Download

1 / 6

60 likes | 77 Views

For most students, the days of being able to easily repay your debt immediately after graduation are long behind us.

E N D

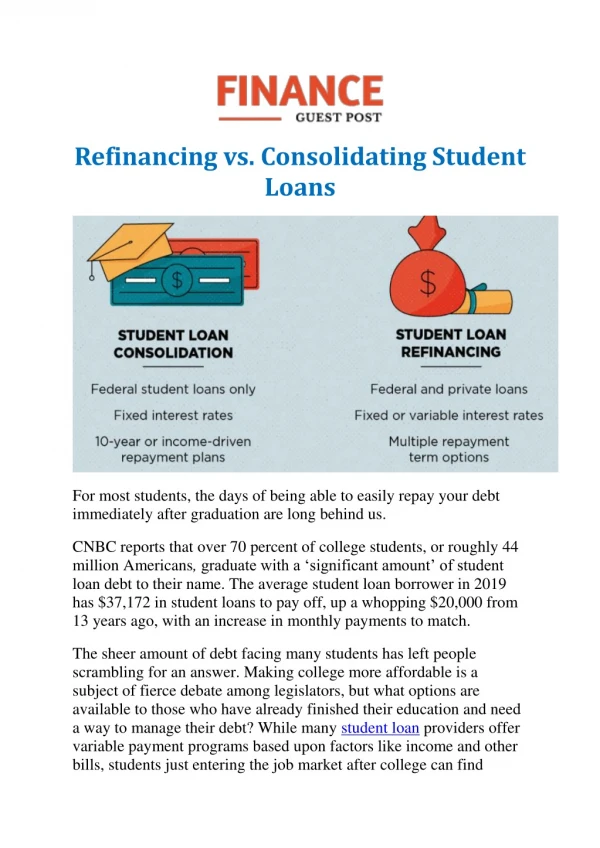

Refinancing vs. Consolidating Student Loans For most students, the days of being able to easily repay your debt immediately after graduation are long behind us. CNBC reports that over 70 percent of college students, or roughly 44 million Americans,graduate with a ‘significant amount’ of student loan debt to their name. The average student loan borrower in 2019 has $37,172 in student loans to pay off, up a whopping $20,000 from 13 years ago, with an increase in monthly payments to match. The sheer amount of debt facing many students has left people scrambling for an answer. Making college more affordable is a subject of fierce debate among legislators, but what options are available to those who have already finished their education and need a way to manage their debt? While many student loan providers offer variable payment programs based upon factors like income and other bills, students just entering the job market after college can find

themselves struggling to make even the minimum monthly payments, and falling behind on these payments can make a huge impact on their credit scores and force people into a bad financial situation that will be difficult to get themselves out of. Luckily, students are beginning to find that they’re not without options. Much like many other kinds of long-term personal loans, student loans can be refinanced or consolidated to lower the minimum monthly payment in an attempt to get a better handle on your overall financial wellness. For any recent college graduate reading this (or even a not-so-recent graduate who still struggles with loan payments, as many do much later in life), these ideas are probably already starting to sound pretty appealing. It’s important to note, however, that each of these different options can have a massively different impact on your finances, and which option is right for you (if either option is right at all) will depend heavily on your personal circumstances. Student Loan Refinancing Student loan refinancing works very similarly to the refinancing options available for other types of loans, like auto loans and mortgages. Student loan refinancing is when a new loan is taken out and used to pay off existing debt. Essentially, you apply for a personal loan through a private financial institution, such as a bank or credit union, and use that loan to pay off your existing student loans. You then repay the new loan over the agreed-upon period of time, just like you would with an auto loan or home loan. The goal of student loan refinancing is to obtain more favourable payment terms and an overall lower interest rate than your previous student loan. This way, even if your overall amount of student debt remains to be paid off, you can do so with a more forgiving interest rate so that you pay less interest over time. In addition to helping you save money on interest in the long run, student loan refinancing can help you pay off your debt faster if you choose a loan with a shorter repayment term.

Every lender is unique, but generally speaking, lenders will consider you a good candidate for student loan refinancing if you have stable income, a credit score that is about 650 or higher, and have a low debt-to-income ratio. Student Loan Consolidation Student loan consolidation is similar to refinancing in the sense that it replaces several existing loans with one new loan, but it’s executed differently. Instead of applying for a new loan to completely pay off your existing loan, student loan consolidation is the process of gathering all of your smaller loans into one big, comprehensive loan with a more stable set of payment terms, such as interest rate. Most student loans actually consist of several smaller loans given out at the same time, both at the federal and private levels, and these individual loans can all have different terms. Consolidating these loans together into one monthly payment can streamline the repayment process. Student loan consolidation can be used for many different types of student loans, but there are some requirements you’ll need to meet. To be eligible for consolidation, your loan will need to either be in repayment or in the grace period. If your loan has a grace period, this typically begins when you graduate, when you stop attending school, or if you’re considered to be enrolled less than half-time. Some types of education-related loans that are ineligible for student loan consolidation include loans that were used for K-12 education instead of college education and loans for post-graduate expenses, such as bar exam prep loans. You also won’t be able to consolidate loans that originated outside of the United States or that were not used for qualified education expenses. Refinance vs. Consolidation: Which Is Right for Me? The most important thing to remember when it comes to refinancing student loans or consolidating them is that the two options apply to a

number of pretty different situations, and the option that works best for one borrower may not work for another. For example, as explained by Forbes, student loan consolidation is primarily used as an organizational tool. If your consolidation involves federal loans (and since federal student loans are among the most common student loan type, there’s a good chance that it will) the interest rate on your payments won’t actually decrease. Instead, your new consolidated interest rate is the weighted average of the interest rates on your existing loans, and then rounded up to the nearest ⅛%. The odds are good that this won’t actually cause your interest rate to decrease like it would with refinancing, so you may not save much money through this option, depending on the exact nature of your existing student loans. Another important thing to note about student loan consolidation is that if you choose to go this route, the outstanding interest on your existing loans will become part of the principal balance of the new loan you take out to pay them off. And even if loan consolidation can give you lower monthly payments, remember that you may be making lower monthly payments over a longer period of time, which means you may pay more interest in the long run. In the case of student loan refinancing, it’s important to note that if you want to have lower loan payments each month, the trade off might be a longer repayment term, which means that you’ll pay more interest over time than you would with a shorter-term loan. Lenders also might not consider you a good candidate for student loan refinancing if you are unemployed/underemployed or if you’ve defaulted on your existing student loans. Student loan refinancing also might not be an ideal option if your student loans are federal loans. It’s also important to note that, depending how you initially got your loans, refinancing may force you to miss out on some good perks. USC Credit Union points out that refinancing will cause you to lose any benefits that come with your initial federal loans.

Yes, it’s true: some types of student loans actually do come with benefits. In many cases, federal student loans offer access to programs like federal debt relief, income-based repayment, or even debt forgiveness through public service, such as working a civil service job. Since refinancing pays off your initial loans and replaces them with a new loan, it would mean that you would no longer be able to take advantage of these types of benefits. If your loan includes any of these forgiveness or relief programs, you may want to do the math to figure out if they would be a better long-term option as opposed to completely refinancing the loan. It’s also worth noting that if you have a combination of federal and private student loans, refinancing might still be an option worth considering. In this case, you may be able to refinance your private loans to get more favorable terms on those and leave your federal loans as they are. That way, you may be able to have the best of both worlds by saving money on some of your loans without giving up the benefits that come with some of your other loans. Another important thing to keep in mind is that, regardless if you choose to consolidate or refinance your student loans, you might need someone to cosign for your new loan. If you don’t quite meet a lender’s requirements for a loan, having a cosigner could help you get approved when you’d otherwise be turned down. Even if you could get a loan to refinance or consolidate your student loans on your own, having a cosigner might help you get even more favorable terms on your new loan. However, given the risks that come with cosigning a loan for someone else, finding someone to cosign for you might not be so easy. The Big Question Which of these options would benefit your own specific situation the most? That’s really the most important question to ask yourself. Figuring out the answer might involve some math (and nobody likes math other than math majors) but reviewing all your options carefully will help you make the right decision and hopefully have an easier time being one of the few and the proud with no more student loan

debt. Author Bio: Angela is a Michigan-based writer who enjoys writing about a wide range of subjects, ranging from film to personal finance. To read more articles visit: https://www.financeguestpost.com/