Download

1 / 44

440 likes | 616 Views

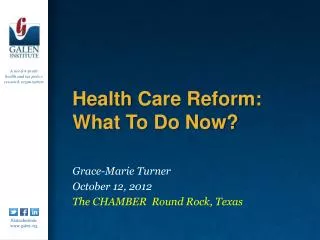

LSU Now and in the Post Health Care Reform World. Fred Cerise July 19, 2011. U.S. health care is expensive. International Comparison of Spending on Health, 1980–2008. Total expenditures on health as percent of GDP. Average spending on health per capita ($US PPP).

E N D

LSU Now and in the Post Health Care Reform World Fred Cerise July 19, 2011

International Comparison of Spending on Health, 1980–2008 Total expenditures on healthas percent of GDP Average spending on healthper capita ($US PPP) Source: OECD Health Data 2010 (June 2010).

Premiums Rising Faster Than Inflation and Wages Cumulative Changes in Components of U.S. National Health Expenditures and Workers’ Earnings, 2000–09 Projected Average Family Premium as a Percentage of Median Family Income, 2008–20 Percent Percent 108% 32% 24% Projected * 2008 and 2009 NHE projections. Data: Calculations based on M. Hartman et al., “National Health Spending in 2007,” Health Affairs, Jan./Feb. 2009 and A. Sisko et al., “Health Spending Projections Through 2018,” Health Affairs, March/April 2009. Insurance premiums, workers’ earnings, and CPI from Henry J. Kaiser Family Foundation/Health Research and Educational Trust, Employer Health Benefits Annual Surveys, 2000–2009. Source: K. Davis, Why Health Reform Must Counter the Rising Costs of Health Insurance Premiums (New York: The Commonwealth Fund, Aug. 2009).

While health care costs increase, there is a strong public sentiment to reduce spending among public programs • We have access problems today among our public program • Having a Medicaid card does not ensure access to services

The government can’t afford to continue feeding the medical-industrial complex at its current rate

Slide from Uwe Reinhardt presentation to NAPH 6/11

Current Health Care Spending is Non-Sustainable • During the past 4 decades, per beneficiary costs under Medicaid and Medicare increased 2.5% faster per year than the rest of GDP. • If that trend continues, federal spending on those two programs alone would rise from 4.6% GDP in 2007 to 20% by 2050. This represents the same share of the economy that the entire federal budget does today. • For all of health care this would represent 40% of GDP in 2050 • That can’t happen

Public delivery systems can be capped and can offer predictable spending and lower costs solutions for some populations

Total Medicaid Spending vs. LSU Hospital Medicaid & DSH Millions

Mini-Med Plans • McDonald’s (Montana) employees pay $56/mo for coverage of up to $2,000/yr • Ruby Tuesday employees pay $18/wk for $1,250 outpatient and $3,000 inpatient care/yr • Denny’s employees pay $69/mo for no inpatient coverage and $300 maximum doctor’s office visits

Affordable Care Act Phases Out Some Caps • Phases out annual dollar limits • Requires essential benefits package for individuals purchasing their own coverage or through small employers • Large employer requirements regarding benefits package not clearly laid out

What Does the Future Hold?2 or 3 Tiers • Wholly Privates: Those who can afford high cost and overutilization • Wholly Publics: Uninsured and Medicaid (Medicare?) • Stressed in the Middle: ESI and Medicare • Delivery system reforms essential to maintaining access • 30% “waste” in the system

Proposed Delivery System Reforms • Medical Homes • Accountable Care Organizations • Coordinated Care Networks • Bundled Payments • Pay for Performance • You get the idea

Delivery system reforms require infrastructure which requires scale. Most U.S. physicians do not practice in large groups. Eighty eight percent of visits to office-based practices are to practices with 9 or fewer physicians.Health Affairs, Web First, August 2011

But this world is changing too.Hospitals are acquiring physician practices again.Insurers are beginning to acquire physicians and hospitals.

Advantages of Hospitals Acquiring PhysiciansNEJM, 5/12/11 • Reduce costs associated with unnecessary practice variation and unnecessary expensive supplies selected by physicians • Standardizing surgical supplies • Selecting cost-effective devices • Requiring use of HIT • Requiring adherence to clinical guidelines • Scheduling elective procedures to maximize asset utilization • Discharging patients consistently early in the day • Doctors trading autonomy for employment

LSU A Huge Head Start – But Not For Long • “Hospital owned practices” • Medical homes • Electronic health records • Chronic disease registries • Disease management programs • Funding flexibility

LSU cannot rely upon being a default public provider. Others will attempt to provide some of these services for additional money. • There is vocal rhetoric regarding our services without regard for the facts.

Strategies LSU Must Employ • Establish greater sense of urgency • Understand our finances • Manage our costs • Improve our quality • Improve patient experience • Improve access – the right thing to do (and insurers will require it) • Primary care • Specialty care • Strategic use of NPs and PAs • Develop partnerships to maximize our services • Balance training and service

Improve Access and QualityBalance Training and Service • We can train AND provide consistent reliable access • We cannot rely SOLELY on residents as PCPs • Use of nurses, NPs and PAs • Consistent and accountable faculty supervision

UHC = Blocking and Tackling • Must have unit costs that are at least in-line with the industry. Should be lower. • Must be able to demonstrate that FTEs are in-line with the industry • Where it makes sense to outsource, outsource • But not for our core expertise • Reliable measures and managers must be accountable to meeting them

Improve Quality • Basics first • Goal for 2012: • No CMS core measure below 50th percentile • All hospitals should be operating in top quartile • Establish targets and managers must be accountable to meeting targets

Improve the Patient Experience • Friendly, attentive, considerate staff • CLEAN facilities • Respect appointments • Be available • “Would you return for care….” • “Would you recommend.…” • Managers must demonstrate attention to the measures and improvements

Develop Partnerships • Among ourselves • Rural hospitals and practices • FQHCs • Capacity expected to double under ACA • Other hospitals and practices

Developing Partnerships • Ease of referrals • Clinics • Emergency departments • Inpatients • Telemedicine • Shared electronic records • Strategic LINCCAs

Summary • Health care is expensive and unaffordable for the entire U.S. population given current practices • Pressure to provide ongoing access while reducing costs • Tiers likely to become more explicit • LSU has structural advantages that must be exploited to allow us to continue providing public services (delivery, education, research) • Others will attempt to profit from changes • LSU must outperform competitors; measure its results; and report in simple, indisputable terms