Download

1 / 4

80 likes | 489 Views

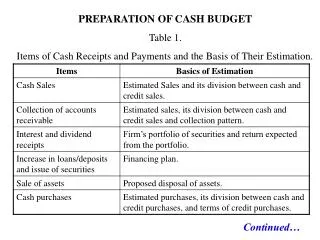

Cash Budget (example). Beginning cash balance$30,000Cash receipts913,700Cash available943,700Cash disbursements (including minimum balance)1,140,880Excess (deficiency)(197,180)Financing: Borrow (repay) 198,000Ending cash balance $35,820. . . Elements of planning an

E N D

1. Cash Budget Cash budget is a schedule of expected cash flows (receipts and disbursements);

predicts the effects on cash position at the given level of operations;

plans for the borrowing and repayment of loans

2. Cash Budget (example) Beginning cash balance $30,000

Cash receipts 913,700

Cash available 943,700

Cash disbursements

(including minimum balance) 1,140,880

Excess (deficiency) (197,180)

Financing: Borrow (repay) 198,000

Ending cash balance $35,820

3. Elements of planning and control related to cash management: Sales and credit policies:

transport, sales discounts payments conditions (eg. in 7 days, 15 days, 30 days, ...)

Purchases and payment policies :

purchases discounts , payment conditions (immediate or terms )

taking of deductions at source, sales taxes , insurance, etc.

Control:

comparison of forecast vs.... actual

taking the necessary actions to balance sources and uses of funds

4. Receipts of funds

Resulting from normal activities

Resulting from the placement of funds

Resulting from other sources (new influx of capital, long term borrowings , sales of assets, gifts, insurance indemnities , etc.)

Disbursements of funds

Resulting from normal business activities

Resulting from short and long term borrowings

Resulting from other activities (eg. acquisition of buildings, projects, etc. )

5. Controlling accounts receivable AR rotation = AR turnover

Days in recovering = average collection periodAR rotation = AR turnover

Days in recovering = average collection period