Hospitals are an obvious place to go for help; recommend preparing hospital staff to educate and assist • Physician offices, FQHCs, free clinics—all trusted voices of care for those seeking coverage

How health systems are engaging in enrollment • Certified Application Counselors • Patient financial services staff, volunteer leadership, patient advocates • Engaging trustees, volunteers and staff regarding the basics of coverage expansion • Educating patients • May conduct local outreach using detailed databases available from Enroll America—Michigan chapter

What MHA is Doing • MHA tools for hospitals • FAQs • Outreach methods • CAC guidance • Sample news release, flyer • Flowchart of uninsured person’s options • Website links • www.mha.org

Presumptive Eligibility • ACA allows hospitals to determine presumptive eligibility for all Medicaid-eligible populations (including the expansion population) starting Jan. 1, 2014 • Hospitals must move forward with these expanded determinations in compliance with state-issued policies and procedures • A proposed policy issued by the state late this summer did not reflect these expanded privileges for hospitals • This weekthe Department of Community Health provided informal notice to the MHA that this expansion of presumptive eligibility privilege for hospitals will not take effect until June 2014