Download

1 / 8

0 likes | 3 Views

Confused about why your car insurance quote keeps changing? At Begin Insurance, we break down the key factors that influence your vehicle insurance costsu2014from your driving history and vehicle type to your postal code and coverage level. Our experts help you find the right policy at the best rate. Understand your quote betteru2014get a transparent consultation today! https://begininsurance.ca/en/blog/what-affects-the-cost-of-my-vehicle-insurance-quote

E N D

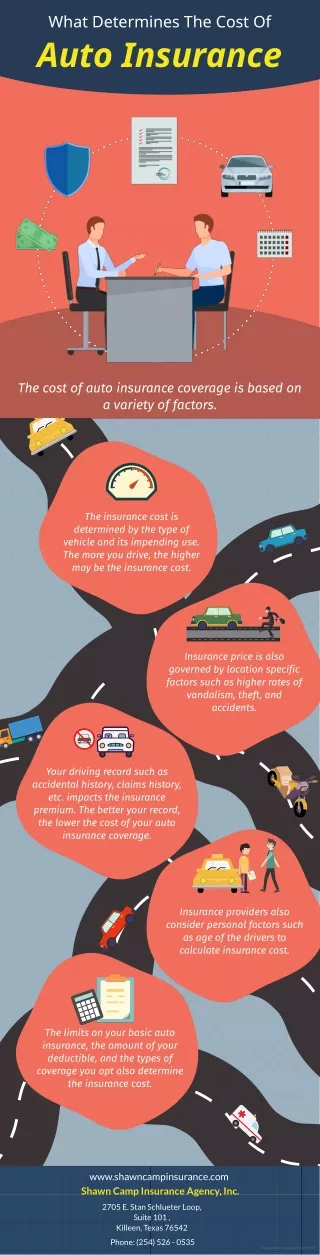

What affects the cost of my vehicle insurance quote?

Why your vehicle insurance quote may be high Your vehicle insurance quote may be high due to rising premiums across Canada and factors like your driving record, location, vehicle type, and claims history. Some factors are obvious, while others, like credit score or postal code, are less well-known. Understanding what shapes your quote helps you make informed, cost-effective choices.

Your driving profile matters • Age & experienceYoung or newly licensed drivers often face higher premiums, as they’re statistically more likely to be involved in accidents compared to older, more experienced drivers. • Driving recordSpeeding tickets, DUIs, and at-fault accidents increase your insurance rates, as they indicate risky behaviour and a greater likelihood of future claims. • Claims historyIf you've filed multiple insurance claims in the past, insurers may consider you a higher-risk customer, which can lead to increased premiums. • Credit scoreSome insurers in Ontario may (with your permission) review your credit score, as a lower score may be linked to higher claim frequency or severity.

Make, model & year • Luxury, sports, or hard-to-repair vehicles typically cost more to insure due to higher repair or replacement costs after an accident or theft. • Safety features: • Vehicles with advanced safety systems, like lane assist, airbags, or automatic braking, may qualify for discounts, as they reduce the risk of serious collisions. • Anti-theft devices: • Cars with built-in or approved anti-theft systems can earn you premium discounts by lowering the risk of theft-related claims. • CLEAR System & EVs: • Insurers use CLEAR data to evaluate claim and repair costs. Electric vehicles may cost more to insure due to limited parts and specialized repairs. Your vehicle’s influence on Insurance cost

Where and how You drive plus coverage choices • Postal code riskLocal claims data influence your premium, areas with higher accident or theft rates generally lead to higher insurance quotes. • Coverage type & deductiblesChoosing comprehensive or collision coverage increases costs, while selecting higher deductibles can reduce your monthly premium, but increases out-of-pocket costs after a claim. • Urban vs. ruralLiving in urban areas often means higher insurance costs due to increased traffic, accident risk, and vehicle theft compared to quieter rural locations. • Commute & car useDaily long-distance commuting increases your time on the road, raising the chance of collisions and resulting in higher insurance premiums.

Uncontrollable external factors that raise rates Inflation: Rising costs of repairs, parts, labour, and rental vehicles directly impact claim payouts, leading insurers to increase premiums for all drivers. Auto theft & insurance fraud: The spike in vehicle thefts and fraudulent claims means higher overall losses for insurers, which insurers offset by raising premiums, even for safe drivers. Supply chain delays: Delays in sourcing auto parts extend repair timelines and increase rental car usage, raising the total cost of claims and impacting insurance rates. Severe weather events: increasingly frequent storms, floods, fires, and hail damage lead to a higher number of claims, pushing insurers to raise premiums to balance increased risk.

How Begin Insurance helps Begin Insurance offers personalized quotes tailored to your driving profile and vehicle type. We break down how market shifts affect your premium, help uncover available discounts, and guide you through coverage comparisons, ensuring your insurance fits your needs, lifestyle, and budget with expert support at every step.

Ready to take the next step? VisitBegin Insuranceto explore tailored coverage options that fit your lifestyle. Contact our expert team today for personalized guidance or to get a free quote, and experience peace of mind with insurance made simple. What to do next?