Download

1 / 2

0 likes | 5 Views

A Home Equity Line of Credit (HELOC) can serve as a strategic tool when considering a HELOC for down payment on new home. This financial instrument allows homeowners to tap into the equity built up in their current residence, providing a flexible line of credit that can be drawn upon to secure the necessary funds for a down payment on a new property.

E N D

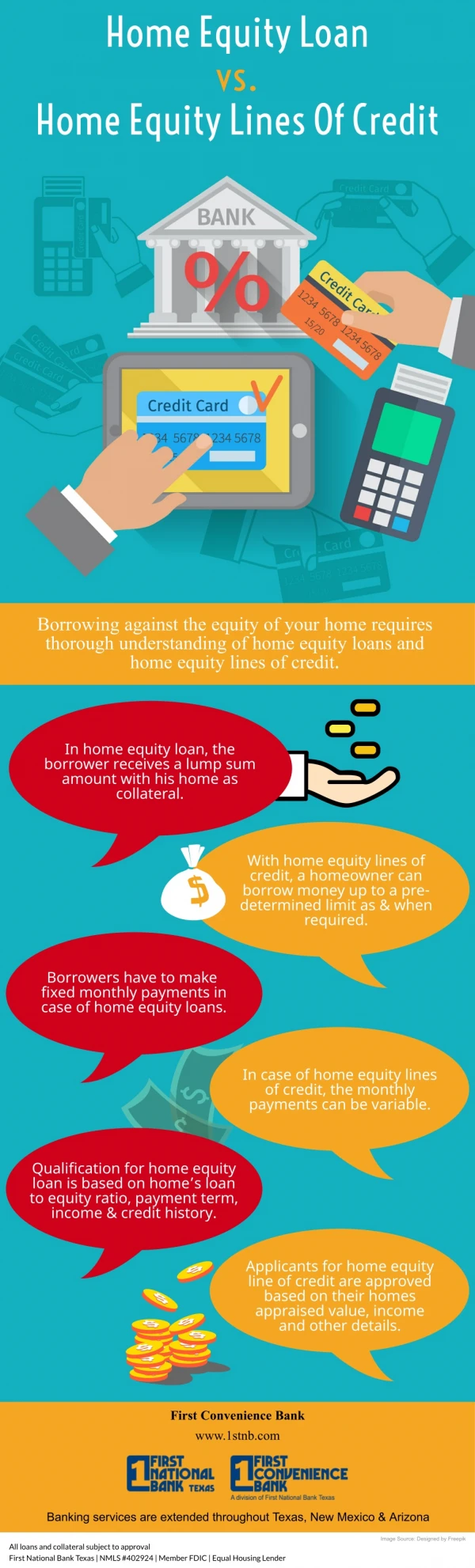

Unlocking Your Home's Potential: How Much Can You Borrow with a HELOC? A Home Equity Line of Credit (HELOC) is a versatile financial tool that allows homeowners to tap into the equity built up in their property. Unlike a lump-sum home equity loan, a HELOC provides a revolving line of credit, much like a credit card, allowing you to borrow, repay, and re-borrow funds up to a set limit over a specific draw period. It's popular for funding home renovations, consolidating high-interest debt, or covering unexpected expenses. But the burning question for many is: exactly "how much can you borrow?" Determining Your Borrowing Power The amount you can access through a HELOC isn't fixed; it depends on several key factors, primarily revolving around your home's available equity. 1. Your Available Equity: This is the cornerstone of your borrowing power. It's calculated by subtracting your outstanding mortgage balance from your home's current market value. For instance, if your home is worth $400,000 and you owe $200,000, you have $200,000 in equity. Lenders, however, typically won't let you borrow 100% of this. 2. Loan-to-Value (LTV) Ratio: Lenders use an LTV ratio to determine their risk exposure. Most will allow you to borrow up to 80% or 85% of your home's value, including your existing mortgage and the new HELOC. So, if your home is worth $400,000, and the lender's LTV limit is 85%, the maximum total debt secured by your home would be $340,000. If you still owe $200,000 on your mortgage, your maximum HELOC could be up to $140,000 ($340,000 - $200,000). This limit often directly dictates your maximum borrowing power. 3. Creditworthiness: Your personal financial health plays a crucial role. A strong credit score demonstrates your reliability in managing debt, often leading to better terms and a higher borrowing limit. Lenders also scrutinize your debt-to-income (DTI) ratio, ensuring you can comfortably handle the additional monthly payments without being overleveraged. 4. Property Value and Appraisal: To accurately determine your home's market value, lenders will typically require an appraisal. This professional assessment of your property value is critical in calculating your available equity and, consequently, your potential HELOC limit. Beyond the Numbers: Other Considerations While the above factors set your maximum limit, consider the practical implications. Interest rates for HELOCs are often variable interest rates, meaning your payments can fluctuate over time. Understanding the draw period (when you can access funds)

and the subsequent repayment period (when you pay back principal and interest) is vital for long-term planning. Responsible Borrowing Ultimately, the question isn't just how much you can borrow, but how much you should borrow to meet your financial goals without overextending yourself. Responsible borrowing means carefully assessing your needs, your ability to repay, and the potential impact of fluctuating interest rates. Conclusion The amount you can borrow with a Home Equity Line of Credit is a dynamic figure shaped by your available equity, the lender's LTV ratio, your credit score, and your debt-to-income ratio, all underpinned by an accurate property value appraisal. By understanding these elements, you can better estimate your potential borrowing power and make informed decisions about leveraging your home's equity. Always consult with a financial advisor or lender to get precise figures tailored to your unique situation.