Download

1 / 48

480 likes | 946 Views

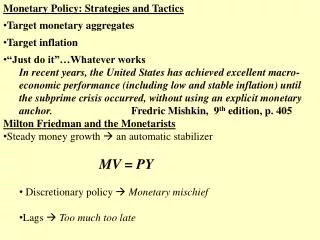

Monetary transmission mechanism and inflation modeling in Poland. Ryszard Kokoszczy ń ski Bureau of Macroeconomic Research National Bank of Poland. Monetary policy framework and the shape of macroeconomic analysis.

E N D

Monetary transmission mechanism and inflation modeling in Poland Ryszard Kokoszczyński Bureau of Macroeconomic Research National Bank of Poland

Monetary policy framework and the shape of macroeconomic analysis • Monetary targeting –relies on the assumed stable relationship between money and inflation. Macroeconomic analysis: money demand functions, short-term forecasting,simple statistical tools. • Inflation targeting – crucial role of medium-term inflation forecasting. Model-based forecasts. Monetary transmission analysis (S-VARs, structural econometric models, DSGE models).

Selected factors affecting MTM • Monetary policy framework – in Poland IT • The role of banks: In Poland banks are the most important financial intermediaries, but the share of internal financing of investment is relatively high • Degree of banking sector concentration: in Polandlow to medium • Other country-specific factors: for Poland and other NMS - the EU entry

Monetary policy framework • Inflation targeting since 1998; • Since 2000 official pure float.

MTM – interest rate channel • The role of banks in MTM • Results from structural VARs • Results from a small structural model • Credit channel – does it exist in Poland?

Financial intermediation • Relatively low (but growing) level of financial intermediation

Financial system • Bank loans dominate as a source of external financing investment; • Important role of loans in foreign currencies • Surplus liquidity of the banking sector since mid-1990s.

Banking sector concentration in Poland (Herfindahl-Hirschman index)

Interest rate p-t and concentration degree Simple (perhaps too simple) exercise: monthly Herfindahl-Hirschman indices added to the previously estimated pass-through equations The degree of concentration mattered for both deposit and lending rate adjustment (the estimated coefficients were significant). For deposits the estimated coefficients were positive, while for credits – negative.

Factors affecting effectiveness of interest rate impact on credit demand • Still underdeveloped financial markets • Mismatch between term structure of banks’ assets and liabilities • Easy access to credits nominated in foreign currencies

Interest rate channel – results from S-VAR (CEE-type, montly data)

Interest rate channel – results from S-VAR (CEE-type, monthly data)

Credit channel • Conflicting evidence on credit channel in Poland • Previous studies pointed at bank size and capital as well as variables connected with bank risk taking as these affecting credit supply. The latest panel study points at the degree of liquidity.

Credit channel – assumptions in the estimation • A bank increases loan supply with an increase in loan rate and decreases with policy rate increases; • Demand for credit increases with output; • Demand for loans and loan supply react to interest rate shocks with a delay (but quarterly frequency of data makes some problems); • Monetary policy tightening limits the possibility of financing investment expenditures from own sources. A firm wanting to invest has to resort to external financing and its balance sheet can affect bank’s willingness to grant a credit. • Due to reserves drainage, banks are less willing to grant credits. The same effect can result from an adverse shock to banks’ capital.

Alternative ordering: credit adjusts within a quarter of monetary policy shock

Credit channel, disaggregated monthly data sample 2002 onwards (very short!) • Units analysed differ by size and ownership: Private firms (named – with some exaggeration – „big”) - more than 9 pers. employed Individual firms (called „small”) – up to 9 pers. employed, private ownership (micro firms) State-owned firms (mining, electricity, gas and power, railway transport etc). • Bank products: credit in current account, revolving credit, investment credit, export credit

Credit channel: what do we expect • A difference in behaviour between big and small firms; • Demand side: bigfirms should be less dependent on the domestic bank financing→a low interest rate semi-elasticity of loan demand. Demand for credit correlated with real activity of firms but the sign of reaction depends on firms’ assessment of the future state of the economy. The level of income elasticity of loan demand can be a measure of uncertainty. A positive but low can indicate that a moderate rate of future returns combined with high uncertainty is expected. Big firms less worried about their economic condition - elasticity can be somewhat higher than for other groups of firms. • Supply side, if banks assess large firms as credible (or can easier monitor them) - loan rate and short-term rate semi-elasticity of loan supply relatively low.

Credit channel: what do we expect (cont) • A difference in behaviour between big and small firms; • Demand side:smaller firms after monetarytightening will rather postpone investment than increase their demand for investment loans. They may rely heavily on short-term loans to finance working capital and inventories. Interest rate semi-elasticity of investment loan demand should be relatively low and respective elasticity of revolving credits and credits in current account should be higher. They rely more on external sources of financing. Demand for short-term loans for current activity is positively correlated with their real income. It can result in relatively high income elasticity of loan demand, particularly for short-term credits. • Supply side: Banks will not respond to such demand positively, adjusting loan supply rather moderately (risk, not enough information).

Credit channel: what do we expect (cont) • A difference between private and state-owned firms: - poor finacial standing (net real loss), lack of capital for investment, risk aversion, frequently changing privatisation plans of goverments, but at the same time possible perception as units having implicit privilages → low elasticities and semi-elasticities of both loan supply and loan demand

Credit channel – what results do we get? • It has been confirmed that there is a difference in reaction to monetary policy shocks between big and small firms (demand side). The reaction of big firms is small and similar for all types of loans. Small firms tend to resign from investment after interest rate increase. Demand for investment loans is inelastic in state-owned enterprises. • Supply side: Differences in the adjustment of loan supply, leading to the observed weakness of the operation of credit channel on the macro level. Adjustments apply rather to types of loans than to groups of enterprises.

Buffer stock behaviour of banks • A crucial assumption in the bank lending channel theory is that monetary contraction drains banks’ reserves, which forces those banks, which are not able to offset a decline in reserves, to adjust their assets, including loans. • Empirical studies suggest that credit contraction may be significantly weakened by changes in the portfolios of the most liquid assets such as Treasury securities. In contradiction to loans, Treasuries can be easily liquidated, so they can serve as a buffer-stock.

Concluding remarks • Tradtional interest rate channel seems to be more important than the credit channel. • Interest rate channel seems to operate faster comparing to our previous estimates (2002). • Credit channel operates, but it is easier to point at some types of credit that work as theory predicts than types of firms (may be the problem of statistical definition of small and big firms). • A big portfolio of liquid assets seems to weaken credit channel operation.

Bureau of Macroeconomic Research MTM – exchange rate channel:Pass-through effect in Poland

Flowchart of the pass-through effect. Interest rate disparity Term structure of interest rates Risk factors (i.e. BD, CA) oil price (Brent, in USD) (supply shock) NEER (30% USD; 70% EUR) (demand shock) output gap (demand shock) CPI Import prices (in domestic currency) Net exports PPI

McCarthy’s model (1999) where: m - index of the import transaction prices expressed in the domestic currency; w - price index of the sold production of industry (PPI); c - consumption price index (CPI); Et-1 - expected value of the corresponding variable in the period t-1. s - supply shock, identified with the oil price (πoil): d - demand shock, identified with the output gap (φ): e - exchange rate shock, identified with the changes of the nominal effective exchange rate:

Bureau of Macroeconomic Research Pass-through effect for the import prices • Camp and Goldberg (2002) obtained similiar results for the OECD countries.

Bureau of Macroeconomic Research Pass-through effect for import prices. • Time decomposition of the P-T effect (for Poland): • t0: 17%; t1: 49%; t2: 25%; t3: 4%; t4÷t8: 5% • Time decomposition of the P-T effect: for OECD 77% in two quarters, for Germany 75% (Camp i Goldberg); for euro-zone 71% (Anderton) or 100% in three quarters (Hahn). • Ratio of the supply to the exchange rate shocks: • Poland: 25% and 75%; OECD: 33% and 67%; • Euro-zone: 41% and 59%.

Pass-through effect for the producer prices • Pass-through close to the share of imports of intermediate goods in total imports.

Bureau of Macroeconomic Research Pass-through effect for PPI. • Time decomposition of the P-T effect (for Poland):51% in two quarters and 88% in one year. • Ratio of the supply to the exchange rate shocks:Poland: 20% i 80%; • For the OECD pass-through effect < 0,3 and diversified among countries; the greater role of the supply shock than the exchange rate shock (McCarthy, Hahn).

Pass-through effect for the consumer prices •Exchange rate pass-through higher than in the most of the developed countries.

Pass-through effect for CPI. • Time decomposition of the P-T effect (for Poland): • t0: 11%; t1: 43%; t2: 30%; t3: 7%; t4÷t8: 9%. • Pass-through in the other countries: • - insignificantly differs from zero in the most OECD • countries, except Belgium and the Netherlands • (McCarthy 2001); • - in 5 Euro countries: 0,04 in one quarter and • 0,08 after 12 q. (Huefner i Schroeder 2002); • - in euro-zone: 0,025 in 1 q.; 0,08 after 4 q.; • 0,16 after 12 q. (Hahn 2003)

Medium-term forecasts, MTM and policy analysis: structural models • A small highly aggregated model (NSA) • A medium-size structural model (ECMOD), the main forecasting tool. • A DSGE model (know-how: Riksbank, estimated on the Polish data).