Internal Control and Cash

170 likes | 448 Views

Internal Control and Cash. Chapter 8. © 2009 The McGraw-Hill Companies, Inc. Internal Control. Definition and Purpose.

Internal Control and Cash

E N D

Presentation Transcript

Internal Control and Cash Chapter 8 © 2009 The McGraw-Hill Companies, Inc.

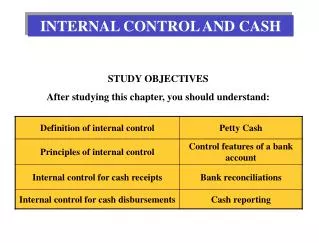

Internal Control Definition and Purpose Internal control is defined as the methods an organization uses to protect against the theft of assets, enhance the reliability of accounting information, promote efficient and effective operations, and ensure compliance with applicable laws, regulations, and codes of ethical conduct. Protect Assets Efficient Operations ReliableInformation Compliancewith Laws

Sarbanes-Oxley Act of 2002 Congress passed the Sarbanes-Oxley (SOX) Act in 2002 to enhance investor confidence in information published by a listed company and to improve the quality of financial reporting in the United States. • Reduce Opportunities for Error and Fraud • Internal control report from management, • Stronger oversight by directors, • Internal control audit by external auditors. • Encourage Good Character • Anonymous tip lines, • Whistle-blower protection, • Code of ethics. • Counteract Incentives for Fraud • Stiffer fines and prison terms.

Common Control Principles • Establish Responsibility. • Separate Duties. • Restrict Access. • Document Procedures. • Independently Verify.

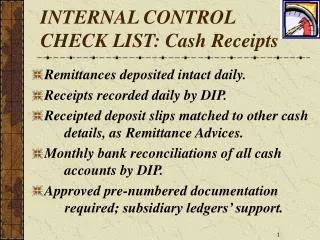

Cash Receipts Companies receive cash in person at the point of sale, or from a remote source as payment on an account. The primary internal control goal for cash receipts is to ensure that the business receives the appropriate amount of cash and safely deposits it in the bank.

Cash Received in Person For proper separation of duties, each cashier is responsible for collecting cash and issuing a receipt at the point of sale. At the end of the day, each cashier prepares a Cash Count form as shown below. Cash Count Cashier 101

Cash Received in Person The supervisor prepares a Daily Cash Receipts Summary and the bank deposit slip. The monies are deposited in the bank and a duplicate deposit slip is obtained from the bank and sent to the accounting department for verification.

Cash Received From a Remote Source Cash Received by Mail Mail Clerk CashReceiptsListing Remittance Advice Checks To supervisorfor approval. To cashier afterstamping “ForDeposit Only” To accountingdepartment.

Cash Received Electronically An electronic funds transfer (EFT) occurs when a customer electronically transfers funds from its bank account to the company’s bank account. EFTs are received immediately, and eliminate the need for some internal controls required when cash is processed manually. The company receives notice from the bank, usually daily, about deposits made through electronic funds transfers.

Cash Paid to Reimburse EmployeesPetty Cash A petty cash fund is a system used to reimburse employees for expenditures they have made on behalf of the organization. A petty cash fund acts as a control by establishing a limited amount of cash to use for specific types of expenses.

Bank Procedures and Reconciliation Banks help businesses control cash by offering services that: Safeguard Cash – The bank provides a secure place to deposit cash. Improved Efficiency and Effectiveness – The bank strengthens the processing of cash. Independent Verification – The bank statement is used to help the company account for its cash transactions.

Bank Procedures and Reconciliation Cash receiptsshould be recorded immediately upon receipt and deposited intact daily. Up to date signature cardshould be maintained. ControllingCash in theBank A deposit ticketshould be used for all deposits. A monthly bank reconciliation should be prepared by an independent party. Cash disbursementsshould be made by prenumbered check.

The Bank Statement The bank statement format varies from bank to bank, but the statement usually contains these common elements: an overall summary of the activity in the account, a list of specific transactions posted to the account, including checks cleared, deposits made, and other transactions, and a running balance in the account. Because amounts that are removed from a bank account reduce the bank’s liability, they are reported as debits on the bank statement. Debit Card

Need for Reconciliation • Your Bank May Not Know About • Errors made by the bank • Time lags • Deposits that you made recently • Checks that you wrote recently You May Not Know About Interest the bank has put into your account Electronic funds transfers Service charges taken out of your account Customer checks you deposited but that bounced (NSF checks) Errors made by you

End of Chapter 8 © 2009 The McGraw-Hill Companies, Inc.