Download

1 / 31

320 likes | 473 Views

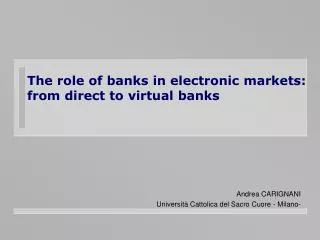

The role of banks in electronic markets: from direct to virtual banks. Andrea CARIGNANI Università Cattolica del Sacro Cuore - Milano-. BATCH. REAL TIME. PC revolution. ?. Late 50’s. Mid 80’s. Today. early 70’s. mid 80’s. early 90’s. A management perspective of the IT evolution.

E N D

The role of banks in electronic markets: from direct to virtual banks Andrea CARIGNANI Università Cattolica del Sacro Cuore - Milano-

BATCH REAL TIME PC revolution ? Late 50’s Mid 80’s Today early 70’s mid 80’s early 90’s A management perspective of the IT evolution Early 70’s

Today BACK END FRONT END CUSTOMER IT IT

IT IT IT IT IT L’impatto dell’IT in banca oggi (2) BACK END FRONT END CUSTOMER IT IT BACK END FRONT END CUSTOMER IT IT

• Internet • PC • Telefono • Smart Card • Sportelli leggeri • ATM • Televisione interattiva • Sportello tradizionale • Screen Phone Source: Booz - Allen Hamilton: Internet Banking Survey I canali distributivi della banca nei prossimi dieci anni

Internet Banking: una contraddizione? Fonte: BlueskyInc

PC vs. Internet banking Client software Standard browser Modem Modem Internet BANCA Server software

PC vs. Internet Il software utilizzato dal cliente è creato, distribuito e aggiornato dal broker o da una società di servizi ad essa collegata. Il software utilizzato dal cliente è un normale browser di navigazione (Netscape, Internet Explorer, etc.). La connessione avviene via linea telefonica e i costi di comunicazioni sono correlati alla distanza tra banca e cliente. La capillarità di Internet permette al cliente di collegarsi alla propria banca da qualsiasi parte del mondo con una spesa limitata. Il software proprietario e il collegamento diretto sono strumenti per la fidelizzazione del cliente: essi rappresentano una sorta di "barriera tecnologica" verso il "mercato perfetto" reso possibile da Internet. L'utente di Internet controlla con facilità l'andamento dell'offerta del mercato e teoricamente può, con un click, sostituire la banca che non soddisfa le sue esigenze.

Internet Provider Firewall Intranet della banca Internet Business Server L’architettura dell’Internet banking Cliente Internet Modem Internet Provider Front end di comunicazione Sistema proprietario

Migration paths toward direct banking counselling bank • Differenciation • different target markets • different products • different market strategies • different corporate cultures • Integration • all-encompassing target markets • shared distribution channels • uniform marketing strategy branch bank direct bank direct bank counselling bank

The private banks in Germany decided to spin off standalone direct banks Deutsche Bank HypoVereinsbank Dresdner Bank Commerzbank New Strategy! Reintegration of Bank24 and branch banking Cost Leadership as full service provider Discount Brokerage Service orientation, Quality leadership among direct banks Discount Brokerage

Deutsche Bank 24: Sei canali-una sola banca 1450 filiali Internet/ Online banking Phone banking 250 “isole” finanziarie 1800 ATM intelligenti 6000 cash dispenser 400 promotori finanziari Fonte: Deutsche Bank AG 3/99

Hamburgische Landesbank Securities Clearing & Settlement : : Back Office/Callcenter : Informationssysteme Beratungs & Betriebsgesellschaft (IBB) Mainframe Overflow Call Center : : : : Eurocom Postal Services : Headoffice Central Callcenter GZS Credit Cards Transactions Bankverlag Print Forms Advance BankCooperations, Outsourcing Networking of Advance Bank • Extensive Outsourcing • Advance Bank retains the customer interface • Separation of distribution/counselling and production of services • Concentration on core competencies • Innovative and extensive use of IT • Long lasting network relationships • Service Level Agreements (close to market mechanisms) Hamburg Wilhelmshaven Duisburg Frankfurt Schweinfurt München

Direct vs. Virtual Banks: A German Definition Direct Banks Financial Institutions that solely rely on electronic distribution channels for the contact with their customers (inbound and outbound), hence abstain from using branches Telephone/Call Center Mobile/SMS/Call Center PC/Internet Fax

Scientific definition of the virtual enterprise Virtual Enterprise “CONGLOMERATE OF LOOSELY COUPLED AUTONOMOUS COMPANIES (PARTNERS), WHICH, IN GENERAL, ARE RELATED TOGETHER BY BILATERAL OR MULTILATERAL CONTRACTS”

1. Focalizzazione sul mercato di massa: sfruttamento dei vantaggi di costo ottenibili attraverso i canali alternativi per offrire una ampia gamma di servizi finanziari. 2. Focalizzazione su nicchie di mercato (es. online brokerage) 3. Focalizzazione su qualità e servizi: orientamento a consulenza e servizi a valore aggiunto Essere un operatore già affermato Le dimensioni sono fondamentali per realizzare economie di scala Rischio di dover affrontare un accesa “guerra dei prezzi” Essere un operatore già affermato Le dimensioni sono fondamentali per realizzare economie di scala Rischio di dover affrontare un accesa “guerra dei prezzi” Necessari grossi investimenti per l’affermazione del brand Il concetto di banca di qualità non è ancora riconosciuto dalla clientela Offerta di prodotti e servizi di alta qualità attraverso canali alternativi a prezzi più alti della banca tradizionale Le banche tedesche e le strategie per la differenziazione Strategia Aspetti chiave

Italy and Germany on the net Web presence Interactive sites Internet banking Dynamic pages integrated with bank IS Static pages Dynamic pages General information on the bank products and services Interaction between baking and customers through mail and scripts Transaction services

La banca diretta in Italia:principali tendenze • Molti gruppi hanno optato per integrare i canali alternativi nella struttura distributiva tradizionale (multicanalità) • In pochi casi si è optato per una vera e propria differenziazione • Molto più spesso ci si è orientati verso una semplice affermazione del brand • Il trading online sta mobilitando molte realtà • Fino ad ora pochissime esperienze e iniziative orientate al Commercio Elettronico

Quale modello per la multicanalità? Canali come centri di profitto PC/Internet PC/Internet Multicanalità Telephone/Call Center Telephone/Call Center Mobile/SMS/Call Center Mobile/SMS/Call Center Fax Fax Canali complementari

The theoretical model External Customer relationships Virtual Cooperation Customer relationships Virtual Cooperation subject involved in banking activities Internal Relationships Products diversification Internal Relationships Products diversification Internal Static Dynamic approach to market and products

Emergence Traditional Batch Real-time of the Virtual Bank Bank External Customer relationships Virtual Cooperation Customer relationships Virtual Cooperation subject involved in banking activities Products diversification Products diversification Traditional Bank Orientation internal relationships Issue • Mainframes management • Communications between branches and central databases • ............................................... IT • Client/Server architectures • Intranet • E-messaging..... Internal • ......................... approach to market and products Dynamic Static The “traditional bank”

The “virtual bank” age The Virtual Traditional Batch Real-time Bank age Bank Virtual Bank Virtual Bank Orientation customer relationships External Issue • Cost reduction Virtual Cooperation • Improved services Virtual Cooperation • Identifying vendor alternatives • ............................................... IT • Internet subject involved • ISDN in banking • GSM activities • ......................... Products diversification Products diversification Traditional Bank Traditional Bank Internal approach to Dynamic Static market and products

Virtual Bank Traditional Virtual Bank maturiy Bank age Virtual Cooperation subject Virtual Bank involved in banking activities Virtual Bank maturity Orientation products diversification • Identifying cross-selling Traditional Bank opportunities • Managing multiple vendors/service providers - least cost, best service. • ............................................... • Internet - phone integration • WEB-TV • Multimedia approach to market and products The “virtual bank” maturity Batch Real-time External Issue Internal IT Fluid Static Dynamic

Considerations Any global model able to consider both the technological and organizational aspects and the other exogenous and endogenous factors that fragment the financial world, has to be considered too difficult to create and manage. The proposed framework has been used to perform a general analysis in our research, but it is evident that a different mix of analysis instruments should produce different reflections.

Value Network subject Direct Bank on involved Direct Bank electronic in banking markets activities Traditional Bank approach to market and products The framework External Internal Static Dynamic

new partners/competitors “Customer retention” “Market share” Banks on the Net Banks focus on... External Value network Subjects involved in banking activities Direct Bank on EM Direct Bank Traditional Bank Internal Fixed Dynamic Approach to products and markets

La clientela bancaria italiana su Internet Velocità del mezzo di comunicazione. Modo più facile di operare con la banca 40.48% Comodità offerta dal mezzo di comunicazione. Poter operare da casa e dal posto di lavoro 52.68% Risparmio di tempo. Indipendendenza dallo sportello. 30.31% Disponibilità del servizio 24 ore su 24 26.80% Commissioni ridotte 8.68% Accedere a informazioni su prodotti e servizi finanziari sempre aggiornate e in tempo reale13.49% Indagine WMTOOLS (mag-99)

VAS Price/Services Easiness Banks on the Net Customers focus on…. External Value network Subjects involved in banking activities Direct Bank on EM Direct Bank Traditional Bank Internal Fixed Dynamic Approach to products and markets

Thanks Andrea CarignaniUniversità Cattolica di Milano andrea@eurobanca.comwww.eurobanca.com