Download

1 / 16

160 likes | 317 Views

DHCFP Annual Public Hearing: Health Care Cost Trends. Commissioner Joseph G. Murphy Massachusetts Division of Insurance June 27, 2011. Premium Trends. DHCFP Premium Trend Reports have illustrated

E N D

DHCFP Annual Public Hearing:Health Care Cost Trends Commissioner Joseph G. Murphy Massachusetts Division of Insurance June 27, 2011

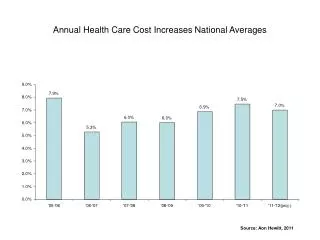

Premium Trends • DHCFP Premium Trend Reports have illustrated • Premiums are rising for all individuals and employers, arguably at levels beyond the affordability of many Massachusetts residents • Administrative costs are rising • Are higher per person for small groups and individuals • Fluctuate from year to year with new investments in spending • Are a declining portion of total premium dollars – as measured by medical loss ratios – as total health care dollars have grown • Medical loss ratios are increasing except for slight decline in calendar year 2010

Health Expenditure Trends • DHCFP Health Trend Reports have illustrated • Health expenditures have risen dramatically since 2002 as utilization, service prices and mix of services have increased • Private payors are being expected to pay higher service prices for certain services to make up for shortfalls from public payor rate of reimbursement • Utilization has increased for many outpatient services, including radiology and laboratory services • Consumers are receiving more care from higher cost providers.

PART OF THE SOLUTION: WHAT IS PERMITTED UNDER EXISTING LAWS

Prior to April 2010 • August 2009 – Governor Patrick charged the Division of Insurance (“Division”) with investigating and determining all reasonable options to address the rising cost of health coverage impacting small businesses. • October 2009 – Governor Patrick directed the Division to schedule informational hearings to examine health insurance premium increases, concentrating on small group premium increases and actions that carriers were taking to address increases costs. • February 2010 – Division issued emergency regulations requiring small group health insurance rate filings be submitted prior to proposed rate effective date and include supporting documentation.

April 2010 • Carriers filed rate increases ranging from 6% to 34%. • After detailed review, the Division disapproved 235 of 274 proposed rate increases because they failed to meet statutory requirements that rates not be excessive or unreasonable in relation to the benefits provided. • Carriers appealed the disapprovals through an adjudicatory hearing process before independent hearing officers at the Division. • Six of the seven administrative proceedings were resolved through settlement agreements with favorable outcomes for Massachusetts insureds. • The Division’s actions saved individuals and small employers $106 million in premiums they would otherwise have paid under the originally proposed rates.

Existing Laws New Chapter 288 (signed by Governor Patrick on August 10, 2010) Process to Review Rate Filings • Historically, small group health insurance rates were “filed and used” on the date rates were effective, and rate filings had very little detail about the reasons for rate changes over the prior period. • The Division’s emergency regulatory changes in February 2010 required carriers to submit small group rate filings prior to their effective date and further required detailed information supporting the filing. • Chapter 288 further modified the rate review standards for small group health insurance. Pursuant to the law and regulatory amendments, as of April 1, 2011, carriers must file rates at least 90 days prior to their proposed effective date.

Existing Law New Chapter 288 Rate Disapproval Standards • The Division will presumptively disapprove a carrier’s small group insurance rates if: • The projected medical loss ratio (MLR) is less than 88% in 2011 and 90% in 2012; beginning in 2013, carriers must meet the federal MLR standard; • The contribution-to-surplus load (profit)is greater than 1.9%; or • The administrative expense load increases by more than the medical CPI increase for the Northeast Region. • The Division also will disapprove a carrier’s rates if the benefits are unreasonable in relation to the rates charged, if the rates are excessive, inadequate or unfairly discriminatory, or if they do not otherwise comply with legal or regulatory requirements.

Existing Laws • Chapter 288 included provisions that: • Enhance Division’s review of small group rate filings • Require smoothing or age adjustment factors • Require limits on increases due to demographic changes to groups • Authorize creation of group purchasing cooperatives for small groups • Address open enrollment features that led to abuses in coverage for those who would buy coverage only when they needed medical procedures • Require carriers to offer limited and tiered provider network products for small employers that will cost 12% less than full network products • Require carriers to file annual statements including detailed information income and expenses • Facilitate Division regulation of third-party administrators

Existing Law New Product Offerings • Limited and Tiered Provider Network Products Carriers that cover more than 5000 eligible individuals or small employers are required to offer a limited or tiered network product to eligible individuals and small employers in the largest metropolitan region in the carrier’s service area that costs at least 12% less than the carrier’s most actuarially similar non-limited/non-tiered network product. • Group Purchasing Cooperatives Chapter 288 of the Acts of 2010 amended a longstanding provision in the Massachusetts market for small group health coverage that prohibited small employers from joining together to negotiate rates with health carriers. The Division promulgated regulations that facilitate the creation of 6 group purchasing cooperatives that can offer coverage to members of qualified associations who have contracted with the cooperative.

ADDITIONAL SOLUTIONS: WHAT NEEDS TO BE ADDRESSEDIN NEW LAWS

WHAT IS MISSING? • The DOI has much greater authority to conduct detailed review of the components of insurer rate filings and can disapprove rates with • Excessive administrative costs; • Excessive contributions to profits; or • Inadequate medical loss ratios. • In order to truly impact the rate of premium growth, the DOI needs much greater authority to disapprove insurer rate filings that include excessive levels of projected payments to providers based • on inefficient systems of care; or • excessive levels of provider reimbursement.

Governor’s Health Care Cost Containment Legislation Addressing the increase in premium levels requires addressing the increase in reimbursement Governor’s bill addresses inefficient provider systems excessive rates of provider reimbursement

Governor’s Health Care Cost Containment Legislation Addressing excessive levels of provider reimbursement • Commissioner of Insurance would have the authority to require carriers to follow certain annual parameters in contracting with providers about fee levels based on • The growth in economic indicators • A provider’s fees relative to median provider payment levels • Overall quality • Mix of patients • Movement toward alternate payment contracts • Commissioner of Insurance would have the authority to disapprove carrier rate filings that are based on provider rates of reimbursement that are not consistent with the annually established parameters

Governor’s Health Care Cost Containment Legislation Developing More Efficient Systems of Care • Promotes the use of alternative payment methodologies and establishment of integrated care organizations oraccountable care organizations (ACOs). • Promotes improved quality and patient safety by encouraging providers to disclose adverse events and analyze them to improve quality and safety. • Promotes health resources planning and creates Health Services System and Payment Reform Coordinating Council (Coordinating Council) and 18 member Health Care Innovation Advisory Committee comprised of stakeholders and experts to oversee and advise process.

DHCFP Annual Public Hearing:Health Care Cost Trends Questions?