Download

1 / 13

130 likes | 257 Views

This paper examines the implications and mechanisms of informed trading within regulated industries, highlighting the paradoxical role of government interventions. It discusses how regulation, intended to safeguard against insider information leakage and enhance shareholder protection, can inadvertently create pathways for further informed trading. Drawing on various natural experiments and extensive evidence, the authors analyze scenarios in the banking, airline, and trucking sectors, demonstrating how oversight may sometimes foster additional insider access to information. The study concludes with an array of insights applicable to regulators and market participants alike.

E N D

InformedTradinginRegulatedIndustries DavidM.Reeb,YuzhaoZhangandWanliZhao DiscussionbyKo-ChiaYu ShanghaiUniversityofFinanceandEconomics 2012NTUICF

Thebiggerpicture • Whydo governments regulate? • Togain control over a certain strategically important sector. • Shareholder protection • Monitoringofwrongdoingofcorporateinsiders • Limittheinformationleakageoftheinsiders

Thebiggerpicture • Summaryoftheresults: • Theveryactofgovernmentalinterventionmightleadtomorepassagesforinformationalleakage. • Additional“insiders”aregeneratedinthemonitoringprocess. Regulators

SummaryofFindings • Averylonglistofevidencethatincludes: • Potentialavenuesforinformedtrading • Short-sales • Equitysalesand/orpurchases • Optionmarket • Potentialinformationalleakageevents • Abnormalshort-salesbeforeearningshocks • NaturalExperiments • 1978Airlinederegulation • 1980Truckingderegulation • 1999Gramm-Leach-BlileyAct(againaderegulation,bankingindustry)

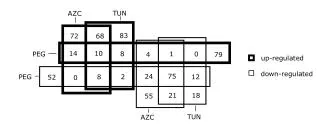

SummaryofFindings • Identification of the channels (Bank industry) • Timing of informational flows • Call report to the regulators by the end of every calendar quarter • Gone public 40 days later • Reaction in the first 20 days of the reports • Federal vs. State supervision • Duplicity increases informed trading. • Political integrity • Interaction between corruption index and supervision

OverallImpression • Verycomprehensiveandwellstructured • Convincingandveryinterestingnaturalexperimentsresults • Manydifferenttakeawaysandpossibleinterpretationsoftheresults • Highlyunlikelyformetopickupanysignificantflawtothecontentsofthearguments

PotentialAvenuesforInformedTrading • Alternativeinterpretationsoftheresults • Regulationprovidesanotherchannelofinformationleakagethusgeneratemore“pseudo-insiders.” • Dotheymitigatetheextentoftradingfromthetrueinsiders? • “Opportunistictrade”variablefromCohenet.al(2010)isincluded • Itisstillinterestingtoseehowinsidertradinginteractswiththeregulator-insidertrading

PotentialAvenuesforInformedTrading • Steele(1989)model:informationleakageasthesquareofthenumberofpeoplewhohaveaccesstotheinformation • Wouldtheresults(themassdatasampleonshort-sales,equityandtheoptionmarkets)bedrivenbythefactthattheseindustries(finance,utilities,andpharmaceuticals)consistofmorepeoplewithvaluableinsiderinformationabouttheindustry? • E.g.Apharmaceuticalresearcherwilllikelyhavethesameinformation(possiblybetterinformation)thanananalyststudyingonthefirm. • Suggestion:average employee salary (NBER data)

PotentialAvenuesforInformedTrading • Short-salemarket • Predictabilityissignificantlybetterforregulated industries than non-regulated industries • However it is not clear that this predictability can be attributed to informed traders or liquidity providers (opportunistic or not). • Diether et al (2007): reversal • Short-sale constraints • Non-transient institutional ownership, index fund ownership (Bushee 1998, among others)

PotentialAvenuesforInformedTrading • Equity market • Adjusted-PIN • Liquidity-PS is controlled. • The asymmetric information part of PIN as in Duarte and Young (2009)

Other comments • Whataboutotherregulatory changes? • Othersupervisedfirms? • Telecomm? • Supervision and regulation (more supervision than regulation, but it is the regulator who conducts the regulatory supervision) • Cost of getting caught seems to be low. (?)

MinorIssues • Table 6 “Regulatory duplicity” got truncated • Punctuation: “Although, …” in several places • Table 9 • Citation update: Adams, R. B., & Ferreira, D. (2012). Regulatory pressure and bank directors incentives to attend board meetings. International Review of Finance, 12(2), 227-248.

Conclusion • Theresearchhasa different takeaway for different people. • I really do enjoy reading the paper. • Goodlucktotheauthors!