Download

1 / 41

420 likes | 924 Views

Developing Your Asset Allocation Strategy for Retirement. Developed by Barbara O’Neill, Ph.D., CFP, Rutgers Cooperative Extension Adapted by Jean Lown, Ph.D. Family, Consumer & Human Development Lown@cc.usu.edu. Overview . Asset Allocation Principles Risk-Return Relationship

E N D

Developing Your Asset Allocation Strategy for Retirement Developed by Barbara O’Neill, Ph.D., CFP, Rutgers Cooperative Extension Adapted by Jean Lown, Ph.D. Family, Consumer & Human Development Lown@cc.usu.edu

Overview • Asset Allocation Principles • Risk-Return Relationship • Application to TIAA-CREF Retirement Investment Options • 9 new investment choices (as of 2003)

What Is Asset Allocation? • Process of diversifying portfolio investments among several investment categories to reduce investment risk • Example: 50% stock, 30% bonds, 10% real estate, 10% cash assets • Objective: lower investment risk by reducing portfolio volatility • Loss in one investment may be offset by gains in another

The Callan Periodic Table of Investment Returns • http://www.callan.com/resource/periodic_table/pertbl.pdf • Illustrates the need for asset allocation • Shows how various asset classes performed during the last 20 years • Best performing asset class changes • One year’s “winner” can be next year’s “loser,” so invest in a variety of assets

Why Asset Allocation? Because Market Timing is Futile • Value of $100 invested in large company stocks (S&P 500 index) from June 1980 to June 2000: • $2,456 stayed invested entire time • $613 if you missed the best 15 months • Biggest market gains are often concentrated in short periods (can’t afford to miss)

Second Example: The Futility of Market Timing • Based on S&P 500 stock market index • If investor stayed fully invested, return was 41.4% • If investor missed top 10 trading days of 1998, 1999, and 2000: -41.7% return • Moral: stay invested in both bull & bear markets

Determinants of Portfolio Performance Source: “Determinants of Portfolio Performance II, An Update” by Gary Brinston, Brian D. Singer and Gilbert L. Beebower, Financial Analysts Journal May-June 1991 For illustrative purposes only. Not indicative of any specific investment.

The Importance of Asset Allocation • Asset allocation is the MOST important decision an investor makes (i.e., buying some stock, NOT Coke versus Pepsi) • Asset allocation determines about 90% of the return variation between portfolios • This study has been repeated numerous times, by different researchers, with similar results.

Downside of Asset Allocation • A diversified portfolio MAY generate a lower rate of return when compared to a single “hot” asset class (e.g., growth stocks from 1995-99) BUT • You never know the “hot” asset class in advance (i.e., Callan table) • Asset allocation reduces volatility to provide a competitive rate of return

Factors To Consider • Investment objective (e.g., retirement) • Time horizon for a goal (e.g., life expectancy for retirement) • Amount of money you have to invest • Your risk tolerance and experience • Caution about risk tests • Your age and net worth

Stocks Large company growth & value Mid cap growth & value Small growth & value International Bonds Domestic International Corporate Municipal Real estate (e.g., REITs) Cash (CDs, I-bonds, MMMFs, Treasury bills) Major Asset Classes

Historical Average Annual Rates of Return • Small Co. U.S. stocks = 12.6% • Large Co. U.S. stocks = 10.4% • Government Bonds = 5.1% • Treasury Bills = 3.8% • Inflation = 3.1%

Stock Capitalization • Large Cap companies: valued at >$5 billion • ExxonMobil, General Electric, Microsoft • Mid-Cap: $1-5 billion • Bath & Beyond, Monsanto, Hilton Hotels • Small-Cap: <$1 billion • Earthlink, FirstFed Financial, Vintage Petroleum

Why Invest Internationally? • Correlations among world markets are low (e.g., U.S. and foreign stocks) • World markets (especially small companies) are driven by local dynamics • Investing in U.S. multinationals does not deliver the same level of diversification • The benefits of diversification outweigh currency, market, & political risks • U.S. accounts for less than 1/3 of the world’s equity (stock) markets

Other Things to Know About Asset Allocation • Portfolio risk decreases as the # of asset classes increases • Best results are achieved over time • Diversify holdings within each asset category • Stock: different industry sectors • Bonds: different types and maturities

RISK • Is a 4 letter word • Remember 2000-2003? • S&P 500 lost 40% of its value

Risk-Return Relationship • Low risk = low return • High risk = possibility of high return • Risk: chance of loss of principal in the short run • 2000-2003 most U.S. stocks lost value (after incredible run-up in prices in 1990s)

Relationship Between Risk and Return High Int’l Stocks U.S. Stocks Real Estate Expected Return Int’l Bonds U.S. Bonds Cash Equivalents Low Low Risk High For illustrative purposes only. Not indicative of any specific investment.

Diversification From Combining Investments No Diversification Complete Diversification Portfolio 1 Portfolio 2 Investment A Investment C Investment D Investment B Some Diversification Portfolio 3 Investment E Investment F For illustrative purposes only. Not indicative of any specific investment

Stocks are Risky in Short Run • Very volatile in sort run (1-5 years) • annual returns -50% to +50%!! • Remember 2000-2003? • 2003 was a great year to buy stocks when all news was gloom & doom • Large Co. U.S. stocks = 10.7% (avg. returns since 1926)

Time Horizon for Retirement? • Until the day you retire? • Until the day you die?

Invest for Growth • There is no such thing as a risk-free investment! • Retirement $ must grow faster than inflation to provide financial security • Average inflation = 3.1% • Risk is relative • Short term volatility=long term growth • Invest in stocks for growth

Recent Example • 2000-2003 was a gut check • Thank goodness some of my portfolio was in bonds & real estate! • Stocks tanked • Bonds held steady • Real estate saved the day

“Safe” Investments are Risky in the Long Run • Inflation = 3.1% • Government Bonds = 5.1% -3.1% = 2% • Treasury Bills = 3.8% - 3.1% = 0.7% • Subtract the impact of taxes and ‘safe’ investments yield negative returns • You will not reach your goal with low risk investments

Understand Risk Tolerance • Beware of taking risk tests and settling for a conservative portfolio • Conservative investors risk outliving their assets • Life expectancy calculators • http://www.ces.purdue.edu/retirement/Module1/module1b.html

The Asset Allocation Process • Define goals and time horizon • Assess your risk tolerance • Identify asset mix of current portfolio • Create target portfolio (asset model) • Select specific investments • Review and rebalance portfolio yearly

Tips For Funding a Tax-Deferred Employer Plan • Diversify across asset classes • Avoid market timing • Choose investments with good historical performance • Past returns are NO guarantee for the future!! • <10 year track record is too short! • Choose funds with low fees

The Big Picture • Same principles can be applied to • 401(k) plans • Individual retirement accounts (IRAs) • Other retirement plans

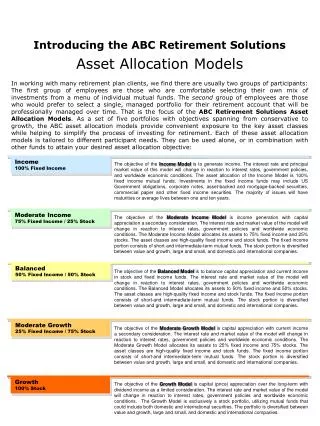

5 TIAA-CREF Asset Classes • Guaranteed (low risk; low return) • Fixed-Income (bonds) • Equities (stocks) • High return; volatile in the short run • Real Estate • Inflation protection; reduce volatility • Money Market (safe but very low return)

Global vs. International • Global: U.S. and foreign investments • International: “all” foreign

TIAA Traditional TIAA Real Estate CREF Money Market CREF Social Choice (bond & stock) CREF Stock Global Equities Growth Equity Index LOTS of overlap! TIAA-CREF Options (pre-2003)

Real Estate Securities Growth & Income S&P 500 Index Large Cap Value Social Choice Equity Mid-Cap Value Mid-Cap Growth Small-Cap Equity International Equity 9 New Fund Choices (2003)

Murky Mixture • Few of the CREF funds are “pure” • CREF Stock • 80% Large-, 15% Mid-, 5% Small-Cap • Some foreign stocks • Mid-Cap Growth • 59% Large-! 39% Mid-, 2% Small-Cap • Read Prospectus (or at least the summary)

Growth Portfolio: 3 asset classes • STOCKS for growth • Large-cap Domestic • 10-15% Mid-Cap • 10-15% Small-cap • 10-15% International • 10-15% Real Estate (to beat inflation) • 10-15% Bonds (to dampen volatility)

New Funds Offer Diversity • Lots of different stock accounts DO NOT mean diversification (overlapping) • International Equity • Small-cap Equity • Real Estate Securities (to complement TIAA Real Estate)

Your “Action” List • Review your current asset allocation • Consider your other retirement accounts • Use the TIAA-CREF web site • Understand risk-return relationship • Talk with a TIAA-CREF rep (at USU) • Sign up for automatic rebalancing • Limits on moving $ out of TIAA • Re-visit, Reallocate, Rebalance

Key Considerations For Successful Investing • Educate yourself to make informed decisions • Establish policies and objectives • Monitor investment performance • Stick to your plan and stay focused • If you need help, seek professional advice

Financial Planning for Women • Second Wednesday of the month • 12:30-1:30 in Family Life 318 • bring your lunch • 7-8:30 p.m. at Family Life Center (500 N & 700 E – bottom of Old Main Hill) • February 8 FPW: Investment Basics • For mo. email news & reminder: Sign up sheet or send email to Lown@cc.usu.edu

Questions? Comments? Experiences? February 8 FPW: Investment Basics Baby Boomer Women Retirement Study USU IRB approved research Step 1: Survey- return by Feb 3 for prize drawing Step 2: Focus Group ($25 compensation)