Capital-Based Macroeconomics

Capital-Based Macroeconomics. Adapted from Time and Money: The Macroeconomics of Capital Structure by Roger W. Garrison London: Routledge, 2001. Keynes and Hayek: Head to Head. 2009. Keynes and Hayek: Head to Head. Friedrich A. Hayek 1899 — 1992. John Maynard Keynes 1883 — 1946.

Capital-Based Macroeconomics

E N D

Presentation Transcript

Capital-Based Macroeconomics Adapted from Time and Money: The Macroeconomics of Capital Structure by Roger W. Garrison London: Routledge, 2001 Keynes and Hayek: Head to Head 2009

Keynes and Hayek: Head to Head Friedrich A. Hayek 1899 — 1992 John Maynard Keynes 1883 — 1946

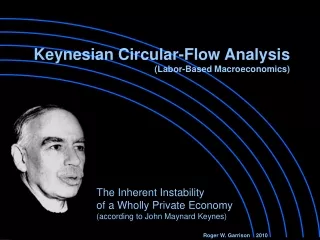

Visions and Frameworks Keynes’s vision of the economy suggests a circular-flow framework—in which earning and spending are brought into balance by changes in the level of employment. Hayek’s vision of the economy suggests a means-ends framework—in which the means of production are transformed over time into consumable output. Graphically, the circular flow appears as the Keynesian cross, the cross’s intersection identifying the particular state of the economy in which income and expenditures are in balance. Graphically, the means and ends appear as the Hayekian triangle, the triangle’s shape depicting the intertemporal pattern of investment. In equilibrium, the pattern of investment corresponds to the intertemporal preferences of consumers.

A BRIEF REVIEW of the KEYNESIAN CIRCULAR-FLOW FRAMEWORK SKIP

BUSINESS ORGANIZATIONS LABOR AND OTHER FACTOR SERVICES THE CIRCULAR-FLOW FRAMEWORK WORKERS CONSUMERS INVESTORS INCOME

BUSINESS ORGANIZATIONS EXPENDITURES consumption plus Investment LABOR AND OTHER FACTOR SERVICES GOODS AND SERVICES WORKERS CONSUMERS INVESTORS INCOME

BUSINESS ORGANIZATIONS EXPENDITURES consumption plus Investment Federal Reserve Policy SLOW 6 % FAST 2 % I N T E R E S T R A T E C O N T R O L WORKERS CONSUMERS INVESTORS INCOME

BUSINESS ORGANIZATIONS EXPENDITURES consumption plus Investment CONSUMPTION STAGES OF PRODUCTION WORKERS CONSUMERS INVESTORS INCOME

BUSINESS ORGANIZATIONS EXPENDITURES consumption plus Investment CONSUMPTION STAGES OF PRODUCTION WORKERS CONSUMERS INVESTORS INCOME SKIP

BUSINESS ORGANIZATIONS EXPENDITURES consumption plus Investment In Keynesian equilibrium, INCOME equals EXPENDITURES. Y = E For a wholly private economy: Y = C + I WORKERS CONSUMERS INVESTORS INCOME

C + I EXPENDITURES The economy is in a Keynesian equilibrium somewhere along the 45o line—the line itself identifying all possible income-expenditure equilibrium points. As taught at all levels, the consumption function is an essential component of the Keynesian framework. The presumed stability of this function underlies Keynesian thinking. Investment depends neither on (current) income nor on the rate of interest. It depends only on profit expectations, which themselves are not well-anchored in economic reality. INVESTMENT C = a + bY b 1 CONSUMPTION a 45o INCOME INCOME Consumption and Investment (as well as Government Spending) are portrayed as additive components of total spending. The three components are distinguished largely in terms of their stability characteristics: stable (C ), unstable (I), and stabilizing (G). A wholly private macroeconomy achieves an income-expenditure equilibrium when Y = C + I. Note that income itself (rather than prices, wages, or the interest rate) is the equilibrating variable.

C + I EXPENDITURES C = a + bY CONSUMPTION According to Keynes, it is only by “accident or design” that the economy is actually performing at its full-employment potential. We assume here that, initially, full employment conditions prevail—if only by accident. INCOME INVESTMENT Yfe Labor income (Y = WN) is fully representative of total income, such that changes in labor income stand in direct proportion to changes in total income. In capital-based macroeconomics, full employment implies that the economy is operating on its production possibility frontier, the PPF itself being defined in terms of sustainable output levels of consumption and investment goods. In Keynesian macroeconomics, full employment implies that the labor market clears at the going wage rate, the going wage itself having emerged during a period in which the economy was experiencing no macroeconomic problems. W S LABOR INCOME D N

C + I ΔI EXPENDITURES EXCESS INVENTORIES C = a + bY 1 (1 – b) ΔY = ΔI E = Y E < Y ΔC ΔY INCOME Yfe According to Keynes, a collapse of investment activity (the collapse being attributed to a waning of “animal spirits”) is the primary cause economic downturns. In response to reduced investment and hence reduced employment opportunities, the economy spirals downward into recession and possibly into deep depression. SKIP W Note that the going wage keeps going—even after the market conditions that gave rise to it are gone. S D The simple investment-spending multiplier, 1/(1-b), quantifies the extend of the downward spiraling. N

EXPENDITURES C + I C = a + bY INCOME Yfe A further loss of confidence on the part of the business community will send the economy even further from its full-employment potential. In the Keynesian construction, prices and the wage rate are sticky downward. But note that they’re not stuck too high. They’re stuck just right. The going wage rate will clear the labor market once again—as soon as spending and hence labor demand recover to their full-employment levels. W S D N

EXPENDITURES C + I C = a + bY INCOME Yfe Recovery may be self-initiating. Waning animal spirits may become waxing animal spirits. In due time, a pressing need to maintain or replace depreciating capital may account for the lower turning point of a bust-and-recovery sequence. (Keynes, of course, preferred not to wait it out. He advocated make-work projects, deficit spending, and monetary stimulation to get the economy turned around.) W S D N

EXPENDITURES C + I C = a + bY INCOME Yfe Recovery may continue as further investment activity drives labor-demand back to its full-employment level... W S D N

C + I EXPENDITURES C = a + bY INCOME From full-employment onward, there is upward pressure on both prices and wage rates. And since prices and wage rates are not sticky upwards, the economy experiences a spiraling inflation. Yfe Recovery may continue as further investment activity drives labor-demand back to its full-employment level... The equilibrium points in the labor market traced out during the recovery and inflationary spiral constitute the so-called L-shaped supply curve. but there is nothing about “animal spirits” that will bring the recovery process to an end at full employment. Over-optimism may push the economy beyond its full-employment level. W S D N

MORPHING FROM CIRCULAR FLOW TO MEANS AND ENDS

C + I EXPENDITURES C = a + bY CONSUMPTION INCOME INVESTMENT Yfe The nature of the Keynesian-styled spiraling associated with recession, depression and inflation becomes more transparent with the production possibility frontier in play. Also, the PPF helps build a bridge from Keynes to Hayek. W S D N

C + I EXPENDITURES C = a + bY CONSUMPTION INCOME INVESTMENT Yfe A waning of animal spirits causes investment to decrease and with it income and consumption. The economy falls inside its PPF. W S D N

EXPENDITURES C + I C = a + bY CONSUMPTION INVESTMENT INCOME INVESTMENT Yfe Note that if investment were to fall to zero, the economy would settle into an income-expenditure equilibrium with Y = C. Thus, the vertical intercept of the Keynesian demand constraint is aligned with the intersection of the consumption function and the 45o line. A further waning sends the economy deeper into the PPF’s interior. Movements inside the frontier (and beyond it) trace out a linear relationship, showing how consumption varies with investment. W S D The straight line that passes through these points is the Keynesian demand constraint. N

C + I EXPENDITURES b (1 – b) a (1 – b) C = + I C = a + bY CONSUMPTION b 1 – b a (1 – b) INCOME INVESTMENT Yfe For simplicity, let a = 0 and b = 0.90. Then C = a + bY becomes C = 0.90Y. And C = a/(1-b) + b/(1-b) I becomes C = 9(I), which led Keynes to write: “If, for example, the public are in the habit of spending nine-tenths of their income on consumption goods, it follows that if entrepreneurs were to produce consumption goods at a cost more than nine times the cost of the investment goods they are producing, some part of their output could not be sold at a price which covered its cost of production.” “The formula is not, of course, quite so simple as in this illustration…. But there is always a formula, more or less of this kind, relating the output of consumption goods which it pays to produce to the output of investment goods…. This conclusion appears to me to be quite beyond dispute. Yet the consequences which follow from it are at the same time unfamiliar and of the greatest possible importance.”

C + I EXPENDITURES C = a + bY CONSUMPTION INCOME INVESTMENT Yfe To keep track of possible interest-rate movements, the loanable-funds market can be brought into view. S RATE OF INTEREST Though Keynes argued that neither saving nor investment depend to any significant extent on the interest rate, he also argued that both curves (as conventionally drawn) shift together, leaving the interest rate unchanged. D SAVIING (S) INVESTMENT (D)

C + I EXPENDITURES C = a + bY CONSUMPTION INCOME INVESTMENT INVESTMENT Yfe With the loanable-funds market in play, we see that decreased investment is accompanied by a leftward shift in the demand for loanable funds, putting downward pressure on the interest rate. S RATE OF INTEREST Appearing in Keynes’s General Theory is this specific application of the loanable-funds framework. The implications, according to Keynes, is that the loanable-funds reckoning is, at best, superfluous. W S But the spiraling downward of income implies that the supply of loanable funds (a.k.a. saving) also shifts leftward, relieving the downward pressure on the interest rate. D D N SAVIING (S) INVESTMENT (D)

As shown on page 180 of his General Theory, Keynes presented the loanable funds market with the interest rate [ r ] on the horizontal axis. Although he failed to label the vertical axis, the accompanying text indicates that “saving” and “investment” are measured vertically. i Keynes’s diagram can be flipped over and rotated 90 degrees to make it conform to modern renditions of the market for loanable funds. S, I S, I Some of the saving curves are intended only to demonstrate that income is a shift parameter and are not otherwise relevant to Keynes’s argument. So, let’s omit them

i ieq S’ = I’ S = I S, I Keynes believed that a shift in investment demand would be accompanied by a matching shift in the saving schedule. Some of the saving curves are intended to demonstrate that income is a shift parameter and are not otherwise relevant to Keynes’s argument. So, let’s omit them.

EXPENDITURES C + I C CONSUMPTION INCOME INVESTMENT INVESTMENT Yfe S RATE OF INTEREST Appearing in Keynes’s General Theory is this specific application of the loanable-funds framework. The implications, according to Keynes, is that the loanable-funds reckoning is, at best, superfluous. D SAVIING (S) INVESTMENT (D)

C + I EXPENDITURES C CONSUMPTION INCOME INVESTMENT INVESTMENT Yfe Hence the Paradox: Try to save more and you’ll instead earn less! The rightward shift in supply of loanable funds puts downward pressure on the interest rate. But before there is any movement along the demand for loanable funds, the pressure is relieved as reduced consumption causes income and hence saving to fall. Keynes also denied that an increase in saving would have the effect imagined by the loanable-funds theorists. Keynes’s “Paradox of Thrift,” as articulated in his General Theory is to the point: “Every ... attempt to save more by reducing consumption will so affect incomes that the attempt necessarily defeats itself.” To resolve Keynes’s “Paradox of Thrift” requires only that we replace the Keynesian cross, which reflects the economy’s circular flow, with the Hayekian triangle, which depicts means and ends in their temporal sequence. S RATE OF INTEREST S W S D D N SAVIING (S) INVESTMENT (D)

C + I EXPENDITURES C CONSUMPTION CONSUMPTION INCOME INVESTMENT Yfe The level of consumption that appears as a part of the Keynesian circular flow also appears in the capital-based framework as the consumable output of a temporal sequence of production activities. S RATE OF INTEREST D SAVIING (S) INVESTMENT (D)

CONSUMPTION CONSUMPTION CONSUMPTION STAGES OF PRODUCTION INVESTMENT INVESTMENT Note that the sole effect on the structure of production comes from the initial reduction in consumption. The derived-demand effect works undiminished on all the earlier stages. The interest rate is effectively out of play. The leftward shift of saving took the downward pressure off of interest rates. And, in any case, the capital structure is assumed to be fixed. The market mechanisms in play here are still those envisioned by Keynes. In accordance with the paradox, an increase in saving causes the economy to spiral down to a less-than-full-employment level. Keynes, however, assumed a “fixed structure of industry,” which in the current context implies a a Hayekian triangle of fixed shape, the only live issue being the triangle’s size, which represents the level of employment and the extent of capital utilization. We begin, as before, with the economy functioning at its full employment level. The labor market is representative of each of the stages of production that make up the economy’s capital structure. The level of consumption that appears as a part of the Keynesian circular flow also appears in the capital-based framework as the consumable output of a temporal sequence of production activities. S RATE OF INTEREST S W W S S D D D N N SAVIING (S) INVESTMENT (D)

Three modifications are needed to transform the Keynesian vision into the Hayekian vision: And now, the “Paradox of Thrift” becomes a “Gateway to Growth.” With wage rates and the interest rate both adjusting to changing market conditions, the economy can move along its PPF and the structure of production can adjust to an increase in saving. 1. Divide the structure of production into stages. 3. Get rid of the Keynesian Demand Constraint. 2. Allow for stage-specific labor markets---in which wage rates adjust to changed market conditions. CONSUMPTION CONSUMPTION STAGES OF PRODUCTION STAGES OF PRODUCTION STAGES OF PRODUCTION INVESTMENT INVESTMENT RATE OF INTEREST S W W W S S S D D D D D N N N SAVIING (S) INVESTMENT (D)

BUSINESS ORGANIZATIONS EXPENDITURES “Mr. Keynes’s aggregates conceal the most fundamental mechanisms of change.” CONSUMPTION STAGES OF PRODUCTION WORKERS FACTOR OWNERS CONSUMERS INCOME

Keynes and Hayek: Head to Head Friedrich A. Hayek 1899 — 1992 John Maynard Keynes 1883 — 1946

Capital-Based Macroeconomics Adapted from Time and Money: The Macroeconomics of Capital Structure by Roger W. Garrison London: Routledge, 2001 Sustainable and Unsustainable Growth The Macroeconomics of Boom and Bust 2009

Capital-Based Macroeconomics Adapted from Time and Money: The Macroeconomics of Capital Structure by Roger W. Garrison London: Routledge, 2001 Keynes and Hayek: Head to Head 2006