Designing Substantive Procedures

Designing Substantive Procedures. The auditor “must plan and perform the audit to reduce the audit risk to an acceptably low level that is consistent with the objective of an audit (ISA 200). The audit risk depends on: Inherent, Control and Detection Risk.

Designing Substantive Procedures

E N D

Presentation Transcript

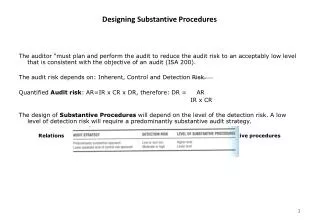

Designing Substantive Procedures The auditor “must plan and perform the audit to reduce the audit risk to an acceptably low level that is consistent with the objective of an audit (ISA 200). The audit risk depends on: Inherent, Control and Detection Risk. Quantified Audit risk: AR=IR x CR x DR, therefore: DR = AR IR x CR The design of Substantive Procedures will depend on the level of the detection risk. A low level of detection risk will require a predominantly substantive audit strategy. Relationship between audit strategy, detection risk and level of substantive procedures 1

Designing Substantive Procedures Assessing control risk for account balances Internal control systems usually applies controls at the time the relevant transaction is first recognized and recorded. Consequently, control risk is assessed by reference to transaction classes, i.e. the substantive procedure is applied to account balances. Account balance assertions for a single transaction class Such transaction classes are most of the P&L accounts (sales, purchases, expenses). This is relatively simpler. Account balance assertions for multiple transaction classes Most balance sheet accounts are affected by more than one transaction class (cash, receivables, payables etc). Thus the control risk assessment for the valuation assertion of the cash balance is based on the control risk assessments for the accuracy for both cash receipts and cash payments. Relevant control risk assessments for transactions classes affecting the cash balance 2

Designing Substantive Procedures Effects of preliminary audit strategies After making a preliminary assessment of the risk of material misstatement the auditor needs to determine the appropriate strategy for the audit. These can be either a predominantly substantive approach or a lower assessed level of control risk approach. In either case the auditor needs to identify types of potential misstatement in the assertions. Predominantly substantive approach Adopted in cases of high control risk, i.e. when: • There are no significant control procedures that pertain to the assertion • Relevant control procedures are ineffective • It would not be efficient to perform tests of controls This may occur more often in smaller entities, which do not implement appropriate controls or apply ineffective control, usually due to lack of duties segregation. Lower assessed level of control risk The auditor must first test the control procedures.

Designing Substantive Procedures Designing Substantive Procedures Having determined the audit strategy, the auditor must design the relevant procedure. These will either provide evidence that supports the truth and fairness of the financial statements or they will reveal monetary errors or misstatements in the recording or reporting of transactions and balances. Designing substantive procedures should consider: • Nature • Timing and • Extent Nature Refers to the type and effectiveness of the auditing procedures, i.e. • Analytical procedures • Tests of details of transactions • Tests of details of balances Analytical procedures These involve detailed, analytical controls. For example in a hotel audit, where most revenue is billed to many customers and in many instances, appropriate tests should be applied, although they may be tedious and costly. At an aggregate level these can be estimated a a multiple of room occupancy and average customer spending. At a detailed level it may be necessary to conduct sample audits to specific time periods and departments.

Designing Substantive Procedures Test of details of transactions These include evidence from a sample (or all) of the individual debits and credits that make up an account to reach a conclusion about the account balance. They should include inspection of documents including tracing and vouching. Cutoff tests are applied to closing balances. They are usually applied at critical dates (e.g. balance sheet closing). It necessary to ensure proper cutoff, since cutoff errors or misstatements can significantly affect profit. Tests of details of balances These are focused on obtaining evidence about account balances rather than on individual transactions. They may include auditing of customer or supplier balances, or physical inspection of the company’s inventory in the warehouse. Detection risk and assertion level for details of balances

Designing Substantive Procedures Examples of analytical procedures for auditing Trade Receivables: - comparing this year's closing balance in the control account with the prior year's balance, a budgeted amount or other expected value; - using the closing balance to determine the percentage of trade receivables to current assets for comparison with the prior year's percentage or industry data; - using the closing balance to calculate the trade receivables' turnover ratio for comparison with the prior year's ratio, industry data or other expected value; Tests of details of transactions such as: - vouching a sample of the individual debits and credits in customer accounts, for the transaction classes indicated, to the entries in journals (for example, vouching the debits to the sales journal) and supporting documentation (such as sales invoices); • tracing transactions data from source documents (such as remittance advices) and journals (such as the cash receipts journal) to the corresponding entries in the customer accounts for the transaction classes indicated; Tests of details of balances, such as: - determining that the closing balances in the individual customer accounts add up to the control account balance; • confirming the balances for a sample of customer accounts with the customers. In the case of trade receivables, it is common to apply each of the three types of substantive procedure to some extent. For other accounts only one or two of the types of test may be performed in obtaining sufficient evidence to meet the planned level of detection risk.

Designing Substantive Procedures Examples of analytical procedures for auditing Sales Revenue In practice, the sales revenue account may show only daily, weekly or monthly totals posted from the sales journal. In either case, to determine that sales revenue is true and fair, auditors may obtain evidence from any of the following: Analytical procedures, such as: - comparing the closing balance with the prior year's balance, a budgeted amount or other expected value • comparing the closing balance with an independent estimate of the closing balance (as illustrated for a hotel's revenues earlier in the chapter); Tests of details of transactions, such as: - vouching the individual credits to the sales journal and to supporting documentation such as sales invoices, shipping documents and sales orders; • tracing transactions data from source documents such as shipping documents, to sales invoices, to the sales journal, and then tracing postings from the sales journal to the sales account; Tests of details of balances (this type of test is unlikely to be applicable). In many cases, both analytical procedures and tests of details are applied to the sales revenue account to achieve the acceptable level of detection risk. In some cases, analytical procedures may suffice

Designing Substantive Procedures Timing Most entities have similar year ends (31st December, 30th June or 31st March). Consequently the preceding few months are a “busy” period for the auditors. To reduce the pressure auditors may try to perform as much work as possible in “quieter” periods. In such cases, certain procedures (typically test of details of transactions and/or balances) can be performed several months before closing, followed by a roll-forward test to verify account balances at year end. Substantive procedures prior to balance sheet date These should include: • Confirmation of trade receivables • Observation of inventory count and • Physical inspection of investments Extend The amount of evidence obtained can vary by changing the extent of substantive procedures. The extent relates to the size of the samples selected.

Designing Substantive Procedures Risk components and the nature, timing and extent of substantive procedures