Download

1 / 4

0 likes | 5 Views

Secure your future with the right insurance coverage in Florida. Whether itu2019s for your home, vehicle, business, or boat, Your Florida Insurance Agency provides customized policies to fit your lifestyle and budget. Enjoy peace of mind with reliable protection from storms, accidents, and unexpected events. This PPT will help homeowners and renters understand the basics of personal property coverage.<br>https://yourfloridainsuranceagency.com/

E N D

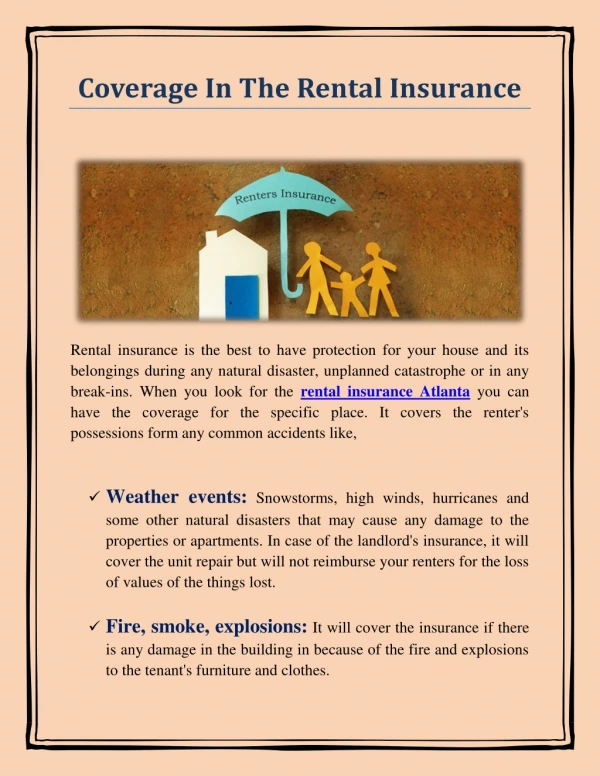

Understanding Personal Property Coverage for Homeowners and Renters Insurance Coverage In Florida yourfloridainsuranceagency.com

Do you know what your insurance actually covers? Many homeowners and renters assume their insurance fully protects their belongings. But does it? Misunderstanding personal property coverage can lead to denied claims, legal disputes, or unexpected out-of-pocket expenses. • Let’s break it down. This will help you make informed decisions about insurance coverage in Florida. It will also help you avoid costly mistakes. • Personal property coverage protects your belongings. It applies to both homeowners and renters insurance. • This coverage includes items that aren’t permanently attached to the property. Some examples include: • Electronics – Laptops, TVs, gaming consoles • Furniture – Couches, tables, beds • Clothing & Accessories – Shoes, handbags, designer pieces • Appliances & Kitchenware – Microwaves, blenders, cookware • Books, Linens, and Décor – Everything that makes a house feel like home What Is Personal Property Coverage?

Replacement Cost vs. Actual Cash Value: What’s the Difference? • When choosing insurance coverage in Florida, you must decide how you’ll be reimbursed. • There are two options: • Replacement Cost – Pays for a new item of similar quality. • Actual Cash Value (ACV) – Pays the current market value of the item. Depreciation is deducted. • Example: TV Replacement • Let’s say your five-year-old TV is destroyed in a flood. With ACV coverage, you might only receive $100 since the TV has lost value. With replacement cost coverage, you would get the amount needed to buy a brand-new TV of similar quality. • Tip: Homeowners’ policies often require an add-on for replacement cost coverage. Some renters’ policies include it by default. • Deductibles: What You Need to Know • A deductible is the amount you pay before insurance kicks in. • For example: If your $1,500 laptop is stolen, and you have a $500 deductible, your insurance will pay $1,000. • The good news? If you file a single claim for both home and personal property damage, you usually pay one deductible, not two. • How Different Industries Use RON: • Real Estate – Homeowners can digitally notarize insurance documents. This speeds up mortgage approvals. • Healthcare – Patients can securely notarize medical insurance claims from anywhere. • Legal Services – Wills and power of attorney documents can be notarized remotely. This ensures insurance payouts happen smoothly.

Final Thoughts: Review Your Coverage Today • Understanding personal property coverage helps you: • Protect your belongings at home and beyond. • Choose the right payout structure (replacement cost vs. ACV). • Avoid surprises with deductibles and policy limits. • Fully cover valuable possessions. • Create an inventory for easy claims. • Don’t wait until disaster strikes – review your policy today! • Need expert advice? Your Florida Insurance Agency! is here to help. Get a free consultation on insurance coverage in Florida. Ensure your personal property is fully protected! Get in Touch with Us 904-900-2175 service@floridaweinsure.com yourfloridainsuranceagency.com