Download

1 / 3

0 likes | 2 Views

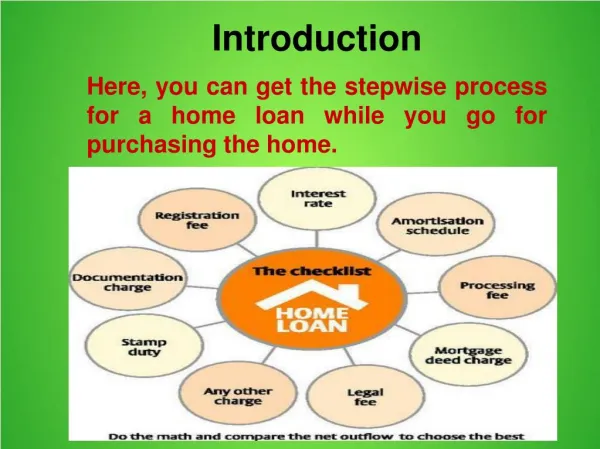

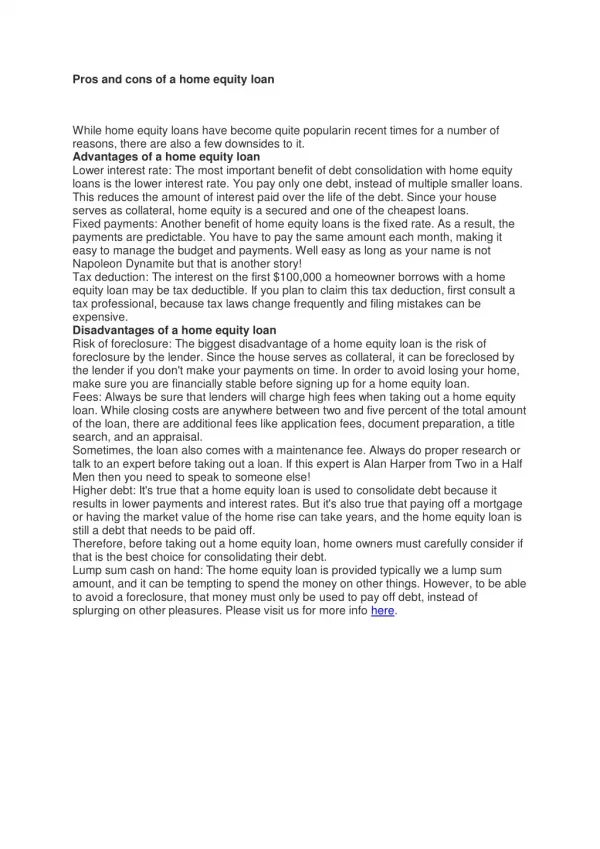

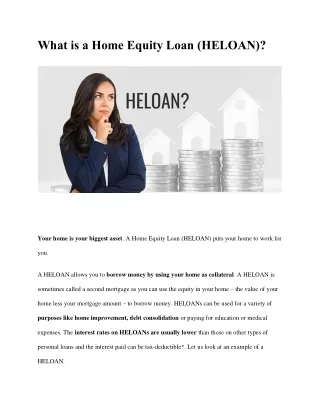

Finding the "best" home equity loan isn't a one-size-fits-all answer, as the optimal choice largely depends on an individual's financial situation and goals. These loans provide a lump sum of cash, secured by your home's equity, typically with a fixed interest rate and repayment schedule.

E N D