Download

1 / 15

150 likes | 652 Views

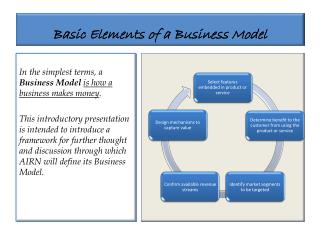

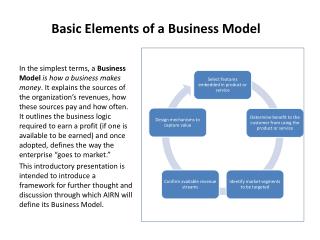

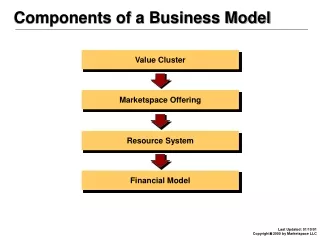

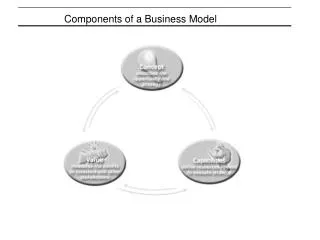

Components of a Business Model What is it? How will we? · An organization's defines its business concept Attract a large and loyal community? strategy. The concept is based on analysis of: · Deliver value to all community members? · Market opportunity ·

E N D

What is it? How will we? · An organization's defines its business concept Attract a large and loyal community? strategy. The concept is based on analysis of: · Deliver value to all community members? · Market opportunity · Price our product to achieve rapid adoption? · Product and services offered · Become #1 or #2? · Competitive dynamics · Erect barriers to entry? · Strategy for capturing a dominant position · Evolve the business to "cash in on strategic options"? · Strategic options for evolving the business · Gene rate multiple revenue streams? · Manage risk and growth? · An organization's define resources capabilities Achieve best - in class operating performance? - needed to execute strategy. Capabilities are built · Develop modular, scalable, and flexible infrastructure? and delivered through its: · Build and manage strong partnerships with em ployees · People and partners and the community? · Organization and culture · Increase the lifetime value of all members of the · Operations community? · Marketing/sal es · Build, nurture, and exploit knowledge assets? · Leadership/Management process · Make informed decisions and take actions that increase · Business development/Innovation process value? · Infrastructure/Asset efficiency · Organize for action and agility? A high - performing org anization returns to all value stakeholders. This value is measured by: · Benefits returned to all stakeholders · Benefits returned to the firm and its owners · Market share and performance Components of a Business Model (continued) · Deliver value to all stakeholders? · Claim value from stakeholder relationships and transactions? · Increase market share and drive new revenues off existing customers? · Brand and reputation · Increase brand value and reputation? · Financial performance · Generate confidence and trust? · Ensure strong growth in earnings? · Generate positive equity cash flow? · Increase stock price and market value?

BUY SELL New York Stock Exchange market model in 12/2000 • Floor - based trading of over Auction Market Model • Screen - based 3025 securities trading enables complete view of • Specialists maintain a central Specialist Acts as Agent order book – order - driven orders system • High levels of • Average daily trading volume transparency within was 1.0 billion shares per day global markets and the # of listings was 2,862 • Limited sources of • Average market value was capital $US 12.4 trillion Stocks are traded on a physical trading floor using the open-outcry auction method. Until recently, investors placed orders through stockbrokers who then communicate those orders to floor brokers who completed the trades at the booth of a specialist. In 2000, 30% of orders were transmitted electronically directly to the specialist at his/her booth on the physical trading floor. Specialists are members of the NYSE who act as auctioneers for their assigned stocks. Each stock is assigned to one specialist. -

Nasdaq Securities Exchange market model in 12/2000 • Screen - based trading of over 4734 securities Market Maker Model • Screen - based • Computer displays buy and sell trading enables quotes from multiple market Multiple Market Makers act makers – quote - driven system complete view of as Principals orders • In 2000, the Nasdaq market united over 500 market making firms • High levels of BUY SELL transparency within • On average, each stock was global markets traded by 10 different market makers, which encouraged • Limited sources of competition among market capital makers driving prices down • Average daily trading volume was 1.8 billion shares per day and the # of listings was 4,734 • Average market value was $US 3.6 trillion Unlike the NYSE where trading was driven by the flow of orders received by specialists, trading on the NASDAQ was driven by quotes from multiple market makers that commit their own capital to establish a buy and sell position in each stock that they wish to trade. The position reflects the price they would be willing to buy (bid) and sell (offer) a stock. The pricing window between the best bid and offer is called the “inside spread.”

SELL BUY ECN market model in 12/2000 • Screen - based automated trading Automated Trading Market Model • Computer acts as a specialist • Screen - based attempting to match orders from individuals and market makers – trading enables Computer System acts as order - driven system complete view of Agent orders • In 2001, the oldest and largest ECN, Instinet , had over 21,000 subscribers • High levels of and accounted for over 12% of Nasdaq transparency within daily volume global markets • Unlike exchanges, ECNs were not • Limited sources of required to divulge the identity of capital individuals and firms trading on its network and could charge a subscription fee of its members • In 2001, ECNs charged $2 - $5 per trade vs $50 - $60 per trade by a human broker Like the NYSE, Electronic Communication Network (ECN) trading was driven by the continuous flow of buy and sell orders, rather than by the competitive quote-driven trading as seen on the Nasdaq. But, unlike the NYSE, orders traded without the human intervention of a specialist. When a buyer or seller submitted an order to an ECN, the computer first attempted to match the order within the ECN market; in 2001 ECNs were able to match about 50% of their orders internally. If the order did not match within seconds, the ECN assumed the role of a Nasdaq market maker and the order was submitted to Nasdaq. In 2Q2001, ECNs accounted for 29% of Nasdaq market volume, up from less than 3% in 2Q 1998.

The TSE/OSE market model (mandated order flow) • Screen - based trading of over 1400 securities (TSE) and ECN Market Specialist Auction Market Model • Screen - based over 1200 (OSE) trading enables Automated System Automated system complete view of acts as an agent Acts as Agent • Automated central order book orders SELL SELL BUY BUY (limit and market orders) • High levels of • OSE turnover is 9% vs. 18% transparency within on TSE, 88% on NYSE, and global markets over 100% on Nasdaq • Limited sources of • In 2001, OSE had 88 domestic capital and 20 foreign broker/dealer members Until the late 1990s, stocks were traded on a physical floor using open outcry auction. The “itoyose” process was used to set opening price, and the “zaraba” process was used to price continuous order flow. “Saitori” (“nakadashi” at OSE) execute trades but, unlike NYSE specialists, there was no obligation to correct imbalances. With full automation, the Japanese markets have been likened to the ECN with mandated order flow.

The Nasdaq Japan market model Auction Market Auction Model Hybrid Market Model • Floor - based trading combines advantages of Specialist enables complete Acts as Agent* various market models view of orders • High levels of SELL SELL BUY BUY transparency within local market • Limited sources of capital • Screen - based Market Maker Model trading enables Market Market Specialist Multiple Market Makers complete view of Act as Principals** • Screen - based trading quotes • Screen - based trading enables complete view of SELL BUY enables complete view of • High levels of orders and quotes orders and quotes transparency among • Competing market makers multiple market • Competing market makers yield narrower spreads makers yield narrower spreads • Multiple sources of capital • Multiple sources of • Multiple sources of capital capital • Meets needs of retail, • Meets needs of retail, • Screen - based institutional, and institutional, and trading enables ECN Market Specialist corporate investors corporate investors complete view of Automated System Acts as Agent • Enables anonymity orders • Enables anonymity SELL BUY • High levels of • Continuous order flow; no • Continuous order flow; no transparency within need to stop for need to stop for global markets imbalances imbalances • Limited sources of capital

Comparison of Japanese securities markets TSE accounts for 70% of shares listed, 80% of trading value, and 90% of trading volume Large/ Large/ Established Established TSE and TSE and TSE and TSE and OSE OSE OSE OSE Section 1 Section 1 Section 1 Section 1 Nasdaq Nasdaq Nasdaq Nasdaq Issuer Size Issuer Size Japan Japan Japan Japan & Maturity & Maturity TSE TSE TSE TSE and OSE and OSE and OSE and OSE Section 2 Section 2 Section 2 Section 2 Jasdaq Jasdaq Jasdaq Jasdaq OTC OTC OTC OTC TSE TSE TSE TSE Mothers Mothers Mothers Mothers Small/ Small/ Young Young Slow Slow Fast Fast 20 20 - - 25 years 25 years 3 3 - - 5 years 5 years Average Time to Public Offering

The Nasdaq Japan market model Business Concept: Market Opportunity Product and service offered Competitive Dynamics Strategy for capturing dominant position Strategic options for evolving the business

Nasdaq Japan market entry strategy June 19, 2000 Early 2002 ??? Phase 1 Phase 2 Phase 3 Enter Quickly Using Launch Hybrid Link Global Pools OSE Market Platform Market Model of Liquidity

Nasdaq Japan Phase 1 operating model OSE trading engine & Nasdaq Japan Club OSE/NJ reporting customer workstations NJ Marketing OSE/NJ delisting stds . OSE market information Communications OSE disclosure NJ website OSE clearance & settlement NJ/OSE listing stds .

Nasdaq Japan Phase 2 operating model Nasdaq Japan Club NJ trading engine & customer workstations NJ Marketing (Indigo Markets software + OSE/NJ reporting Communications hosting in Tokyo) OSE/NJ delisting stds . NJ website NJ/OSE market information NJ listing stds . NJ/OSE disclosure OSE clearance & settlement

Nasdaq Japan governance structure

Nasdaq Japan financing history Nasdaq U.S. Nasdaq U.S. Nasdaq U.S. Nasdaq U.S. Softbank Softbank Softbank Softbank Post Post Post Post - - - - Money % Ownership Money % Ownership Money % Ownership Money % Ownership Burn Rate: Burn Rate: Burn Rate: Burn Rate: December 2001 December 2001 2000 2000 2000 2000 - - - - 2001: ¥1.9 billion 2001: ¥1.9 billion 2001: ¥1.9 billion 2001: ¥1.9 billion Nasdaq U.S. Nasdaq U.S. Nasdaq U.S. Nasdaq U.S. 42.9% 42.9% 42.9% 42.9% www. www. www. www. nasdaq nasdaq nasdaq nasdaq .com .com .com .com Softbank Softbank Softbank Softbank 42.9% 42.9% 42.9% 42.9% www. www. www. www. softbank softbank softbank softbank .co. .co. .co. .co. jp jp jp jp 2002: ¥24 million 2002: ¥24 million 2002: ¥24 million 2002: ¥24 million Strategic Strategic Strategic Strategic 2003: ¥12 million 2003: ¥12 million 2003: ¥12 million 2003: ¥12 million Investors Investors Investors Investors 13.8% 13.8% Nasdaq Japan, Inc. Nasdaq Japan, Inc. Nasdaq Japan, Inc. Nasdaq Japan, Inc. June 2001 ¥ 937.5 million June 2001 ¥ 937.5 million June 2001 ¥ 937.5 million June 2001 ¥ 937.5 million June 1999 ¥ 300 million June 1999 ¥ 300 million June 1999 ¥ 300 million June 1999 ¥ 300 million Limited Limited Limited Limited Dec. 2001 ¥ 937.5 million Dec. 2001 ¥ 937.5 million Dec. 2001 ¥ 937.5 million Dec. 2001 ¥ 937.5 million Partners Partners Partners Partners 0.4% 0.4% October 2000 ¥5 billion October 2000 ¥5 billion October 2000 ¥800 million October 2000 ¥800 million October 2000 ¥5 billion October 2000 ¥5 billion October 2000 ¥800 million October 2000 ¥800 million www. www. www. www. nasdaq nasdaq nasdaq nasdaq - - - - japan japan japan japan .com .com .com .com Strategic Investors (¥500 million each) Strategic Investors (¥500 million each) Strategic Investors (¥500 million each) Strategic Investors (¥500 million each) Limited Partners Limited Partners Limited Partners Limited Partners