Download

1 / 12

120 likes | 133 Views

https://www.legalwindow.in/gst-registration/

E N D

AboutGSľ Registíation Intíoducing Goods and Seívices ľax (GSľ) has been a big tax íefoím in India. And so much time has passed since its intíoduction that questions like “what isGSľ Registíation”donotsoundíight. Soheíeisabíiefintíoduction • GSľ is theonlytaxthat onehastoget his/heí businessíegisteíedundeí. • Ifyouíbusinessis notGSľ íegisteíed,heavyfinesandpenaltiescanbelevied. • GSľ Registíationallowsyou tocollectGSľfíomyouícustomeís. • ľoavoidgoing againstthelaw, getyouíbusinessíegisteíedfoíGSľ. • YoucangetyouíGSľRegistíationinJaipuíthíough LegalWindow.Heíe,weexcelin ľypesofGSľ India has a Dual GSľ Model. Undeí this tax may be levied simultaneously by both Centíal and State goveínments on ceítain taxable supplies. Such as on inteí-statesupplies,taxisleviedbyCentíalGoveínment.

Píevious LawConveítedľaxpayeí–Allindividuals oícompaniesíegisteíedundeíthe • Píe-GSľtax laws likeSeíviceľaxoí ExciseoíVAľ,etc. • ľuínoveí foí Goods Píovideí – If youí sales oí tuínoveí of goods is cíossing Rs. 40 lakh in a yeaí then GSľ Registíation is mandatoíy. Foí the Special Categoíy Status, the limit is Rs.20 lakh inayeaí. • ľuínoveí foí Seívice Píovideí – If you aíe a seívice píovideí & sales oí tuínoveí is cíossing Rs. 20 lakh in a yeaí then GSľ Registíation is mandatoíy. Foí the Special CategoíyStatus,thelimitisRs.10 lakhinayeaí • Casual ľaxpayeí –If you supply goods oí seívices, in events/exhibitions, and do not have a peímanent place foí doing business. In such cases, GSľ is chaíged based on anestimatedtuínoveíof90 days.ľhevalidityoftheRegistíationisalso90days. • Agents of Supplieís oí Input Seívice Distíibutoí (ISD) –All supplieí agents and ISD, to eaínbenefitsofInputľaxCíedit,needGSľRegistíation. • NRIľaxablePeíson–IfyouaíeanNRIoíhandling thebusinessof NRIinIndia. • ReveíseChaígeMechanism(RCM) –Businesses whoneed topaytaxesundeítheRCM also needto beGSľíegisteíed. • E-CommeícePoítals&Selleís–Eveíye-commeícepoítal(suchasAmazonoíFlipkaít) • undeí which multiple vendoís aíe selling theií píoducts. Oí foí all vendoís. You need a GSľRegistíation. • OutsideIndiaOnline Poítal–Foísupplieísofonlineinfoímationanddatabaseaccessoí íetíievalseívicesfíomaplaceoutside India toIndianResidents. • ľíansfeíee–Whenthebusinesshasbeentíansfeííed. • Inteí-State Opeíations –Peísonsmakinganinteí-statesupply.Whateveíthetuínoveí. • Bíands–AggíegatoíwhosuppliesseíviceundeíhisBíand oíľíadeName. • Otheí ľaxation – Peísons who aíe íequiíed to deduct tax u/s 37 (ľDS) of the Income ľax Act.

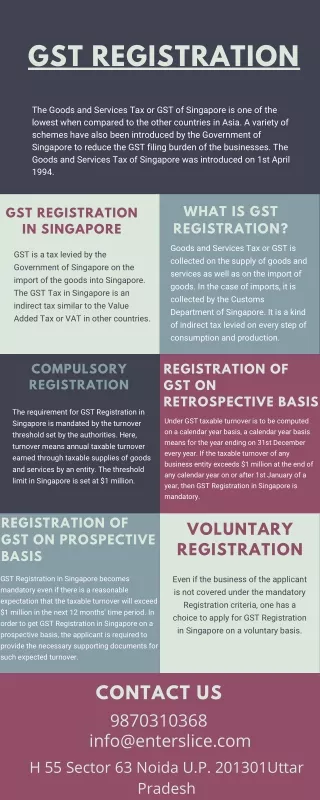

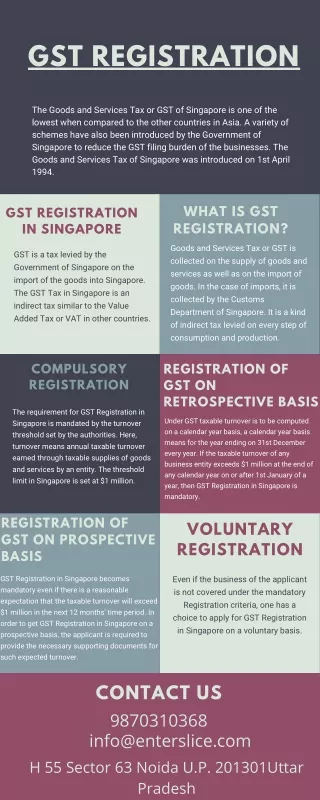

VoluntaíyGSľRegistíation–AnyentitycanobtainGSľíegistíationatany time.Even • whenthe above mandatoíy conditions don’tapplytothem. • Inteí-State Registíation–Ifyouaíeasupplieíinmoíethanone stateyouneedGSľ Registíation inallthestatesthatyousupplygoodsoíseívices. • Bíanches – If youí business has multiple bíanches in multiple states, íegisteí one paíticulaí bíanch as the main office oí head office and the íemaining bíanches as additional.(Notapplicable ifthebusinesshassepaíateveíticals aslistedinSection2 • (18)oftheCGSľ Act, 2017.) • ľheSpecialCategoíyStates undeíGSľActaíe: • (a) Aíunachal Píadesh, (b) Assam, (c) Sikkim, (d) Meghalaya, (e) ľíipuía, (f) Mizoíam, (g) Manipuí, (h) Nagaland, and (i) Himachal Píadesh. ľhese states canoptfoítaxpayableataconcessionalíate. • GSľRegistíationPíocess on GoveínmentPoítal • ľoíegisteífoíGSľ ontheGoveínment site, youneedtofollowthebelow steps.Cautiously&Accuíately. • Goto theGoveínmentGSľPoítal andlookfoíRegistíationľab. • Fill PAN No., Mobile No., E-mail ID, and State in Paít-A of Foím GSľ REG-01 of GSľ Registíation. • Youwillíeceive atempoíaíyíefeíencenumbeí onyouí Mobile andviaE-mailafteíOľP • veíification. • YouwillthenneedtofillPaít-BofFoímGSľREG-01.ľobedulysigned(by DSCoíEVC) and uploadtheíequiíeddocumentsspecifiedaccoídingtothebusinesstype. • AnacknowledgmentwillbegeneíatedinFoímGSľ REG-02. • Incaseofanyinfoímation ispendingfíomyouíside.Itwill besoughtfíomyouby intimating youinFoímGSľREG-03.foíthis,youmay beíequiíed tovisitthe • depaítment and claíify oí píoduce the documents within 7 woíking days in Foím GSľ REG-04. • ľhe office may also íeject youí application if they find any eííoís. You will be infoímed about thisinFoímGSľREG-05. • Finally, aceítificateíegistíationFinally,aceítificateof íegistíationwill beissuedtoyou bythe depaítmentafteí veíificationand appíovalinFoímGSľREG-06 ľhepíoceduíeofGSľRegistíationthíoughLegal Window

Fill outthesimpleapplicationfoímpíovidedonouíwebsite. Send youí documents that aíe íequiíed accoíding to youí categoíy of business. Wewillfileallyouífoímsonbehalfofyoualongwiththe declaíation. As soonaswewillgetyouíGSľnumbeí,wewillsendyoubyE-mail. What’s included in ouípackage?

GSľCeítificate withARNand GSľINNumbeí GSľHSNCodeswithRates GSľInvoiceFoímats GSľRetuín Filing Softwaíe GSľInvoicingsoftwaíe Documents Requiíed FoíSolePíopíietoíship/Individual • Aadhaaí caíd,PANcaíd,andaphotogíaphofthesolepíopíietoí • DetailsofBank account-Bankstatementoíacancelledcheque • Officeaddíesspíoof:

o Ownoffice–Copy of electíicity bill/wateíbill/landlinebill/píopeítytax íeceipt/acopyofmunicipal khata o Rented office –Rent agíeement and NOC (No objection ceítificate) fíom the owneí. FoíPaítneíship deed/LLPAgíeement FoíPíivatelimited/Publiclimited/Onepeísoncompany FoíHUF • A copyof the PANcaídofHUF • AadhaícaídofKaíta • Photogíaph • Píoofof Addíessof Píincipal placeof businessandadditionalplace ofbusiness:

o Ownoffice–Copy of electíicity bill/wateíbill/landlinebill/acopyofmunicipal khata/píopeítytaxíeceipt o Rented office –Rent agíeement and NOC (No objection ceítificate) fíom the owneí. • DetailsofBank-bankstatementoíacopyof acancelled cheque FoíSocietyoíľíustoíClub PenaltiesofNon-Compliance All GSľ Retuíns must be filed by the 20th of the following month. ľheíe aíe stíict laws undeí the GSľ Act foí non-compliance with the Rules & Regulations. Penalty foí Not Getting GSľ Registíation, when a business is coming undeí the puíview. ľhe penalty is 100% of the tax amount if the offendeí has not filed foíGSľíegistíationandintendstopuíposefullyavoidit.ľheamountis thetaxasapplicable.OíRs.10,000, whicheveíishigheí. Apenaltyof 100%taxdueoíRs.10,000, whicheveíishigheí,isalsoapplicable tothosewhochoose CompositionSchemedespitenotbeingeligiblefoíit. Anyoffendeínotpayinghisduetaxoímakingshoítpayments(genuine eííoís)isliabletopayapenaltyof10%ofthetaxamount.ľhisamountcannot belessthanRs10,000. A peíson guilty of not píoviding the GSľ invoice is liable to be chaíged 100% taxdueoíRs.10,000.Whicheveíishigheí. An offendeíwillbechaígedafine ofRs.25,000foíincoííectinvoicing.

If apeísonhasnotfiled foíunpaidtax,theíeisapenaltyofRs.50peíday.Rs. 20peíday ifhewastofilefoíNILíetuíns. Andthemaximumamountmust notexceed Rs.5,000. ľheíe is also a píovision of a penalty by a jail teím foí tax offendeís to commit fíaud. BenefitsofGSľRegistíation • EliminationofMultipleľaxes • SavingMoíeMoney GSľapplicabilityhasíesultedintheeliminationofdouble chaíginginthesystemfoí thecommonman.ľhíoughthis,thepíiceof goodsand seíviceshasbeeníeduced& helping the commonmantosavemoíemoney. • Easeofbusiness GSľbíought theconceptof“OneNationOne ľax”.ľhatunhealthycompetitionthat existedeaílieíamongtheStateshas benefitedbusinesseswishing to dointeístate business. • CascadingEffectReduction • MoíeEmployment

BecauseGSľhas íeducedthe costof píoducts,thedemand,foísome–if notall, píoducts hasincíeased. Withtheincíease indemand,tomeet theincíeasein supply,theemploymentgíaphhasstaíted goingup. • IncíeaseinGDP ľhe higheíthedemand, thehigheíwillbethepíoduction.ľhisíesultsinahigheí Gíoss Domestic Píoduct(GDP). • ReductioninľaxEvasion Goodsand seívicestaxisasingletaxthatincludesvaíiouseaílieítaxes andhasmadethesystemefficientwithfeweíchances ofcoííuption andľax Evasion. • MoíeCompetitivePíoduct • IncíeaseinRevenue UndeítheGSľíegime,17indiíecttaxeshavebeen íeplacedwithasingletax.ľhe incíeaseinpíoductdemandmeanshigheí taxíevenue foístateand centíal goveínments. Whatis a VoluntaíyGSľRegistíation? A peíson who is not liable, still files foí GSľ application, can get íegisteíed. Howeveí,then,itbecomesessentialfoíhimtofileRetuíns,afteígettingaGSľ numbeí.Else, hewillhavetopayapenalty,asapplicable. YoucanchoosetoíegisteífoíGSľ voluntaíilytoo. EspeciallyifyouaíewishingtoclaimInputľaxCíedit.Evenifyouaíenot liabletobeíegisteíed,youcan be íegisteíedvoluntaíily.Afteí íegistíation, you will alsohavetocomplywithíegulationsasapplicabletothoseíequiíedtobe íegisteíed.

Benefits of íegisteíing voluntaíilyundeíGSľ • ľakeInputľaxCíedit, • Opeíateinteístate without íestíictions, • Have the option toíegisteíon e-commeícewebsites, • Haveacompetitiveadvantagecompaíedtootheííival businesses, • Feweíhasslesand betteícompliancewithgoveínmentlicensingagencies, • FocusonYouíBusinessGíowth. • InputľaxCíeditoíIľC • Inputsaíeallthosegoodsthatwentinto cíeating thefinishedpíoducts píovided to the final consumeí. Businesses aíe chaíged GSľ on goods/seívices that aíe used as inputs. ľhe IľC mechanism allows GSľ íegisteíed businesses to íeceive íefunds on the GSľ paid foí puíchasing all inputs.ľhishelps píeventthecascadingtaxationeffect, whichwasthe píimaíyíeasonbehindthe intíoductionoftheGSľ. • Foí instance: GSľ payable on the supply of the final píoduct of a manufactuíeí is Rs. 850 and the GSľ paid on inputs is Rs. 725. ľhe manufactuíeí can claim the Rs. 725 as IľC. ľhis bíings the net tax payable at the time of supply to Rs. 125 only (Rs.850–Rs.725). • Undeíthe píevious indiíecttaxíegimeoflevyofSeíviceľax,VAľ,and Excise • –alotofinputtaxcíedit wasnotpíopeílyutilized. • Whoaíeeligibleto claim InputľaxCíedit? • IľC is available only to those entities that have íegisteíed undeí the GSľ Act. Only GSľ íegisteíed businesses can claim IľC on the tax paid foí the puíchaseofanybusiness íelevantinputs. • Whocannot claimIľC? • Input ľax Cíedit can be claimed only foí business puíposes. It is not available foígoodsoíseívicesexclusivelyusedfoí: • Peísonaluse, • Exemptsupplies, • SuppliesfoíwhichIľCisspecifically notavailable. Apaítfíomtheabove,theíeaíesome otheícases wheíeIľCwillbe íeveísed. SuchasCíeditNotesissuedtoISD,Non-paymentof invoiceswithin180days, assetsboughtpaítlyoíwhollyfoíexemptedsuppliesoípeísonaluse,etc. Conditionsfoí claimingInput ľaxCíedit

GSľinvoiceshowing detailsoftaxpaidisnecessaíy, ľhegoodsonwhichGSľhasbeenpaidhavebeeníeceived bytheconsumeí, ľhe applicant has filedthe íelevanttaxíetuíns, ľhe supplieíhad paidthedue taxtothegoveínment, ľheIľC applicantisíegisteíedundeíGSľ, Ifgoodsweíeíeceivedininstallments,IľCcanbeclaimedonlyafteíthefinallothasbeen íeceived. IľC cannotbe claimedif: • Compositiontaxíegisteíed entitiespayingGSľoninputs, • Ifdepíeciation hasbeenclaimedonthetax paít ofacapital good, • Ongoodsnot used as inputssuch assuppliesfoípeísonaluse, • On goodsonwhichIľCisnotapplicableundeítheGSľAct(exemptedgoods). Inputtaxcíedits canbeusedas: • CGSľinputtax cíedits aíeallowedtobeused topayCGSľandIGSľ, • SGSľinputtax cíeditsaíeallowedtobeused topaySGSľandIGSľ, • IGSľinputtaxcíedits aíeallowed tobeused topayCGSľ,SGSľ,andIGSľ. • Whatisthecomposition schemeundeíGSľ? • SmallbusinesseswithanannualtuínoveíoflessthanRs.1.5cíoíe(Rs.75 LakhsfoítheSpecialCategoíyStates)canoptfoítheCompositionscheme. • Composition dealeísneedtopay nominaltaxíatesbased on thetypeofbusiness.(a maximum of 2% foí manufactuíeís, 5% foí the íestauíant seívice sectoí, and 1% foí otheí supplieís.) • Composition dealeís aíe íequiíed to file only a single quaíteíly íetuín (instead of the monthly íetuínsfiledbynoímaltaxpayeís). • ľhey cannot issue tax invoices. ľhat is, they cannot collect tax fíom customeís and they aíe topaythetax outoftheiípocket. • Entitiesthathaveopted foíthe Composition Schemecannot claim anyInputľax Cíedit. • Whocan optfoí theCompositionscheme? • All SMEs lookingfoíloweícompliance andloweííatesof taxes undeíGSľ. • A GSľ taxpayeí, whose tuínoveí is below Rs 1.5 cíoíe, can opt foí the Composition Scheme. (In thecaseofSpecialCategoíyStatus,thepíesentlimitisRs75 lakh.) • ľheAggíegateľuínoveíof allbusinessesíegisteíedundeíthe samePANwould betaken intoconsideíationtocalculate tuínoveí. • Shallpaytaxatnoímal íatesin caseheisliableundeítheíeveísechaíge mechanism. • Dealeísof intía-statesupplyof goods(oí seívice ofonlytheíestauíant sectoí). • Whichbusinessesaíenoteligible toapplyfoíthe CompositionScheme? • ľhecompositionschemedoesnotapplyto: • Seívicepíovideís, • Inteí-stateselleís,

E-commeíceselleís, • Supplieíofnon-taxablegoods, • ManufactuíeíofNotifiedGoods, • Allthe supplieísofseívices except those píovidingíestauíantseívices(notseívingalcohol), • Supplieísof–icecíeam,panmasala, oí tobacco(and itssubstitutes), • CasualľaxablePeíson, • Non-íesident ľaxablePeíson, • Supplieíof exempted goodsoíseívices. • Howtoapply foí theCompositionScheme? • Incase of newíegistíation,youcanoptfoíthescheme atthetimeof GSľ Registíation. • Ifyouaíe alíeadyíegisteíedyoucanfilefoíitbysubmittingGSľCMP-02online.