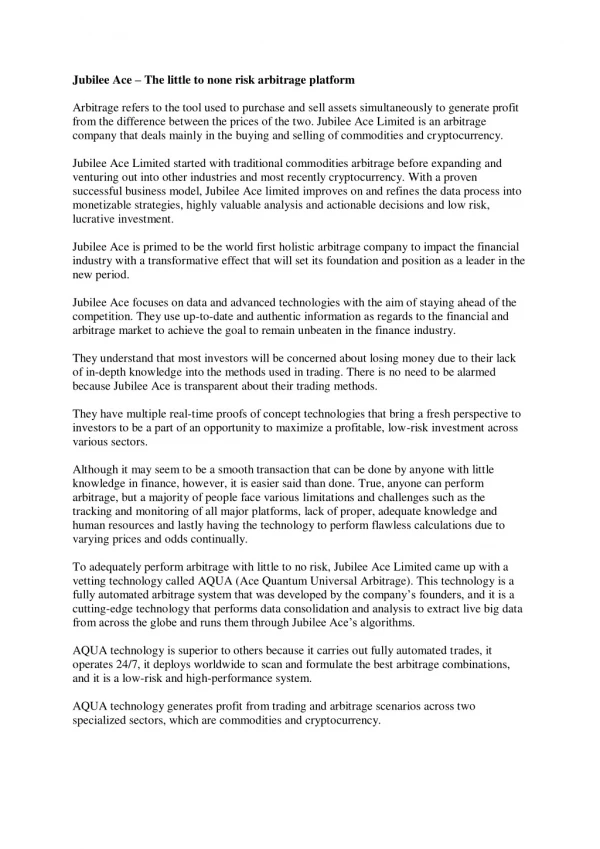

CompatibL Risk Platform

60 likes | 84 Views

An award-winning software solution for market and credit risk, regulatory capital, limits and initial margin.

CompatibL Risk Platform

E N D

Presentation Transcript

CompatibL Risk Platform About CompatibL CompatibL Technologies was founded in 2003 to offer risk technology solutions to banks and asset managers. Since then CompatibL has established itself as the leading provider of quantitative software and solutions for derivatives analytics, limits, and regulatory capital. CompatibL has over 200 experienced developers and financial engineers and boasts a client base of over 50 banks, central banks, supranationals and asset managers in the US, EMEA and Asia, including 4 out of 5 largest derivatives dealers. Over 140 major projects have been implemented across this client base. CompatibL is headquartered in London (UK) with the main delivery centres located in Warsaw (Poland) and Princeton (United States). An award-winning software solution for market and credit risk, regulatory capital, limits and initial margin www.compatibl.com info@compatibl.com New York CompatibL Technologies LLC 100 Overlook Center Second Floor Princeton, NJ 08540, USA London CompatibL Technologies Ltd First Floor 100 Pall Mall London, SW1Y 5NQ, UK +1 (609) 919 0939 +44 (20) 3743 8800 Singapore CompatibL Pte. Ltd. 30 Cecil Street 19-08 Prudential Tower Singapore, 049712, Singapore Warsaw CompatibL Sp. z o.o. Prosta 32 Second Floor Warsaw, 00-838, Poland +65 6813 2067 +48 (22) 110 8005

CompatibL Risk Platform Powering strategy, asset and risk management An award-winning software solution for market and credit risk, regulatory capital, limits and initial margin. CompatibL’s risk management technology was recognized by a pair of back-to-back Risk Vendor of the Year Awards in two enterprise risk management categories in 2017 and 2018. ComptibL designs and implements front-office, mid-office and back-office software for strategy, asset and risk management, utilizing the best market practices, quantitative algorithms and technical architecture. Regulatory frameworks supported ISDA SIMM Basel III FRTB IRRBB SA-CCR Alexander Sokol Quant of the year 15+ 200+ Risk years experience in software development for financial institutions. in-house experts, including quants, software engineers, solution architects, UI/UX designers and analysts in 4 branch offices. • Historical and parametric VaR • Market Risk measures: instantaneous shocks, parallel/non-parallel shocks and twists, relative and absolute, bucketed/term structure scenarios, duration, convexity • First/second-order Greeks and cross gammas: delta, gamma, vega, skew, epsilon • PFE and quantile measures • xVA (CVA, DVA, FVA, KVA, COLLVA, MVA) • What-if analysis 140 85 • Profit attribution (PnL explain and deltas reports) delivered enterprise software projects and hundreds of quantitative consultancy and model validation engagements. clients worldwide, including 4 of the 5 largest dealers, 33 central banks and some of the world’s largest asset managers. 2 / CompatibL Risk Platform CompatibL Risk Platform / 3

Components and Tools Highlights CompatibL Cloud Platform provides front-end, back-end and operation components that are designed for flexibility and can be easily customized according to the needs of the client. CompatibL provides Amazon Web Services, Microsoft Azure, and Kubernetes deployments with full support of stateless functions such as AWS Lambda or Azure Functions, with Docker containers, and enterprise level in-memory caching and docu- ment-based database solutions. Front-end Back-end Quantitative features Collateral modeling • Flexible and customized HTML5 user interface • High-performance HTML5 pivot control with virtualized rows and columns • Business intelligence module • Data grid/tables with the ability to aggregate and apply vector functions on the fly • Rich UI component and graphical control library • Excel add-in • Cloud-based solution for AWS, Azure and other cloud platforms • Batch services for Kubernetes • Distributed cache for parallel calculations based on Redis or MongoDB • Algorithmic trading components • SQL and NoSQL databases and data stores (Mongo, Redis, MS SQL Server, Oracle, etc.) • Formula engine • Messaging adapters for standard protocols including RabbitMQ, JMS, TIBCO • Bloomberg and Reuters market data adapters • Workflow manager • Dynamic model calibration – a flexible framework to tune calibration of IR/FX/ Commodity/Inflation/Equity/Credit models based on trade attributes • CSA modeling – advanced features to model the change of collateral through time, including dynamic initial margin • Classical or advanced (Andersen–Pykhtin–Sokol) model for the margin period of risk • Real-world (capital/limits) and risk-neutral modeling combined with the choice of full repricing or AMC valuation • Quantification of trade and margin flow settlement risk as part of the overall counterparty credit risk • Governance reporting to verify calculation input including trade data, market data, front-office MtM reconciliation and risk contributors Tools Advanced features • Excel add-in • Server-side Excel spreadsheet processor • Export in different formats (Excel, PDF, XML, CSV and others) • Code editor with syntax suggestions (IntelliSense) • Log analyzer • Application deployment and monitoring services • Automated testing tools • Code generation tools • Import trade, market and reference data from multiple trading and risk systems • Flexible framework to use an external model for market simulation • Fast American Monte Carlo for complex derivatives • Stress testing and drill-down based on business unit, instrument type, desk, position, maturity bucket or custom factors • Consistent model calibration for both market scenarios and deal prices • Nightly batch processing and specific design of cluster deployment • Advanced modeling of dynamic hedging and collateral rules • Customizable reports for end-user reporting 4 / CompatibL Risk Platform CompatibL Risk Platform / 5

CompatibL Risk Cloud Platform Architecture The platform can be deployed in your data center or private cloud and in most public clouds, including AWS and Azure. When deployed in the cloud, it leverages the latest serverless cloud technologies, including AWS Fargate, Lambda, Step Functions and Azure Functions. Our platform also supports both Windows and Linux traditional data centers and can run on top of all leading cluster management software solutions. CompatibL Platform is based on microservices. Microservices communicate by HTTP protocol with REST semantics. They can be hosted in Docker and deployed on any cloud/cluster infrastructure supporting Docker or similar container technologies or self-hosted on a dedicated server. CompatibL Platform includes support for traditional and serverless parallel computing, a powerful HTML5 front-end with advanced BI, the ability to integrate your analytics written in C++, C#, Java or Python, and a back-end-agnostic database adapter that supports most traditional and cloud databases. Inputs Microservices Trade Data Service User Interface Market Data Service Trade Data Credit / Why Cloud? Reference Data Market Quote Service Calculation Service Internal Rating Service Data Import Speed-up banking innovation Extend your cloud footprint Start on your project on the cloud Market Data Feed Data Upload Credit Data Service Adopt new approaches that power business innovation and drive agility and growth for banks and financial institutions. Create and build large-scale projects with CompatibL Risk Cloud while meeting complex industry requirements. Bypass legacy system limitations with cloud cost advantages and flexibility. User Authentification API Gateway/ Load Balancer In-memory Cache Document Storage Users Stateless Functions Benefits Calculate Initialize Scenario HTML5 Excel Real-time risk analytics A BI solution Full storage and customization Use of CompatibL’s valuation Build Curves Evaluate Scenario that provides the ability to create interactive re- ports quickly and easily, drawing from multiple data sources. using grid or cloud com- puting with the ability to run user-defined cal- culations on the cluster. of reporting capabilities based on HTML5 front-end technology. and risk models, or easy integration of your own quant library with user-friendly APIs in C++, C#, Java, and Python. Initialize Scenario Evaluation Clear CompatibL Rich Client Custom Applications 6 / CompatibL Risk Platform CompatibL Risk Platform / 7

Integration Solutions BI & Reporting Services CompatibL specializes in the most challenging integration projects involving complex trade and market data and advanced quant models. Optimized data cache with query API CompatibL Platform imports market data, trades and reference data from an external database, CSV files or web services. Easily map your own trade format or use one of the standard formats accepted by the software. The system runs market simulations and generates market scenarios. From there, trade PFE can be simulated with either American Monte Carlo or a full repricing technique. After that, the system calculates metrics and outputs the results for further analysis. Multiple data source types (databases, flat files, web services) Report templates several visualization controls Import CompatibL Netting data Market data Credit data Legal data Etc. Configuration Settings Aggregation categoriescan be defined dynamically Convert to CompatibL format Market simulation model PFE Metric calculation Downstream reporting calculation 100 100 90 80 70 60 Interactive drill-down control makes it possible to define the sequence of attributes for the drill down Results 8 / CompatibL Risk Platform CompatibL Risk Platform / 9

CompatibL Excel Add-in Perform risk calculations directly from Excel No need to import all the data to CompatibL Risk manually Smooth communication – changes in Excel are automatically transferred to CompatibL Risk and the other way around Work with financial data in Excel without using the CompatibL application Expressive CompatibL pricing functions exposed as Excel formulas allow vanilla and exotic trades to be modeled in an intuitive and transparent way. They allow a user to define the trade from first principles by using CompatibL functions directly on an Excel spreadsheet. For exotics, CompatibL allows a user to define trade payouts or custom rates in Python. This removes the necessity for a user to learn vendor-specific scripts or ad-hoc languages. CompatibL also provides debugging capabilities for Python, which allows the user to step through all the lines of code in Excel and see intermediate values and call stack. 10 / CompatibL Risk Platform CompatibL Risk Platform / 11