Download

1 / 5

0 likes | 0 Views

When unexpected bills or emergencies strike u2014 like car repairs, medical costs, or utility payments u2014 some Illinois residents consider payday loans Illinois as a quick way to access cash. But before you commit to one, itu2019s vital to understand what the law allows, how the process works, and how to protect yourself.

E N D

Understanding Payday Loans in Illinois: What You Need to Know When unexpected bills or emergencies strike — like car repairs, medical costs, or utility payments — some Illinois residents consider payday loans Illinois as a quick way to access cash. But before you commit to one, it’s vital to understand what the law allows, how the process works, and how to protect yourself. What Are Payday Loans? A payday loan is a short-term, high-cost loan designed to be repaid when your next paycheck arrives. Generally, you borrow a small amount, pay a fee or interest, then repay in a lump sum (or via postdated check or authorization for electronic withdrawal). The idea is that it’s a stopgap until your next pay. In Illinois, however, the landscape for payday lending has changed significantly in recent years. While traditional payday loans are heavily regulated (or restricted) under state law, many lenders now offer installment-style loans or small consumer loans under the same rules that apply to payday-style lending. Thus, if someone searches for payday loans Illinois, what they really need is to understand what is legal today, what protections exist, and what alternatives might be safer.

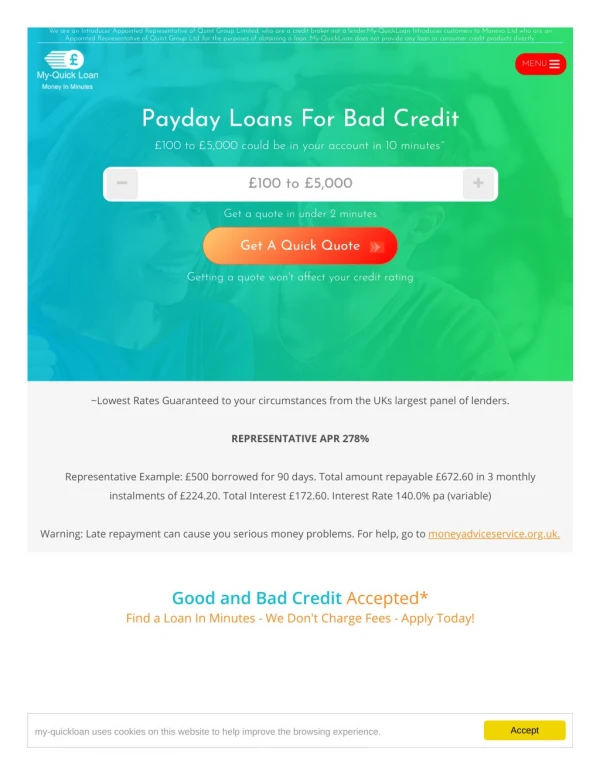

Legal Framework: What Illinois Law Says Illinois has enacted strong consumer protections regulating or limiting payday lending. Here are the key features of those laws: 1. 36% APR Cap (All-in Limit) In March 2021, Illinois passed the Predatory Loan Prevention Act (PLPA), which applies an “all-in” interest rate cap of 36% APR on most consumer loans (including payday-style and installment loans). Any contract exceeding that rate is considered void. Thus, when people look for payday loans Illinois, they should expect that the effective annual cost must not exceed 36%. 2. Term Limits and Indebtedness Periods Under earlier laws (Payday Loan Reform Act) and still relevant in oversight, payday loans had minimum terms (e.g. 13 days) and maximum consecutive indebtedness durations. For example: •A loan must have a minimum term of 13 days. •A borrower cannot be in continuous indebtedness for more than 45 consecutive days under payday loans. •After such period, the borrower must wait at least 7 calendar days before obtaining another payday loan. 3. Loan Amount Limits & Payment Caps Illinois law prohibits making a payday-style loan if it would cause the total payments due in a month (including other outstanding payday loans) to exceed either $1,000 or 25% of a borrower’s gross monthly income, whichever is less. This prevents loans that impose excessive monthly burdens. 4. No Rollovers or Renewals Rollovers—extending a loan or refinancing a pending balance—are not allowed in Illinois. Lenders cannot legally extend your due date or roll over your balance with additional fees. 5. Right to Repayment Plan After 35 Days If a payday loan remains outstanding after 35 consecutive days, the borrower is entitled to demand an interest-free repayment plan. This gives at least 55 days (with no additional fees or interest) to repay in installments. The plan must have at least 4 installments, spaced no less than 13 days apart, and cannot exceed a total repayment period of 90 days. 6. Additional Restrictions & Protections •Lenders may not take an interest in your personal property to secure a payday loan.

•If you prepay any portion, you should have no penalties. •In case of insufficient funds for a payment, the lender may charge a fee (capped at $25) but only one such fee per check or debit. •If a contract violates the law (e.g. exceeds the 36% cap), it’s void: the lender cannot legally collect the principal, fees, or interest. Because of these changes, the traditional “payday loan” product has been curtailed in Illinois, and many lenders now offer consumer installment loans subject to the same 36% cap and protections. The State of “Payday Loans Illinois” Today Because of the 2021 reforms, many high-cost “payday loan” products have effectively been eliminated in Illinois. The law forced many lenders who previously charged very high rates or used short-term rollovers to either exit the state or reformulate their loan products under the new 36% ceiling. Key current features: •Many lenders now issue installment loans rather than one-time payoff loans. •The maximum interest rate across such small consumer lending is capped at 36% APR. •People seeking payday loans Illinois may find that traditional short-term cash advance products are no longer offered legally. •Illinois regulators have seen many high-cost lenders surrender their licenses post- reform, reducing the number of bad actors. Thus, consumers should be wary of any lender advertising “payday loans Illinois” that promises very high interest, rollovers, or terms that violate the legal caps — such offers may be unlawful or predatory. Pros & Cons: Is a Payday/Small Consumer Loan Wise? Pros •Fast access to funds: For emergencies, a small consumer or installment loan can provide needed cash quickly. •Transparency: With the 36% cap and legal requirements, you can know in advance exactly what your cost will be.

•Protected under law: Illinois law offers repayment plan rights and prevents rollovers, reducing the risk of debt spirals. Cons & Risks •High relative cost: Even 36% APR is expensive compared to many longer-term loans or credit cards with lower rates. •Recurring borrowing temptation: If you can’t handle the payment, you may seek another loan, which compounds risks. •Unlicensed or illegal lenders: Some companies may advertise high-cost payday loans ignoring Illinois law; deals that exceed legal terms are void and risky. •Strain on cash flow: Even a legal loan might still stress your monthly budget if not carefully planned. Because of these cons, such loans should be a last resort — not a routine financing method. How to Safely Use a “Payday-Style” Loan in Illinois If you are considering what’s advertised as a payday loan Illinois, follow these safety steps: 1.Check legitimacy and licensing Ensure the lender has a valid license to operate under Illinois consumer lending rules. 2.Ensure the total APR ≤ 36% If the total cost of your loan (interest, fees) exceeds 36% APR, it may be invalid. 3.Avoid rollovers or extensions Do not agree to any renewal, refinancing, or extension — these are illegal under Illinois law. 4.Request a repayment plan if needed If repayment is delayed beyond 35 days, you’re legally entitled to a no-interest installment plan over 55 days. 5.Carefully review all terms Get written disclosures: principal amount, total cost, repayment schedule, and any fees. 6.Limit your borrowing Borrow only what you absolutely need and that you can realistically repay on time. 7.Avoid predatory offers If the lender pressures you, hides terms, or demands unusual fees, walk away.

Alternatives to Payday Loans in Illinois Before going the loan route, explore these safer options: •Credit union microloans or small-dollar loans: Many credit unions offer small personal loans at far lower cost. •Installment or personal loans from banks or online lenders: With longer repayment periods, the cost burden per payment is less. •Borrowing from family or friends: If possible, this can avoid interest or protect you from legal risk. •Community assistance or nonprofit programs: Local nonprofits or charities may help with emergency bills. •Budget adjustment or delaying nonessentials: Cutting expenses or restructuring can sometimes bridge the gap. Often, these alternatives cost less and carry less risk than short-term expensive loans.