Download

1 / 3

0 likes | 2 Views

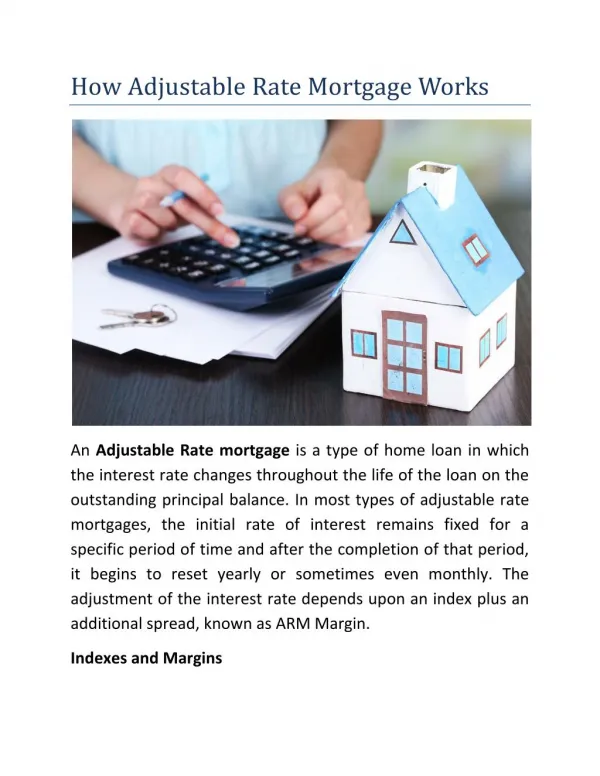

An Adjustable-Rate Mortgage is, simply put, a home loan where the interest rate can change over time. Unlike a fixed-rate mortgage, where your interest rate and monthly principal and interest payment remain constant for the life of the loan, an ARM typically starts with an initial fixed-rate period.

E N D