Download

1 / 39

420 likes | 465 Views

This text explains how to consolidate ownership and account for dividends in financial statements for subsidiaries using the equity method. It provides detailed calculations and entries for clarity.

E N D

Baker / Lembke / King 9 Consolidation Ownership Issues Electronic Presentation by Douglas Cloud Pepperdine University

Subsidiary Preferred Stock Outstanding Peerless Products purchased 80 percent of the common stock of Special Foods on December 31, 20X0, at its book value of $240,000 and accounts for the investment using the basic equity method. Peerless Products earns income from its own operations of $140,000 in 20X1 and declares dividends of $60,000. Special Foods reports net income of $50,000 in 20X1 and declares common dividends of $30,000. On January 1, 20X1, Special Foods issued $100,000 of 12 percent preferred stock at par value, none of which is purchased by Peerless.

Subsidiary Preferred Stock Outstanding Peerless’s Income from Special Foods Special Foods’ net income, 20X1 $50,000 Less: Preferred dividends ($100,000 x .12) (12,000) Special Foods’ income accruing to common shareholders $38,000 Peerless’s proportionate share x .80 Peerless’s income from Special Foods $30,400

Subsidiary Preferred Stock Outstanding Income to Noncontrolling Interest Preferred dividends of Special Foods $12,000 Income assigned to Special Foods’ noncontrolling common shareholders ($38,000 x .20) 7,600 Income to noncontrolling interest $19,600

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Subsidiary 30,400 Dividends Declared-- Preferred (12,000) Common (60,000 (30,000) Investment in Special Foods 246,400 ) An entry is required to eliminate income from Special Foods.

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income from Subsidiary 30,400 (1) 30,400 Dividends Declared— Preferred (12,000) Common (60,000 (30,000) (1) 24,000 Investment in Special Foods 246,400 (1) 6,400 )

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income to Non- controlling Interest Dividends Declared-- Preferred (12,000) Common (60,000) (30,000)(1) 24,000 Noncontrolling Interest An entry is needed to assign income to noncontrolling interest.

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Income to Non- controlling Interest(2) 19,600 (19,600) Dividends Declared-- Preferred (12,000)(2) 12,000 Common (60,000) (30,000)(1) 24,000 (2) 6,000 (60,000) Noncontrolling Interest (2) 1,600

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, Jan. 1 300,000 100,000 Investment in Special Foods 246,400 (1) 6,400 Common Stock 500,000 200,000 Noncontrolling Interest (2) 1,600 An entry is necessary to eliminate the beginning investment in common stock.

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Retained Earnings, Jan. 1 300,000 100,000 (3) 100,000300,000 Investment in Special Foods 246,400 (1) 6,400 (3)240,000 Common Stock 500,000 200,000 (3) 200,000500,000 Noncontrolling Interest (2) 1,600 (3) 60,000

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Preferred Stock 100,000 Noncontrolling Interest (2) 1,600 (3) 60,000 An entry is necessary to eliminate subsidiary preferred stock

Consolidation Workpaper--20X1 Peerless Special Eliminations Item Products Foods Debits Credits Consolidated Preferred Stock 100,000(4) 100,000 Noncontrolling Interest (2) 1,600 (3) 60,000 (4) 100,000 161,600

Subsidiary Preferred Stock Held by Parent ($50,000 - $12,000) x .80 Elimination entry needed in the workpaper prepared at the end of 20X1. E(5) Income from Subsidiary 30,400 Dividends Declared--Common 24,000 Investment in Special Foods Common 6,400 Eliminate income from subsidiary.

Subsidiary Preferred Stock Held by Parent $12,000 x .60 Elimination entry needed in the workpaper prepared at the end of 20X1. E(6) Dividend Income--Preferred 7,200 Dividends Declared--Preferred 7,200 Eliminate dividend income from subsidiary preferred.

Subsidiary Preferred Stock Held by Parent $4,800 + $7,600 $12,000 x .40 Elimination entry needed in the workpaper prepared at the end of 20X1. E(7) Income to Noncontrolling Interest 12,400 Dividends Declared--Preferred 4,800 Dividends Declared--Common 6,000 Noncontrolling Interest 1,600 Assign income to noncontrolling interest.

Subsidiary Preferred Stock Held by Parent Elimination entry needed in the workpaper prepared at the end of 20X1. E(8) Common Stock--Special Foods 200,000 Retained Earnings, January 1 100,000 Investment in Special Foods Common 240,000 Noncontrolling Interest 60,000 Eliminate beginning investment in common stock.

Subsidiary Preferred Stock Held by Parent Elimination entry needed in the workpaper prepared at the end of 20X1. E(9) Preferred Stock--Special Foods 100,000 Investment in Special Foods Preferred 60,000 Noncontrolling Interest 40,000 Eliminate subsidiary preferred stock.

Special Points About the Eliminating Entries • Peerless’s 60 percent share of Special Foods’ preferred stock is eliminated against the preferred stock investment account. The remaining preferred stock is included in the noncontrolling interest account. • Peerless’s dividend income from its investment in Special Foods’ preferred stock is eliminated against its share of Special Foods’ dividends declared. Continued

Special Points About the Eliminating Entries • The income assigned to the noncontrolling interest includes income of Special Foods accruing to both preferred and common shareholders other than Peerless Products. Similarly, the total noncontrolling interest includes Special Foods’ stockholders’ equity amounts accruing to both preferred and common stockholders other than Peerless.

Subsidiary Preferred Stock, Special Features Special Foods issues $100,000 par value, 12 percent preferred stock on January 1, 20X0. The stock is cumulative, nonparticipating, and callable at 105. No dividends are declared on this stock during 20X0. On December 31, 20X0, Peerless Products purchases 80 percent of the common stock of Special Foods for $240,000 and on January 1, 20X1, Peerless purchases 60 percent of the preferred stock for $61,000.

Subsidiary Preferred Stock, Special Features Special Food’s Stockholders’ Equity, December 31, 20X0 Preferred Stock $100,000 Common Stock 200,000 Retained Earnings 100,000 Total Stockholders’ Equity $400,000

Peerless’s share $70,200 (60 percent) Noncontrolling stockholders’ share $46,800 (40 percent) Subsidiary Preferred Stock, Special Features Preferred Stock Interest, January 1, 20X1 Par value of Special Foods’ preferred stock $100,000 Call premium 5,000 Dividends in arrears for 20X0 12,000 Total preferred stock interest, January 1, 20X1 $117,000

Peerless’s share $226,400 (80 percent) Noncontrolling stockholders’ share $56,600 (20 percent) Subsidiary Preferred Stock, Special Features Common Stock Interest, January 1, 20X1 Common stock $200,000 Retained earnings ($100,000 - $17,000) 83,000 Total common stockholders’ interest, January 1,20X1 283,000

Subsidiary Preferred Stock, Special Features Elimination Entries, January 1, 20X1 E(10) Common Stock--Special Foods 200,000 Retained Earnings 83,000 Differential 13,600 Investment in Special Foods Common 240,000 Noncontrolling Interest 56,600 Eliminate investment in common stock. $100,000 - 17,000 $240,000 - ($283,000 x .80) $283,000 x .20

Subsidiary Preferred Stock, Special Features Elimination Entries, January 1, 20X1 E(11) Preferred Stock--Special Foods 100,000 Retained Earnings 17,000 Investment in Special Foods Preferred 61,000 Additional Paid-In Capital 9,200 Noncontrolling Interest 46,800 Eliminate subsidiary preferred stock. $117,000 - $100,000 ($117,000 x .60) - $61,000 $117,000 x .40

Special Points About the Eliminating Entries • The $83,000 portion of Special Foods’ retained earnings relating to the common stock interest is eliminated in the first entry, with the remaining $17,000 of retained earnings related to the preferred stock interest eliminated in the next entry. • Because Peerless’s share of Special Foods’ common stock interest is $226,400 and the cost of the investment was $240,000, a $13,600 differential arises in consolidation. Continued

The total noncontrolling interest on January 1, 20X1, consists of both preferred and common stock interests, as follows: Preferred stock interest ($117,000 x .40) $ 46,800 Common stock interest ($283,000 x .20) 56,600 Total noncontrolling interest, Jan. 1, 20X1 $103,400 Special Points About the Eliminating Entries • The difference ($9,200) between the cost of Peerless’s investment in Special Foods’ preferred stock and the underlying claim on Special Foods’ net assets is $70,200 ($117,000 x .60) minus the cost of the preferred stock investment, $61,000.

Period Net Income Dividends Ending Book Value 20X0 $40,000 -0- $300,000 20X1 50,000 $30,000 320,000 20X2 75,000 40,000 355,000 Parent’s Purchase of Additional Shares On January 1, 20X0, Special Foods has $200,000 of common stock outstanding and retained earnings of $60,000. The following data relates to Special Foods: Peerless Products purchases its 80 percent interest in Special Foods in several blocks as shown on Slide 28.

Ownership Purchase Percentage Book Date Purchased Cost Value Differential 1/1/X0 20 $ 56,000 $ 52,000 $ 4,000 12/31/X0 10 35,000 30,000 5,000 1/1/X2 50185,000160,00025,000 80 $276,000 $242,000 $34,000 Note that Peerless does not gain control until January 1, 20X2. Parent’s Purchase of Additional Shares

Investment in Special Foods Stock 20X0 Balance 99,000 Parent’s Purchase of Additional Shares 1/1 Purchase shares 56,000 12/31 Equity-method income (20%) 8,000 12/31 Purchase shares 35,000

Investment in Special Foods Stock 20X1 20X1 12/31 Dividends received 9,000 Balance 105,000 Parent’s Purchase of Additional Shares Balance 99,000 12/31 Equity-method income (30%) 15,000

Investment in Special Foods Stock 20X2 20X2 12/31 Dividends received 32,000 Balance 318,000 Parent’s Purchase of Additional Shares Balance 105,000 1/1 Purchase shares 185,000 12/31 Equity-method income (80%) 60,000

Parent’s Purchase of Additional Shares The consolidation workpaper prepared at the end of the year includes: E(12) Income from Subsidiary 60,000 Dividends Declared 32,000 Investment in Special Foods Stock 28,000 Eliminate income from subsidiary.

Parent’s Purchase of Additional Shares The consolidation workpaper prepared at the end of the year includes: E(14) Income to Noncontrolling Interest 15,000 Dividends Declared 8,000 Noncontrolling Interest 7,000 Assign income to noncontrolling interest. $40,000 x .20 $15,000 - $8,000

Parent’s Purchase of Additional Shares The consolidation workpaper prepared at the end of the year includes: E(14) Common Stock--Special Foods 200,000 Retained Earnings, January 1 120,000 Land 34,000 Investment in Special Foods 290,000 Noncontrolling Interest 64,000 Eliminate beginning investment balance. $105,000 + $185,000 $320,000 x .20

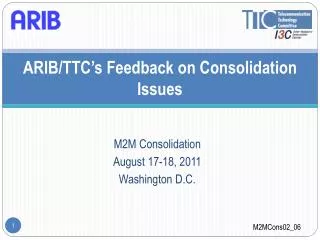

B Company C Company Alternative Ownership Structures A Company (a) Direct Ownership

B Company C Company Alternative Ownership Structures A Company (b) Multilevel Ownership

B Company Alternative Ownership Structures A Company (c) Reciprocal Ownership

Chapter Nine The End