Download

1 / 60

600 likes | 732 Views

2010 TASB/TASA Annual Conference Presented by: Texas Association of School Business Officials Becky Bunte, CTSBO Director of Professional Development Tom Canby, Director of Research and Technology Houston, Texas September 24, 2010.

E N D

2010 TASB/TASA Annual Conference Presented by: Texas Association of School Business Officials Becky Bunte, CTSBO Director of Professional Development Tom Canby, Director of Research and Technology Houston, TexasSeptember 24, 2010 How to Better Monitor Financial and Operational Performance in Your ISD

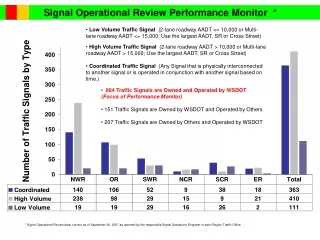

Challenges • Mandates • State law • Texas administrative code • Federal requirements • Inconsistent standards • Our members have crossed over from all types of business sectors and governmental arenas • Consensus – Public education administration is the most complex Complexities increasing yearly

Other Challenges Con’t…. • Annual growth in student enrollment on average 82,000 • Based on average annual growth for five years

Other Challenges Con’t…. Chart shows four-year percent student enrollment change all ISDs through school year 2008-2009 52% ISDs increasing enrollment over five school years

Perception - High Administrative Costs • Perception - Most costs outside of teacher classroom are administrative • Fact - Very small portion of education budget is allocated to district and campus administration • Central 3.1% • Campus 5.6% • New mandates are layered every year onto historical mandates • Administrative costs relatively flat year-over-year as percent of total budget

Perception - High Administrative Costs Con’t…. • Perception – Elimination of all funds for administration would free up resources for instruction • Fact - Elimination of all budgetary allocations for central administration would not have a significant financial impact and would not eliminate the administrative requirements. Someone must do the work. • Noncompliance with regulatory mandates results in financial penalties.

Perception - High Administrative CostsCon’t…. • Perception – Increasing portion of education budget is consumed year-over-year by administration • Fact – Administrative costs show only a small change year-over-year as percent of total budget and have declined since 2003

Other Challenges Con’t…. • Fiscal year 2010 • Deficit budgets 50% of ISDs • ($ 804.6 M)

Key Indicators to Consider • District financial fact sheet • Budget to actual • Cash flow projections • Fund balance projections • Balance sheets • Investment reports • Construction reports by project • Tax collection report • Benchmarking metrics to comparable districts • Pupil/teacher ratios • Pupil/other staff ratios • FIRST indicators and trends

Sample Financial Fact Sheet • Sample Financial Fact Sheet • (Included on last page of handout.)

Sample Financial Reports • Financial reports • Sample financial reports can be downloaded from the TASBO website – www.tasbo.org – click on Resources/Presentations/Reports • Five Year Report

Step Back and Look at the “Big Picture” • Is the revenue side living up to expectations? • Taxes at or above projection? Collection rates similar to prior years? Is local economy still healthy? Top-ranked taxpayer status? • Attendance rates at or above projection? State funding estimate still good? • Are the expenditures following the budget? • Any significant variances between budget and actual revenues and expenditures?

What Should Your Annual Audit Report Tell You About Your District? • Budget to Actual • General Fund • Child Nutrition Fund • Debt Service • Management letter

Optimum Fund Balance Schedule 1. Total General Fund Balance 8/31/10 or 6/30/10 (Exhibit C-1 object 3000 for the General Fund Only) $_______ 2. Total Reserved Fund Balance (Exhibit C-1 object 3400 for the General Fund Only) $_______ 3. Total Designated Fund Balance (Exhibit C-1 object 3500 for the General Fund Only) $_______ 4. Estimated amount needed to cover fall cash flow deficits in General Fund (net of borrowed funds and funds representing deferred revenues) $_______ 5. Estimate of two month’s average cash disbursements during the fiscal year $_______ 6. Estimate of delayed payments from state sources (58XX) $_______ 7. Estimate of underpayment from state sources equal to variance between Legislative Payment Estimate (LPE) and District Planning Estimate (DPE) or District’s calculated earned state aid amount $______ 8. Estimate of delayed payments from federal sources (59XX) $______ 9. Estimate of expenditures to be reimbursed to General Fund from Capital Projects Fund (uses of General Fund cash after bond referendum and prior to issuance of bonds) $______ 10. Adjustmernt to meet Board Policy $______ 11.Optimum Fund Balance and Cash Flow (2 + 3 + 4 + 5 + 6 + 7 + 8 + 9+10) $______ 12.Excess/(Deficit) Undesignated Unreserved General Fund (1 – 11) $______

Why is Fund Balance Important? • General Fund Balance is needed for: • Reserves • Designations • Cash flow deficit in fall until property taxes are collected in January • Financial cushion/emergencies • Bond credit ratings • Generally Undesignated Unreserved (Unassigned) Fund Balance is between 16 and 24 percent (2-3 months) of General Fund Expenditures

Bond Rating Considerations • Generally, a school district with a higher bond rating will achieve a lower borrowing cost than a district with a lower bond rating. • Key factor with all rating agencies • District fund balance is compared to other issuers • Rating agencies consider historical trends • Formal board policies related to fund balance viewed favorably

Considerations to Determine Appropriate Level • General uncertainty regarding state funding and school finance • Maintenance and Operations Tax Rate • Volatility of taxable assessed valuation

Considerations to Determine Appropriate Level • Revenue Source – Local versus State • More local – higher fund balance • Cash flow • Growth of student enrollment • Increased investment revenues for operating expenditures

Fund Balance Sample Policy • Example ISD CE (Local) Annual Operating Budget: A financial goal of the District shall be to have a sufficient balance in the operating fund to be able to maintain fiscal independence in case of a financial need or crisis. The District shall strive to maintain a yearly fund balance in the general operating fund in which the total fund balance is 32.5 percent of the total operating expenditures and the unreserved/undesignated (Unassigned) fund balance is 24 percent of the total operating expenditures.

Other Sample Policies • The annual approved budget shall maintain a cash balance approximately equal to the total expenditures of the first two months of the fiscal year. • Round Rock ISD’s Financial Policies Available at www.tasbo.org/resources/presentationsunder TASA/TASB Annual Convention-Sept. 2008 or in myTASBO Resources

Trends and Benchmarking • Benchmarks • Ratios • Peer districts • Prior audits

Sample Benchmark ReportsDemo available at http://www.tasbo.org/resources/efacts/e-facts-demo • FACTS SM

eFACTS+ • Observe patterns and correlations in • Financial Resources • Staff Resources • Student Demographics and • TAKS performance Advanced Business Analytics

Sample Benchmark Reports Total Students and Total Staff and Fund Balance General Fund

Sample Benchmark Reports Ratio Students to Counselors By Campus For An ISD

Sample Benchmark Reports Operating Costs Per Student By Campus For An ISD

Sample Benchmark Reports State Aid Funding Transportation and Costs

Sample Benchmark Reports Total Cost Per Mile and Total Mileage

Sample Benchmark Reports State Aid Funding Special Education and Costs

Sample Benchmark Reports Pct Econ Disadv and Free Lunch Participation Comparable School Districts

Sample Benchmark Reports Insurance Costs

Sample Benchmark Reports Utility Costs

Sample Benchmark Reports Source: SY 2008-2009 AEIS

Look at the Data Analyze revenue and expenditure trend lines (by function, by object, matrix combo) • Total $ • % of total • $ per student • Analyze student growth (decline) patterns • District-wide • By campus • By special populations • Develop staffing guidelines for district use for all areas • Analyze staffing patterns • Administrators (central + campus) • Student/teacher ratios • Counselors, Nurses, Librarians • Secretaries, Aides, Clerical Staff • Maintenance, Food Service, Transportation • Technology

Resources • What is TASBO doing to improve support services in Texas school districts? • Resources include: • Training • Best practices through myTASBO • Business analytics tool eFACTS+ • Onsite management reviews • Certification program

Resources Con’t… • Upgrade to knowledge management tools in progress • Mentoring program • Award of Merit Program • Future expansion by function • Performance Excellence Program (based on Baldrige)

Resources Con’t… • TASBO Performance Excellence Program • TASBO PEP • Malcom Baldrige Education Criteria for Performance Excellence • Program of National Institute Standards and Technology • http://www.baldrige.nist.gov/

Resources Con’t…. • TASBO’s goal is to be a resource for: • Performance excellence using the National Baldrige criteria as a framework for improvement. • Recognize achievement of performance excellence • Increase number of schools that also pursue National-level Malcolm Baldrige award • Tiered award program • Recognize progress implementing Baldrige Goals and Objectives

Resources Con’t…. • TASBO PEP • Rigorous evaluation • Leadership; • Strategic planning; • Customer focus; • Measurement, analysis and knowledge management; • Workforce focus; • Process management; and • Results • Implementation Systems and processes not achieved overnight

Resources Con’t…. • Malcolm Baldrige Performance Excellence • Hypothetical investment in company winners outperformed S&P 500 by 4.8 to 1 • Award winners • Higher level of quality • Lower costs • World class results

Budget Issues • Was your ISD able to adopt balanced budget for school year 2010-2011? • Approximately 50% of ISDs adopted a deficit budget for school year 2009-2010 • More ISDs will adopt deficit budgets for SY 2010-2011

Budget Reduction Strategies • Maximize participation in shared services arrangements • Elimination of bus routes within 2 miles • Reduction in hourly wage for tutorials

Budget Reduction Strategies • Renegotiation of long-term contracts/leases Photocopiers • No hiring for vacancies after Spring Break • Move forward of purchase order cut-off date for departments and campuses

Budget Reduction Strategies • No raises given for 2010-2011 school year • Summer school reduction (reduced scope of programs and grade levels served) • Freeze on district contribution for employee health insurance

Budget Reduction Strategies • Mandatory direct deposit for all employees (saves money on checks, postage, staff time, etc. Must give option of cash card) • Reduce non-campus budgets by 10% • Change student teacher ratio to increase number of students in classrooms

Budget Reduction Strategies • Energy savings projects • Eliminate Block Scheduling • Discontinue reading recovery programs • Reduced administrators (attrition) • Reduced maintenance and custodial staff