Download

1 / 7

70 likes | 86 Views

Before you apply for your first credit card, check out our list of things that you might unintentionally miss out!

E N D

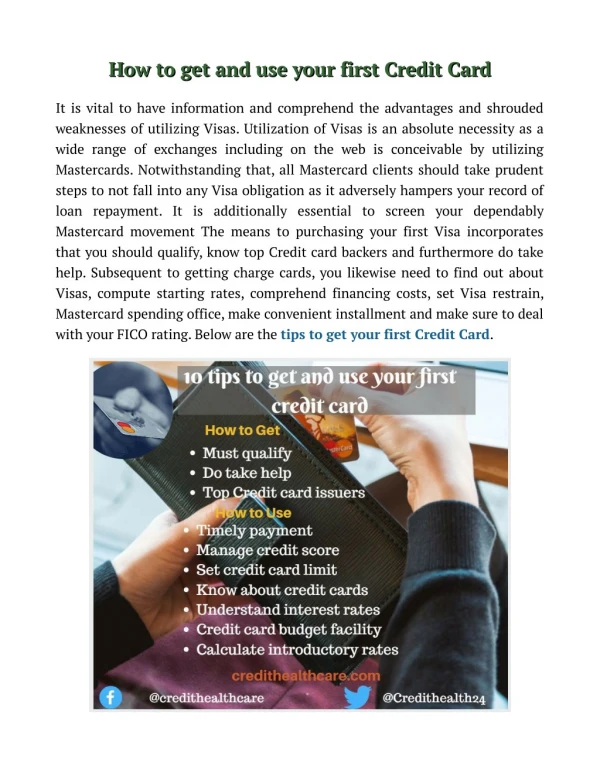

Applying For Your First Credit Card? Here’s What You Need To Know If you have already started working for at least a year, chances are that you’ll probably already have your first credit card. Or, you might be thinking of getting one. Well, you’re in luck! But before we get into the nitty-gritty details about the world of credit cards, let’s start with the basics. A credit card is a facility that is used all over the world including in Singapore. It gives you convenience, speed and efficiency when making payments. Even with these benefits, some of us might be a little apprehensive when applying for credit cards. However, there is no need to fear if you are well versed on how credit cards work. Individual discipline and organization is key for one to experience the benefits of having a credit card. What To Take Note Of Before Applying For A Credit Card If you are planning to apply for a credit card in Singapore, do take note of the following points before you submit your credit card application: 1. Don’t rush You should take your time and do a full assessment of the bank that is offering the credit card. It is best to have a full understanding of all the terms and conditions that go along with having a credit card. Making a rash decision can lead to terrible regrets and losses. 2. Focus on the need

There are several types of credit cards offered in the market. You should carefully check the pros and cons of each card and match this with your needs. Different cards have different benefits. For instance, some offer more perks for dining, entertainment, while some offer rewards that can be converted to air miles. Be sure of what you need the credit card for. 3. Compare the different options especially costs and benefits Different credit cards have different costs. Some things to compare are the interest rates, annual fees and benefits. Benefits come in the form of cash backs, travel insurance, reward programs and other similar rates. This will help you pick a card that you will get the maximum benefit from at a minimum cost. 4. Check the eligibility requirements You should ensure that you meet all the eligibility requirements before they submit your application. This is a simple checklist to make sure that the application is not rejected because a simple requirement was not met. 5. Check one’s credit rating You should request for your credit rating before applying for a credit card. You can do so on the Credit Bureau Singapore website. However, if this is your first credit card, and you have not taken up any loans before, your credit rating will not be reflected. That said, most banks will approve of your credit card application as long as you meet their minimum annual income cap. However, if you have a poor credit rating, it will be wise for you to make an effort to improve the credit rating before applying for the credit card. 6. Pay off outstanding balances on other credit cards If you have other credit card debt that is left unpaid, be sure to do so before applying for a new one.

Unpaid credit card debt paints a negative picture on your credit rating and can significantly lower your chances of getting the credit card approved. 7. Open an account in the bank concerned This is not a must-have, but it can score you extra brownie points in some scenarios. By opening an account with the bank, it will enable the card to be approved much soonerbecause your details are already stored in the bank’s system. In addition, the bank will be able to confirm your income if the account opened is a salary account. 8. Check that details are correct and attach all required documents When applying for a credit card, a few documents and information are needed. One needs to be careful to read through the terms and conditions and give all the details required as well as attach the documents needed. This will speed up the approval process. 9. Be transparent about your income You should never overstate your income because this is considered as fraud. On the other hand, you should also not understate your income because the bank may doubt your ability to service a debt. 10. Apply for only one card at a time While the allure of applying for multiple credit cards and receiving many freebies are tempting, you should only limit yourself to applying for one credit card at a time. By applying for multiple credit cards, this might cause the bank to make a negative conclusion about you and assume that you have taken more debt than you can handle. Once you have considered all the above points, you can now proceed to apply for the credit card, having satisfied the following eligibility conditions in Singapore: •Must be above 21 years. •Should be a Singaporean, permanent resident, or foreigner living in Singapore.

•For Singaporeans and permanent residents, the minimum income per annum should be S$ 30,000, and for foreigners the minimum income per annum should be S$ 45,000. •The credit score or credit rating of the applicant will be considered when issuing the credit card because it shows the applicant’s creditworthiness. What Are The Charges That I Can Expect With A Credit Card? If you are successful in your application for a credit card, here are some of the charges you can expect along with a credit card: 1. Finance charges or interest In Singapore, the average interest rate for credit cards is 25.9% per year. However, if you do not pay the full amount of your credit card bill, you will be charged an extra 2% per month. This additional interest can become very expensive, so it is better to pay the bills in full every month. 2. Late charges This is charged when the applicant fails to pay the amount on the due date. Some banks have a grace period of one day, but not all of them.

3. Annual fees Annual fees are actually the annual cost that the applicant will pay for enjoying the benefit of having the credit card. The annual fees usually cover administrative costs. In Singapore, annual fees are averaged at S$192. Annual fees can actually be avoided. A trick is to call up your bank and request a waiver of your annual fees. If the bank is unwilling, you always have the option of cancelling your card. In most scenarios, banks will waive off the annual fee. 4. Transaction fees For those credit card holders who make purchases from outside Singapore, there is a small transaction fee that is loaded onto the cost of the item bought. This fee differs with each credit card. Here Are Some Of The Typical Credit Cards That You Can Apply For In Singapore, the applicant will have a choice of three major credit card networks, namely Visa, MasterCard and American Express. Among these three networks, there are also three main categories of cards, which are described below: •Air Miles Credit Cards This type of card helps you to earn air miles based on your credit card spendings. For instance, some air miles credit cards award you 1 air mile for every $1 spent. These air miles can then be converted into actual plan tickets. It is a good choice for those who have a high income and a high monthly expense. •Cashback Credit Cards This card provides you with a rebate as you spend, though there is a minimum threshold of spending that you will have to achieve to receive a bonus cashback. This card is ideal for those who have a lower expenditure per month.

•Rewards Credit Cards This card gives you rewards of points whenever cash is spent on the card. However, there is a minimum amount that must be spent for a bonus reward of points to be received. These points can be used to redeem air miles, vouchers, etc. A rewards credit card can be used by a cross-section of individuals. Oh No! I Have Racked Up Multiple Credit Card Debt. What Should I Do? If you have fallen into the credit card debt trap, the first thing you should do is to make an effort to repay all of your debts. Snowballing them will only incur additional interest and unnecessary late payment fees. With that said, we know how much easier it is said than done. What happens if your credit card debt runs into the thousands? For some of us, procuring tens of thousands to pay off our credit card debt can be quite a challenge. While the easiest option is to seek help from relatives and friends, this can cause the relationship to sour.

The next option you might be thinking of is to take out a loan from a bank. However, banks usually have a long and tedious application process which might not be in your favour, especially if you have to pay off your credit card debt as soon as possible. During instances like these, a personal loan from Credit 21 can provide swift help to pay off all your credit card debt. Our loan application process is quick, hassle-free and simple! All you have to do is to submit an online enquiry with us, and we will get back to you within minutes! In most scenarios, our borrowers are able to receive their loan within the hour. This way, you will get to settle your credit card debt immediately!