Download

1 / 18

280 likes | 699 Views

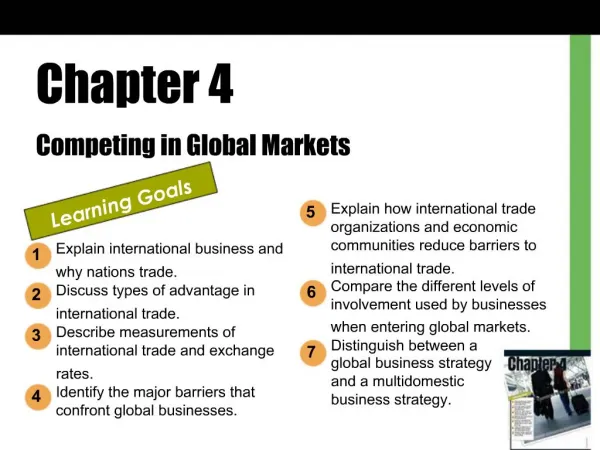

Chapter 4 Competing in Global Markets. Learning Goals. Explain how international trade organizations and economic communities reduce barriers to international trade. Compare the different levels of involvement used by businesses when entering global markets.

E N D

Chapter 4 Competing in Global Markets Learning Goals Explain how international trade organizations and economic communities reduce barriers to international trade. Compare the different levels of involvement used by businesses when entering global markets. Distinguish between a global business strategy and a multidomestic business strategy. 5 Explain international business and why nations trade. Discuss types of advantage in international trade. Describe measurements of international trade and exchange rates. Identify the major barriers that confront global businesses. 1 6 2 3 7 4

ExportsDomestically produced goods and services sold in markets in other countries. • ImportsForeign-made products and services purchased by domestic consumers. • WHY NATIONS TRADE • • Boosts economic growth by providing access to new markets and needed resources. • • More efficient production systems. • • Less reliance on economies of home nations.

International Sources of Factors of Production • • Decisions to operate abroad depend on availability, price, and quality of • • Labor • • Natural resources • • Capital • • Entrepreneurship • • Allows a company to spread risk throughout nations in different stages of the business cycle or development.

Size of the International Marketplace • • World population = 7 billion • • One in five people live in relatively well-developed countries. • • Share of world’s population in less-developed countries will grow in coming years. • • Population size is no guarantee of prosperity. • • Though developing nations generally have lower per capita income, many have strong GDP growth rates and their huge populations can be lucrative markets.

Absolute and Comparative Advantage • • Absolute advantage Country can maintain a monopoly or produce at a lower cost than any competitor. • • Example: China’s domination of silk production for centuries. • • Rare these days, mostly tied to climate advantages for growing certain crops. • • Comparative advantage Country can supply a product more efficiently and at lower cost than it can supply other goods, compared with other countries. • • Example: India’s combination of a highly educated workforce and low wage scale.

MEASURING TRADE BETWEEN NATIONS • Balance of tradeDifference between a nation’s imports and exports. • Balance of paymentsOverall flow of money into or out of a country. • Major U.S. Exports and Imports • • U.S. leads world, exports and imports annually total $3 trillion. • • U.S. imports more goods than exports; exports more services than imports.

Exchange Rates • Exchange rateValue of one nation’s currency relative to the currencies of other nations. • • Values fluctuate, or “float,” depending on supply and demand for each currency in the international market. • • National governments deliberately influence exchange rates • • Business transactions usually conducted in currency of the region where they happen. • • Rates can quickly create or wipe out competitive advantage. • • Hard currencies Currencies that owners can easily convert into other currencies. • • Foreign currency market is world’s biggest, with daily volume of $1.5 trillion, 50 times the size of all equity markets put together.

BARRIERS TO INTERNATIONAL TRADE • Social and Cultural Differences • Language Potential problems include mistranslation, inappropriate messaging, lack of understanding of local customs and differences in taste. • Values and Religious Attitudes Differing values about business efficiency, employment levels, importance of regional differences, and religious practices, holidays, and values about issues such as interest-bearing loans.

Economic Differences • Infrastructure Basic systems of communication, transportation, energy facilities, and financial systems. • Currency Conversion and Shifts Fluctuating values can make pricing in local currencies difficult and affect decisions about market desirability and investment opportunities. • Political and Legal Differences • Political Climate Stability is a key consideration. • Legal Environment Three dimensions: U.S. law, international regulations, laws of the countries where they plan to trade. Corruption can be an important issue. • International RegulationsFriendship, commerce, and navigation treaties between U.S. and other nations.

Types of Trade Restrictions • Tariffs Taxes, surcharges, or duties on foreign products. • • Revenue tariffs generate income for the government. • • Protective tariffs raise prices of imported goods to level the playing field for domestic competitors. • Nontariff Barriers Also called administrative trade barriers • • Quotas limit the amount of a product that can be imported over a specified time period. • • An embargo imposes a total ban on importing a specified product or all trading with a particular country. • • Exchange controls through central banks or government agencies regulate the buying and selling of currency to shape foreign exchange in accordance with national policy.

REDUCING BARRIERS TO INTERNATIONAL TRADE • Organizations Promoting International Trade • • General Agreement on Tariffs and Trade (GATT) sponsored negotiations to reduce worldwide barriers to trade. • • Founded 1947 • • Uruguay Round of negotiations cut average tariffs by one-third, or $700 billion. • • Led to the establishment of the World Trade Organization.

World Trade Organization Monitors GATT agreements. • • 149 member countries • • Began monitoring GATT agreements in 1995 • World Bank Lends money to less-developed and developing countries. • • Funds projects that build or expand infrastructure. • • Provides assistance and advice. • International Monetary Fund Promotes trade through financial cooperation. • • Makes short-term loans to member nations to meet expenses. • • Operates as lender of last resort for troubled nations.

International Economic Communities • • Reduce trade barriers and promote regional economic cooperation. • • Free-trade area Members trade freely among selves without tariffs or trade restrictions. • • Customs union Establishes a uniform tariff structure for members’ trade with nonmembers. • • Common market Members bring all trade rules into agreement. • NAFTA (1994) • • World’s largest free-trade zone: United States, Canada, Mexico. • • Combined population: 435 million • • Total GDP: nearly $14 trillion • • U.S. and Canada are each other’s biggest trading partners.

CAFTA (2005) • • Free-trade zone among United States, Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras, and Nicaragua. • • Total GDP: nearly $14 trillion • • $33 billion traded annually between U.S. and these countries. • European Union • • Best-known example of a common market. • • Combined population: 450 million people in 25 countries • • Total GDP: $12 trillion • • Goals include promoting economic and social progress, introducing European citizenship as complement to national citizenship, and giving EU a significant role in international affairs.

GOING GLOBAL • • Three key decisions for companies considering going global: • • What foreign market(s) will the company enter? • • What expenditures are required to enter a new market? • • What is the best way to organize overseas operations? • Levels of Involvement • Importers and Exporters Most basic level of international involvement, with the least risk and control. • Countertrade Payments made in the form of local products, not currency.

Contractual Agreements Often come after a company has some experience in international sales. Include franchising, foreign licensing, and subcontracting. • Franchising Contractual agreement in which a wholesaler or a retailer gains the right to sell the franchisors’ products under that companies brand name in exchange for agreeing to related operating requirements. • Offshoring Relocation of business processes to lower-cost location overseas. • International Direct Investment Includes establishment of manufacturing facilities, opening of an overseas division, and acquisition of an existing firm in the host country. • • Joint ventures Allow companies to share risks, costs, profits, and management responsibility with one or more host country nationals.

From Multinational Corporation to Global Business • Multinational corporation (MNC)An organization with significant foreign operations and marketing activities outside its home country.

DEVELOPING A STRATEGY FOR INTERNATIONAL BUSINESS • Global Business Strategies • • Firm sells same product in essentially the same manner throughout the world. • • Works well for products with nearly universal appeal and luxury items. • Multidomestic Business Strategies • • Firm develops products and marketing strategies that appeal to customs, tastes, and buying habits of particular national markets. • • Example: Spinach, egg, and tomato soup on the menu in KFC’s menu in China.