Download

1 / 19

190 likes | 219 Views

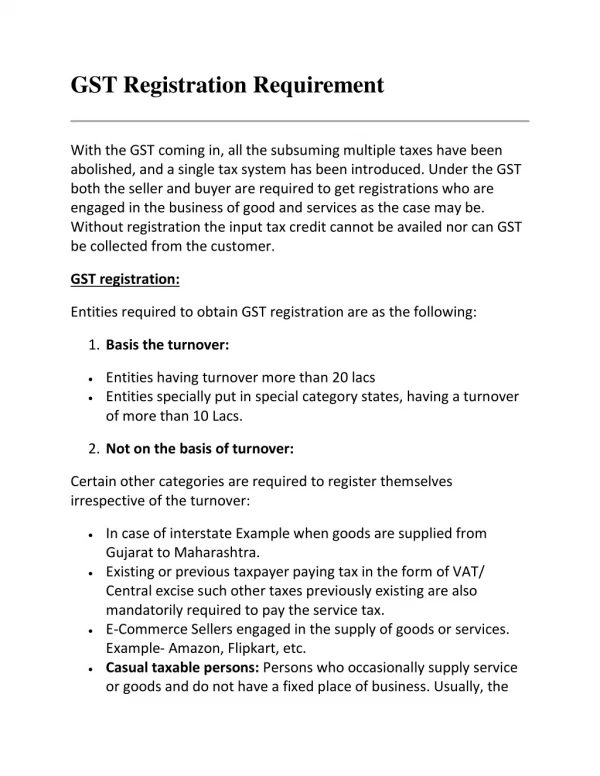

The concept of casual taxable person has their own relevance under the GST law. Any person who is a casual taxable person and who is making any taxable supply shall be requiring taking GST registration. <br><br>In other words, if any casual taxable person is making non taxable supply then in that case he shall not fall under this clause and mandatory GST registration shall not be applicable.<br><br>Meaning of Casual taxable Person<br><br>“Casual taxable person” means a person who occasionally undertakes transactions involving supply of goods or services or both in the course or furtherance of business, whether as principal, agent or in any other capacity, in a State or a Union territory where he has no fixed place of business.<br><br>In other words, a person registered in Delhi, supplying goods from Haryana where he do not have any fixed place of business, then GST registration for that person shall be mandatory.<br>

E N D

Practical GuideonGST Registration for Casual taxable Person By CA Paras Mehra

A word from the Author Casual Taxable Person is a very old concept and has been extended under Goods and Services Tax (GST). The concept of casual taxable person is important for those entities or business who does not have any fixed place of business in other state. Hence, it is become important to understand the concept of casual taxable person under GST. In case you have any query regarding GST or company registration, kindly drop an email to paras@hubco.in and I would be more happy to answer. Best Wishes CA Paras Mehra

Introduction to Casual taxable Person The concept of casual taxable person has their own relevance under the GST law. Any person who is a casual taxable person and who is making any taxable supply shall be requiring taking GST registration. In other words, if any casual taxable person is making non taxable supply then in that case he shall not fall under this clause and mandatory GST registration shall not be applicable.

Meaning of Casual taxable Person “Casual taxable person” means a person who occasionally undertakes transactions involving supply of goods or services or both in the course or furtherance of business, whether as principal, agent or in any other capacity, in a State or a Union territory where he has no fixed place of business. In other words, a person registered in Delhi, supplying goods from Haryana where he do not have any fixed place of business, then GST registration for that person shall be mandatory. Clause 20 of Section 2 of CGST Act

Logic behind the Casual taxable Person • GST registration is state wise and hence there may be a situation where a person who is registered under one state may also require registering under another state but only for few days. Further, he also does not have any other fixed place of business from where he can take GST registration. • Therefore, the concept of casual taxable person shall help that entire person who does not have any fixed place of business but they are liable to register under GST from that state. Contd.

Practical Example • Example: • Trade fair in Pragati Maidan Delhi, where many dealers comes from across India to sell their specialty however, since they are supplying goods/services from Delhi for few days only, hence it may not be feasible for them to apply for normal registration. • Hence, this person can take registration as a casual taxable person. Casual taxable person can be a company, firm, individual etc.

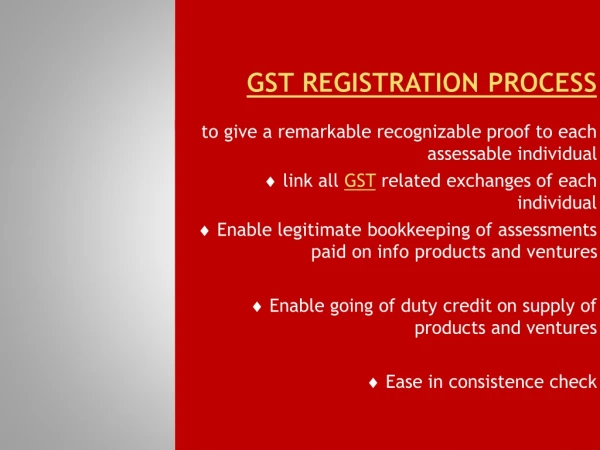

1 Gather all documents The first step for GST registration is to gather all documents in scan form in your computer. Following is the list of basic documents requirement: PAN Card of the firm Passport size photo Registration documents Authorisation letter Copy of Cancelled Cheque Address proof like Elect bill Now proceed to step 2

2 Create TRN and Login The second step is to visit the gst.gov.in and click on new user registration, then after that a TRN number is generated, based upon which you can create the log in and proceed. While creating the login, make sure you enter valid mobile and email. This is because the GST registration is authenticated using the OTP on the respective mobile number and email. Now proceed to step 3

3 Prepare the GST REG - 01 • The GST registration shall be applied via form GST REG 01 where person needs to select the appropriate category i.e. Casual Taxable Person, if he is covered under the definition as discussed above. • He needs to enter certain other details as well like estimated turnover, period of registration etc. Now proceed to step 4

4 Calculate estimated Tax Liability Once you choose the category of Casual Taxable Person, you need to calculate the estimated tax liability based upon the estimated revenue. Whatever, is the tax liability, it must be paid in advance. Further, whatever is paid, then adjusted against the actual tax liability. Further, advance paid can be tracked in Electronic Cash Ledger. Now proceed to step 5

Practical Example in step no.4 Example: Mr. A wants to register as a casual taxable person in the state of Delhi. He wants to participate in an exhibition which will last for 40 days. During the tenure of 40 days, he expects the turnover of Rs.50 lakh. Solution: The total expected turnover is Rs.50 lakh and the tax rate is 18%. Therefore total estimated tax liability is Rs.9 lakh (CGST plus SGST). Therefore, Mr. A needs to make an advance deposit of Rs.9 lakh before the tax authorities to get the GST registration.

5 Registration time limit The online GST registration for Casual Taxable Person is granted for a maximum period of ninety days. However, if any extension is sought for additional number of days, then the registration may be extended to further 90 days. In total, the time period shall be 180 days (90 + 90). Proceed to Step no.6

6 GST Registration is granted Once all the additional formalities are done, GST registration is granted by the authorities. However, sometime, the GST inspector may issue certain objections which are to be clarified by the taxpayer. Once the clarification are accepted by the GST inspector, the GST registration details are issued over the email directly to the applicant. Registration Complete

Download the Registration Certificate Once the GST registration is granted, the taxpayer can download the GST registration certificate in form GST REG 06. All the activity relating to GST can be tracked online in your GST account. Once the GST registration is granted, you need to issue tax invoice for each supply made of goods or services or both.

Thank You very much for the time! GST Registration Online In case you have any issues, please email us at info@hubco.in or visit our website, www.hubco.in.

A Presentation by Hubco.in A entity owned and controlled by Hubco Technologies Private Limited +91 9953523014 II +91 8130502049 II info@hubco.in