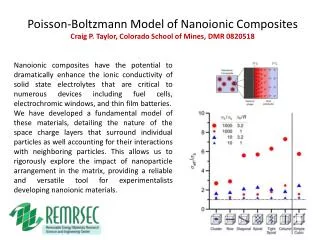

Nadia J Taylor Associate

350 likes | 699 Views

Nadia J Taylor Associate. PRIVATE TRUST COMPANIES Establishing a PTC and Acting as a Registered Representative. A PTC can be either: an IBC; or a Domestic company. HOW IS A PTC ESTABLISHED?.

Nadia J Taylor Associate

E N D

Presentation Transcript

PRIVATE TRUST COMPANIESEstablishing a PTC and Acting as a Registered Representative

A PTC can be either: an IBC; or a Domestic company HOW IS A PTC ESTABLISHED?

The name of a PTC cannot include words such as “Trustee”, “Trust Company” or “Private Trust Company” without the prior approval of Central Bank. INCORPORATING A NEW PTC

Minimum Capital Requirement - $5,000. Specific objects and purposes. Designated Persons or Designated Person. Special Director. Registered Representative. MEMORANDUM AND ARTICLES OF ASSOCIATION

Objects and Purposes of a PTC “to act as trustee only for a trust created or to be created at the direction of a Designated Person or Designated Persons.” MEMORANDUM AND ARTICLES OF ASSOCIATION

A Designated Person(s) is an individual or individuals described as such within the Designating Instrument provided that if more than one each Designated Person must be related to the Designated Person so described by consanguinity or some other family relationship. DESIGNATED PERSON OR PERSONS

A Designated Person may be deceased. The names of the Designated Person(s) will not be a part of the memorandum and articles of association. DESIGNATED PERSON OR PERSONS

A PTC must have one Special Director with: knowledge of trust administration; or five years experience in a discipline relevant to trust administration which includes one or more of law, finance, commerce, investment management or accountancy. SPECIAL DIRECTOR

A PTC is not required to have a Special Director if: a licensee serves as a RR of the PTC. SPECIAL DIRECTOR EXCEPTION

Must be either: A licensee of the Central Bank; or A Financial and Corporate Services Provider (duly licensed under the Financial and Corporate Services Provider Act, 2000). Restricted only to the business of a PTC. WHAT IS A REGISTEREDREPRESENTATIVE (RR)

A RR may provide the services of: Secretary; Director; or Bahamas Agent. Where a RR acts as a Bahamas Agent for a PTC, it must enter into a service agreement to provide administrative services to the company. FUNCTIONS OF A RR

A licensed FCSP wanting to act as a RR must: Apply to the Central Bank for written approval of the Governor to act as a RR; Engage in RR services through a subsidiary company (Regulations 6(1)). REGISTERED REPRESENTATIVE (RR)

The Governor of the Central Bank may approve or deny an FCSP seeking to be a RR based on: The fitness of the FCSP. The business record and relevant experience of the FCSP or its beneficial owners. REGISTERED REPRESENTATIVE (RR)

Whether it has sufficient human and physical resources to act as a RR. The best interest of the financial industry. REGISTERED REPRESENTATIVE (RR)

A RR must be resident in The Bahamas and maintain a minimum share capital of $50,000. The fee payable to the Public Treasury to act as a RR of a PTC is $2,500 annually. REGISTERED REPRESENTATIVE (RR)

A RR is the main point of contact for the Central Bank in relation to PTCs. A RR is required to verify the identities of : the settlor and any person providing the funds or assets which are subject to the trust; REGISTERED REPRESENTATIVE (RR)

The Designated Person; The Protector of any trust in which the PTC is a trustee; Vested beneficiaries of any trust of which a PTC is a trustee. REGISTERED REPRESENTATIVE (RR)

RR must maintain the following books and records at its office in The Bahamas: Memorandum and Articles of Association; Designating Instrument; CV of Special Director; REGISTERED REPRESENTATIVE (RR)

Trust instruments for each trust; A list of all the PTCs of which a RR acts; The “Form of Acknowledgement to be executed by the settlor of the trust ” (to be produced where possible). REGISTERED REPRESENTATIVE (RR)

[INSERT COMPANY NAME] I, [DIRECTOR], hereby confirm that in relation to [INSERT COMPANY NAME] a Company [incorporated/to be incorporated] under the laws of The Bahamas, the Designated Person or Designated Persons for the purposes of Section 2 of the Act shall be: [INSERT INDIVIDUAL (S) NAME (S)]. Signed: DIRECTOR Acknowledged by: [INSERT COMPANY NAME] DESIGNATING INSTRUMENT

I, [INSERT SETTLOR’s NAME], hereby acknowledge that in relation to [INSERT COMPANY NAME] (the “Company”) a company [incorporated/to be incorporated] under the laws of The Bahamas: that the Company’s directors are not required by law to possess or exhibit expertise in trust administration and, therefore, said directors may, in fact, not be possessed of or exhibit such skill, that Company is not required by law to provide any fidelity bond, FORM OF ACKNOWLEDGEMENT TO BE EXECUTED BY SETTLOR OF TRUST

that the capital of the Company is not required by law to exceed Five Thousand Dollars and may, therefore, be minimal; and that Company is not required by law to perform an annual audit. Accordingly, accepting the foregoing and fully understanding the legal implications hereof, I hereby waive any and all rights of complaint in respect of these matters. Signed: Settlor Acknowledged by: FORM OF ACKNOWLEDGEMENT TO BE EXECUTED BY SETTLOR OF TRUST

BTCRA section 3(2): “No trust company shall carry on trust business from within The Bahamas whether or not such business is carried on in The Bahamas unless it is in possession of a valid licence granted by the Governor authorising it to carry on such business.” REQUIREMENT OF A LICENCE

A PTC is exempt from the requirements of section 3(2) of the BTCRA if: The PTC complies with the definition of a “private trust company” under the BTCRA as amended; It has a single Designating Instrument; It does not solicit trust business QUALIFICATIONS OF EXEMPTION

Upon appointment as a RR of a PTC, a RR has a duty to certify to the Governor of the Central Bank that the PTC meets the requirement for exemption from section 3(2) of the BTCRA either: QUALIFICATIONS OF EXEMPTION

Within six (6) months of the date of coming into force of the Regulations; or If a PTC is either an IBC or Domestic Company incorporated after the date of coming into force of the Regulations, within three 3 months of its incorporation. QUALIFICATIONS OF EXEMPTION

A RR certifies exemption by obtaining from the directors of each PTC for which it provides services a duly completed Compliance Certificate in the form set out in the Fourth Schedule to the Regulations. HOW DOES A RR CERTIFY EXEMPTION?

The Certificate should be accompanied by a briefing sheet on each PTC containing the name of the settlor and a list of trusts to be administered by the PTC. A RR must obtain a duly completed Compliance Certificate on, or before 31st December of each year. HOW DOES A RR CERTIFY EXEMPTION?

We, the undersigned directors (the “Directors”) of [COMPANY NAME], a Private Trust Company established under the laws of the Commonwealth of The Bahamas pursuant to the Banks and Trust Companies Regulation Act, 2000 (the “Company”) hereby declare that between [DATE] and [DATE]: 1. The Company has served only as trustee for trust or trusts for Designated Person or Designated Persons or an individual or individuals who are related by consanguinity or other family relationships to the Designated Person or Designated Persons and has not carried on any business or activity which was prohibited; and COMPLIANCE CERTIFICATE

2. The Directors have acted honestly and in good faith with a view to the best interest of the Company. And we each make this solemn declaration conscientiously believing it to be true. ________________ __________________ Director Director COMPLIANCE CERTIFICATE

Establishment and Maintenance of the PTC Fees due on commencement $5,000 Annual Fee $5,000 Registered Office/ Agent $? (discretionary) Establishment of a RR Application to act as RR $2,500 Annual fee. $2,500 APPLICABLE FEES & COSTS

Provision of RR services Fees for acting as: (i) secretary; (ii) director; or (iii) Bahamas Agent. $? (discretionary) Establishment of Trusts Fees for: drafting a trust deed; and $? establishing a trust. $? (discretionary) APPLICABLE FEES & COSTS

Converting an existing IBC or Domestic Company into a PTC. Converting a restricted licence Trust Company into a PTC. Converting an existing Foreign Company into a PTC. OTHER WAYS OF ESTABLISHING A PTC

QUESTIONS? Nadia J TaylorAssociatentaylor@higgsjohnson.com