Regulation A Compliance

30 likes | 189 Views

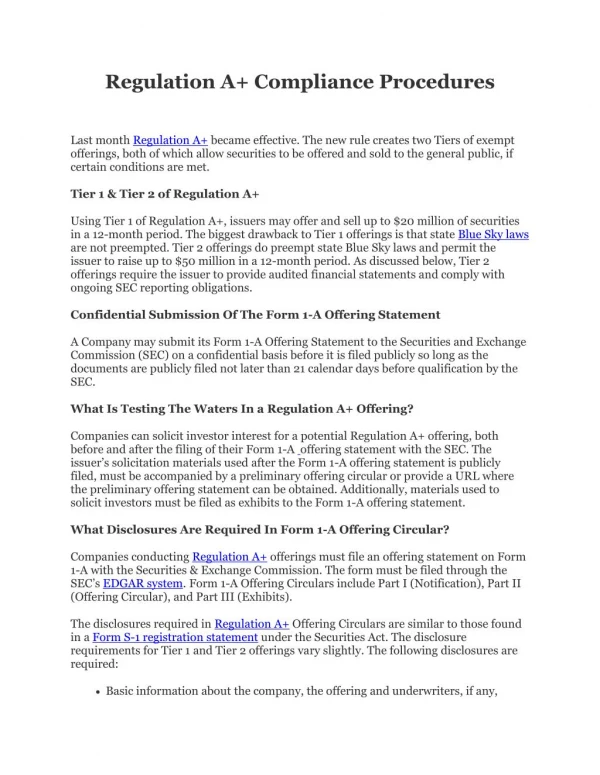

Companies can solicit investor interest for a potential Regulation A offering, both before and after the filing of their Form 1-A offering statement with the SEC. The issuer’s solicitation materials used after the Form 1-A offering statement is publicly filed, must be accompanied by a preliminary offering circular or provide a URL where the preliminary offering statement can be obtained. Additionally, materials used to solicit investors must be filed as exhibits to the Form 1-A offering statement.

Regulation A Compliance

E N D

Presentation Transcript

Regulation A+ Compliance Procedures Last month Regulation A+ became effective. The new rule creates two Tiers of exempt offerings, both of which allow securities to be offered and sold to the general public, if certain conditions are met. Tier 1 & Tier 2 of Regulation A+ Using Tier 1 of Regulation A+, issuers may offer and sell up to $20 million of securities in a 12-month period. The biggest drawback to Tier 1 offerings is that state Blue Sky laws are not preempted. Tier 2 offerings do preempt state Blue Sky laws and permit the issuer to raise up to $50 million in a 12-month period. As discussed below, Tier 2 offerings require the issuer to provide audited financial statements and comply with ongoing SEC reporting obligations. Confidential Submission Of The Form 1-A Offering Statement A Company may submit its Form 1-A Offering Statement to the Securities and Exchange Commission (SEC) on a confidential basis before it is filed publicly so long as the documents are publicly filed not later than 21 calendar days before qualification by the SEC. What Is Testing The Waters In a Regulation A+ Offering? Companies can solicit investor interest for a potential Regulation A+ offering, both before and after the filing of their Form 1-A offering statement with the SEC. The issuer’s solicitation materials used after the Form 1-A offering statement is publicly filed, must be accompanied by a preliminary offering circular or provide a URL where the preliminary offering statement can be obtained. Additionally, materials used to solicit investors must be filed as exhibits to the Form 1-A offering statement. What Disclosures Are Required In Form 1-A Offering Circular? Companies conducting Regulation A+ offerings must file an offering statement on Form 1-A with the Securities & Exchange Commission. The form must be filed through the SEC’s EDGAR system. Form 1-A Offering Circulars include Part I (Notification), Part II (Offering Circular), and Part III (Exhibits). The disclosures required in Regulation A+ Offering Circulars are similar to those found in a Form S-1 registration statement under the Securities Act. The disclosure requirements for Tier 1 and Tier 2 offerings vary slightly. The following disclosures are required: Basic information about the company, the offering and underwriters, if any,

Underwriting discounts and commissions, Summary of risk factors, Material differences between the offering price and the amount paid for shares by insiders during the past year, Plan of distribution, Selling security-holders, How offering proceeds will be spent, Business operations for the prior three fiscal years or since inception, if less than three years, Physical property/real estate, Management’s discussion and analysis of the company’s liquidity and capital resources and results of operations, Directors, executive officers and significant employees of the company, Executive compensation, Beneficial ownership by officers, directors and 10% owners, Transactions with related parties, promoters and certain control persons, and Material terms of the shares being offered. What Are The Financial Statement Requirements For Regulation A+? Tier 1 and Tier 2 offerings require the company to provide financial statements for the two most recent fiscal years. An important distinction between Tier 1 and Tier 2 offerings is that Tier 2 companies must provide audited financial statements, while Tier 1 companies may provide unaudited financial statements. U.S. based companies must prepare their financial statements in accordance with U.S. Generally Accepted Accounting Procedures (GAAP), while Canadian companies may prepare their financial statements in accordance with either US GAAP or International Financial Reporting Standards of the International Accounting Standards Board (IASB IFRS). Delivery Of The Offering Circular To Investors During the pre-qualification period of Regulation A+ offerings, companies must provide a preliminary offering circular to prospective investors at least 48 hours before the sale. When a company is subject to ongoing Tier 2 reporting obligations and current in its obligations, delivery of a preliminary offering circular is not required. Under these circumstances, the company and any intermediaries are subject to the general offering circular delivery requirements. Within two business days after each sale, companies and intermediaries must provide investors with a copy of the final offering circular or provide a notice identifying where investors may obtain the final offering circular on EDGAR and contact information for the company or intermediary. Qualification Of The Offering Statement

Offering statements must be qualified by the SEC before sales can occur. Once the SEC is satisfied with the disclosures that comply with Regulation A+, it will issue a notice of qualification. The notice of qualification is similar to the notice of effectiveness issued by the SEC for Form S-1 registration statements. Continuous & Delayed Offerings Regulation A+ permits continuous or delayed offerings. Companies conducting continuous or delayed Tier 2 offerings must be current in their annual and semi-annual reporting obligations. A company can add additional securities to their Form 1-A Offering Statement by submitting a post-qualified amendment to its previously qualified offering statement. Regulation A+ allows continuous or delayed offerings as follows: Securities offered or sold by or on behalf of a person other than the company, its subsidiary or a person of which the company is a subsidiary, Securities offered and sold pursuant to a dividend or interest reinvestment plan or employee benefit plan, Securities issued upon the exercise of outstanding options, warrants or rights, Securities issued upon the conversion of outstanding securities, Securities pledged as collateral for a loan or other obligation, Securities that are part of an offering that begins within two days after the offering’s qualification date, will be offered on a continuous basis, may continue to be offered for a period in excess of 30 days after initial qualification, and will be offered in an amount that, at the time the offering statement is qualified, is reasonably expected to be offered and sold within two years after the initial offering qualification. For further information Regulation A+, please contact Brenda Hamilton, Securities Attorney at 101 Plaza Real South, Suite 202 North, Boca Raton, FL, (561) 416-8956, or by email at info@securitieslawyer101.com. This securities law Q & A is provided as a general or informational service to clients and friends of Hamilton & Associates Law Group, P.A. and should not be construed as, and does not constitute legal advice on any specific matter, nor does this message create an attorney-client relationship. Please note that prior results discussed herein do not guarantee similar outcomes. Hamilton & Associates | Securities Lawyers Brenda Hamilton, Securities Attorney 101 Plaza Real South, Suite 202 North Boca Raton, Florida 33432 Telephone: (561) 416-8956 Facsimile: (561) 416-2855 www.SecuritiesLawyer101.com