Download

1 / 4

0 likes | 3 Views

Learn how a HELOC can help you access your home's value with flexibility and low interest. No fees. No credit hit. Fast closing times.<br>

E N D

Home Equity Line of Credit (HELOC): A Flexible Financing Tool for Homeowners in 2025 Introduction As home values continue to climb in 2025, many homeowners are seeking smart ways to leverage their equity. One of the most popular and flexible solutions is a home equity line of credit (HELOC). Whether you’re planning a home renovation, covering education expenses, or consolidating high-interest debt, a HELOC offers a convenient and often low-cost way to borrow against the value of your home. This article explains what a home equity line of credit HELOC is, how it works, its pros and cons, and how to choose the best one for your financial goals. What Is a Home Equity Line of Credit (HELOC)? A home equity line of credit HELOC is a revolving line of credit that lets you borrow against the equity in your home. Equity is the difference between your home’s current market value and what you owe on your mortgage. Unlike a traditional home equity loan, which gives you a lump sum upfront, a HELOC functions like a credit card. You can borrow, repay, and borrow again up to a set limit during a defined draw period, typically lasting 10 years. After the draw period, you enter the repayment phase, which can last another 10 to 20 years. How a HELOC Works 1. Draw Period During this phase, you can access funds as needed, up to your approved credit limit. Most lenders offer checks, debit cards, or online transfers to make access easy. 2. Variable Interest Rates Most HELOCs have variable interest rates tied to the prime rate, which means your monthly payment may fluctuate. Some lenders offer fixed-rate conversion options for part of your balance. 3. Repayment Period

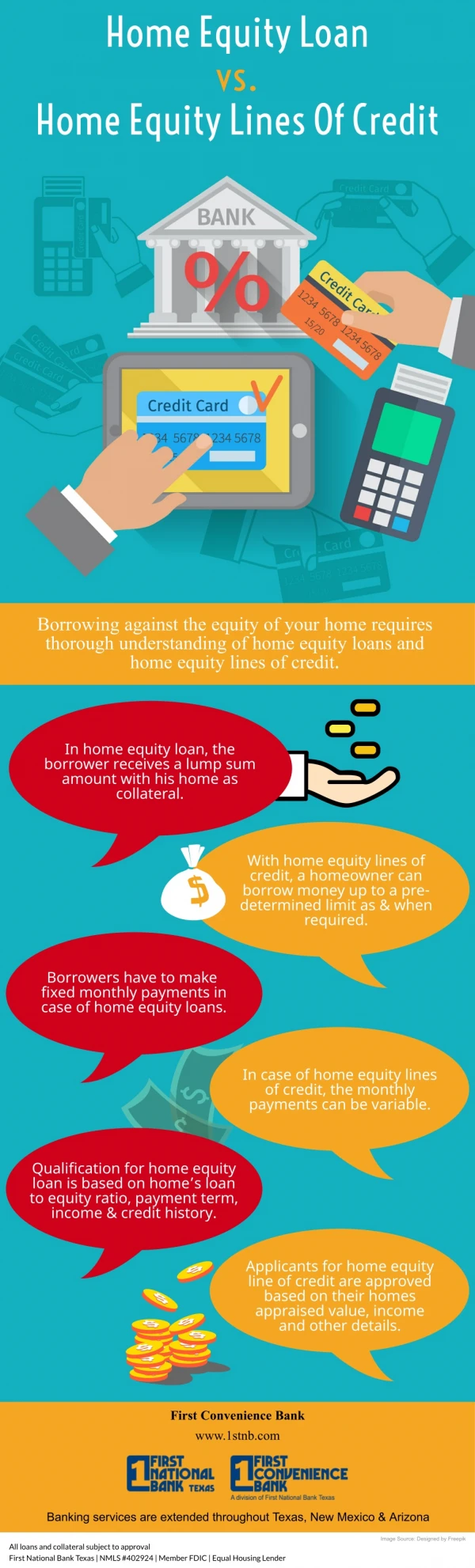

Once the draw period ends, you can no longer borrow additional funds. You must begin repaying the outstanding balance—often in fixed monthly payments including principal and interest. Benefits of a Home Equity Line of Credit HELOC ✅ Flexibility HELOCs provide ongoing access to funds, making them perfect for long-term or unpredictable expenses, such as home improvements or medical bills. ✅ Lower Interest Rates Because your home secures the loan, interest rates are generally lower than those for credit cards or personal loans. ✅ Interest-Only Payments During Draw Period During the draw phase, you’re often only required to pay the interest, reducing your monthly payment obligations. ✅ Pay for What You Use You’re not obligated to use the full amount available. Interest is only charged on the portion you borrow. Risks and Considerations While a home equity line of credit HELOC can be beneficial, it’s not without risks: ❌ Variable Interest Rates If interest rates rise, your monthly payments may increase significantly. ❌ Potential for Over-Borrowing The ease of access to funds can tempt some borrowers to overspend. ❌ Risk of Foreclosure Because your home is collateral, failure to repay could result in losing your home. ❌ Fees and Closing Costs Some lenders charge annual fees, inactivity fees, or closing costs, which can add to the cost of borrowing.

How to Qualify for a HELOC Lenders typically consider the following factors when evaluating your HELOC application: ● Home Equity: You’ll need at least 15%–20% equity in your home. ● Credit Score: A score of 620+ is required, but 700+ will get you better rates. ● Debt-to-Income Ratio (DTI): Most lenders look for a DTI below 43%. ● Income and Employment: You must demonstrate reliable income and employment history. To improve your chances, pay down existing debt and review your credit report before applying. Top HELOC Lenders in 2025 Choosing the right home equity line of credit HELOC depends on your goals, location, and credit profile. Here are some top-rated options: 1. Bank of America ● APR: Starting at 8.00% ● Highlights: Introductory rate discounts, fixed-rate conversion options 2. Wells Fargo ● APR: Starting at 7.75% ● Highlights: High borrowing limits, online account management 3. Figure ● APR: Starting at 7.99% ● Highlights: Fast approval and funding, all-digital application 4. PenFed Credit Union ● APR: Starting at 6.99%

● Highlights: Low fees, excellent customer service HELOC vs. Home Equity Loan: What’s the Difference? Feature HELOC Home Equity Loan Disbursement As needed, revolving credit Lump sum Interest Rate Usually variable Usually fixed Repayment Terms Draw and repayment periods Fixed term with regular payments Best For Ongoing or variable expenses One-time, large expenses If you prefer flexibility and ongoing access to funds, a home equity line of credit HELOC may be better than a fixed home equity loan. Tips for Managing Your HELOC 1. Borrow Wisely: Use the funds for value-adding investments like renovations or debt consolidation. 2. Track Interest Rate Changes: Since rates are variable, monitor the market to prepare for payment changes. 3. Make Extra Payments: Paying more than the minimum reduces your principal and long-term interest. 4. Review Your Terms: Understand your draw period, repayment schedule, and any applicable fees. Final Thoughts A home equity line of credit HELOC offers homeowners flexible access to funds with competitive rates and significant borrowing power. If used responsibly, it can be an effective way to finance home upgrades, pay off high-interest debt, or cover other large expenses. However, it’s important to understand the terms, compare lenders, and ensure that you can comfortably manage your repayments—especially when the draw period ends. By tapping into the equity you’ve built in your home, a HELOC can serve as a powerful financial tool to help you reach your short- and long-term goals in 2025.