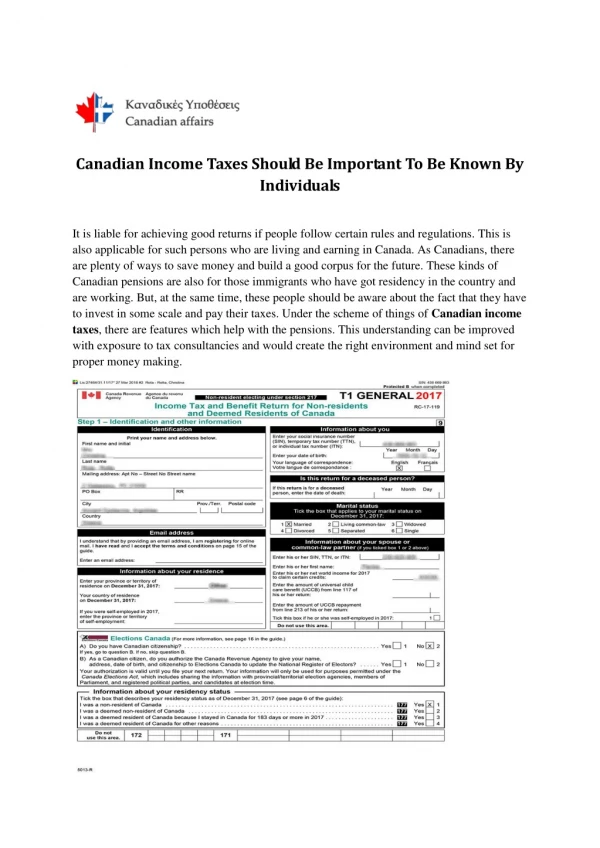

Download

1 / 38

380 likes | 920 Views

OREGON INCOME TAXES. Personal Income Tax. Corporate Excise Tax. Surplus Kicker. Proposed Legislative Tax Changes. Oregon Income and Property Taxes. General Fund Revenues. 1999-01 Biennium: Total $10.1 billion. 2001-03 Biennium: Total $9.2 billion. ($ 755 million). ($ 395 million).

E N D

OREGON INCOME TAXES Personal Income Tax Corporate Excise Tax Surplus Kicker Proposed Legislative Tax Changes

General Fund Revenues 1999-01 Biennium: Total $10.1 billion 2001-03 Biennium: Total $9.2 billion ($ 755 million) ($ 395 million) ($ 8.7 billion) ($ 8.1 billion)

OREGON INCOME TAXES Personal Income Tax

Oregon Personal Income Tax Federal Adjusted Gross Income + • Oregon Additions: • Interest on non-Oregon bonds... - • Oregon Subtractions: • Federal income tax up to $3250... - • Deductions • Standard either: Itemized • $1,640 single • $3,280 joint = Oregon Taxable Income

TOP FIVE OR SUBTRACTIONS–Tax Year 2000: Total Full-Year Subtractions = $5.1 billion SUBTRACTION $ Amount (millions) • Federal Income Tax $2,415 • Social Security Income $1,104 • Federal Pension Income $ 719 • Oregon Tax Refund $ 345 • Interest from U.S. Bonds $ 306

TOP FIVE FEDERAL ITEMIZED DEDUCTIONS– Tax Year 2000: Total Full-Year Deductions = $9.1 billion DEDUCTION $ Amount (millions) • Home Mortgage Interest $ 3,862 • Property Taxes $ 1,065 • Other charitable contributions $ 1,048 • Medical and Dental Expenses $ 693 • Charitable contributions: Education $ 215

Oregon Personal Income Tax Oregon Taxable Income x Tax Rates = Tax Before Credits - • Tax Credits • $145 personal credit... = TAX

TOP FIVE OR CREDITS –Tax Year 2000: Total Full-Year Credits= $423 million CREDIT $ Amount (millions) • Personal Exemption $ 361 • Tax Paid to Other States $ 17 • Earned Income $ 10 • Working Family $ 7 • Child Care $ 6.6

Income Tax Credits 2000: $422.6 million

Income Tax Rate and Credit Rate by Income 2000 Returns

Distribution of Tax Returns Total 2000 Returns: 1.6 million Total 1990 Returns: 1.3 million

Components of AGI 1990: $35 billion

Components of AGI 2000: $66 billion (full-year returns)

Change in Major Components of AGI- Tax Year 2000 and 2001* * Preliminary Data as of Dec. 2002

Distribution of AGI Components 2000 AGI: $66 billion (full-year returns)

Average AGI 2000 Average AGI: $43,615 1990 Average AGI: $26,610

Average AGI By County - 2000 Polk 40,853 Statewide Avg. AGI = $43,165 $0 to $29,999 $30,000 to $40,000 $40,000 to $50,000 Above $50,000

Average Tax by County - 2000 Columbia Statewide Avg. Tax = $2,416 $0 to $1,499 $1,500 to $1,999 $2,000 to $2,499 Above $2,500

Average Tax by County - 1990 Statewide Avg. Tax = $1,404 $0 to $1,499 $1,500 to $1,999 $2,000 to $2,499 Above $2,500

Number of Tax Returns:Tax Withheld, Estimated Payments & Refunds - 2000

Tax Withheld, Estimated Payments & Refunds - 2000 Total Tax Due: $4.2 billion

Breakdown by Industry and Month of Tax Withholdings Index – 1998-2002

Industry Sectors With a Decline in Withholdings Between July 2001 and Nov. 2002 TOTAL -$238,111

Part Year and Nonresident Taxpayers State has nexus to tax income earned by residents and income from Oregon sources earned by nonresidents. Applies to: Full Year Residents Part Year Residents • lived in Oregon but moved out • lived elsewhere but moved to Oregon Nonresidents • absentee landlord • commute from Vancouver, WA

Part Year and Nonresident Taxpayers Example: Total Income Less: Exempt Income Plus: Additions Less: Subtractions Adjusted Gross Income Federal $20,000 1,000 500 200 $19,300 Oregon $5,000 0 0 50 $4,950 Oregon percentage ($4,950/$19,300) = p = 25.65%

Part-Year Resident $19,300 - 7,250 12,050 923 237 - 36 $201 Federal AGI Less: Deductions 5,000 Federal Tax 2,250 Total Deductions Taxable Income: Tax before credits: Multiply by p Less Credit ($145) x p TAX DUE

Nonresident $4,950 - 1,860 3,090 170 - 36 $134 Oregon AGI Less: Deductions 5,000 Federal Tax 2,250 Total 7,250 Multiply by p Taxable Income: Tax before credits: Less Credit ($145) x p TAX DUE

Check-off Donations Total (2000) = $585,000

SURPLUS KICKER&POTENTIAL CHANGES in Federal and State Income Tax Laws

2% Kicker At the end of a biennium if …... exceed COS estimate by 2% or more…. Entire excess is credited to CORP Taxpayers 1. CORP Income Tax Revenues 2. Other General Fund Revenues exceed COS estimate by 2% or more…. Entire excess is refunded to PI Taxpayers

Measure 28 • Passed during 5th special session • Increases top personal income tax rate to 9.5% • Increases the corporate tax rate to 6.93% • Increases tax rates for 3 years beginning tax year 2002 • Average tax increase is $114 per year • Raises $313 million in 2002-03 fiscal year • Raises $414 million in 2003-05 biennium

Bush’s Proposed Economic Recovery Plan • Eliminate double taxation on dividends • Accelerate the 10% federal tax bracket expansion • Accelerate the reduction in income tax rates • Accelerate the reduction of the marriage penalty • Increase Federal child care credit by $400 • Increase business expensing threshold • Provide similar tax relief to alternative minimum tax returns

DIVIDEND INCOME AND NUMBER OF RETURNS Statewide – Tax Year 2000 Dividend Income = $1.5 billion Number of Returns w/Dividends = 388,461 Total Dividend Estimated Tax = $105 million