Download

1 / 3

0 likes | 2 Views

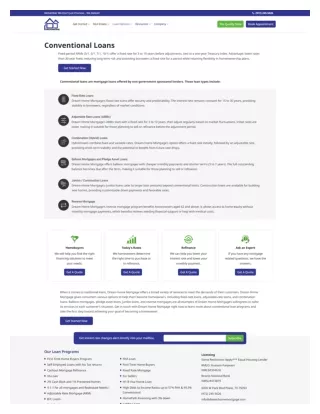

For homebuyers across Virginia, the conventional loan remains a widely sought-after financing option, distinguished by not being insured or guaranteed by a government agency. These loans often appeal to borrowers with strong credit scores and a solid down payment, offering competitive interest rates and flexible terms that can be tailored to various financial situations.

E N D