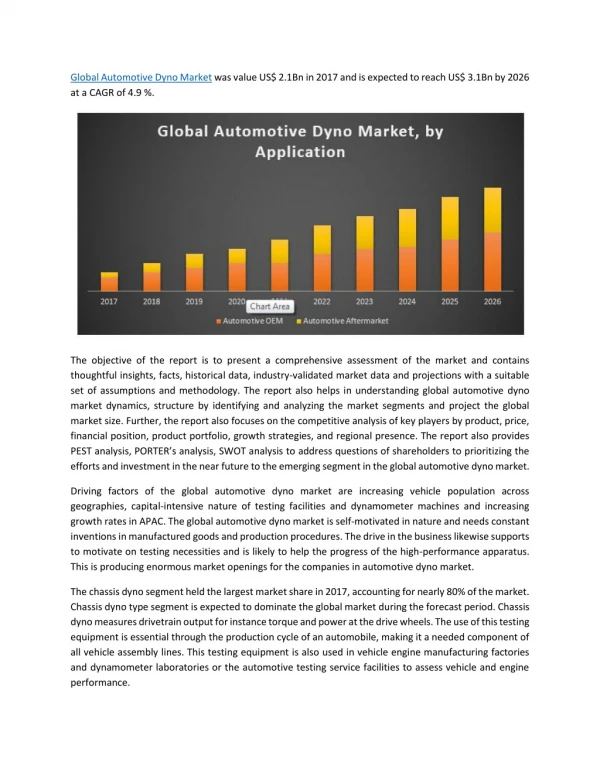

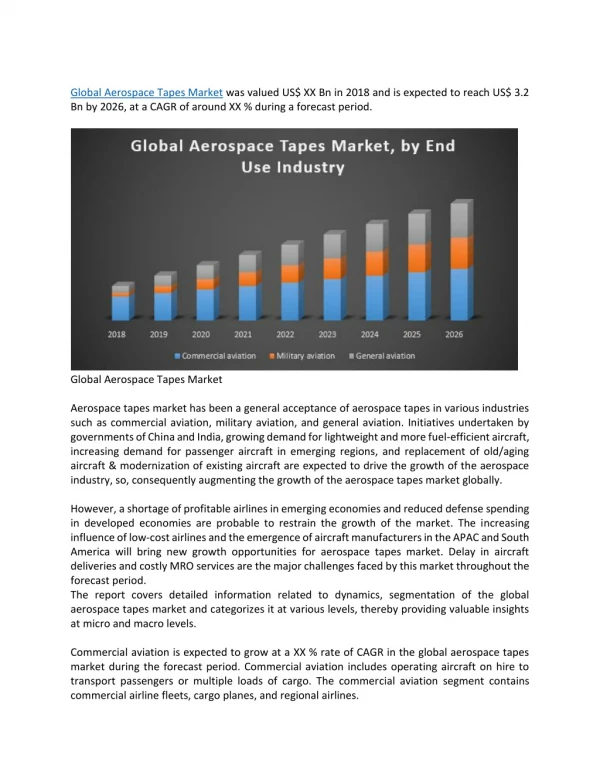

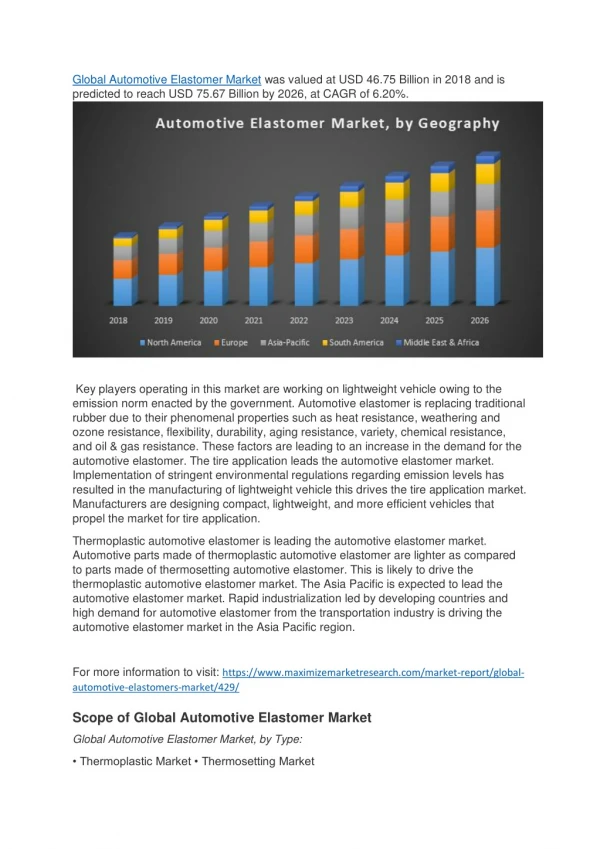

Global Automotive

Global Automotive Presenter: Industry----Frank GM----Raymond Toyota----Angela Volvo---Lillian Global Auto Sales The growing importance of Emerging Market Surprise! Surprise! QUICK EXPANSION

Global Automotive

E N D

Presentation Transcript

Presenter: • Industry----Frank • GM----Raymond • Toyota----Angela • Volvo---Lillian

Surprise! Surprise! • QUICK EXPANSION • The production for the next 20 years will be more than what’s been made for the entire 110 years of auto industry history • BRIC, especially China has been, and will be the major driving force of global Auto industry • Expected to replace Japan as the second largest market

Continuous Growth in Global Automobile Industry • Global Vehicle Ownership Estimation: Over 1 billion units in 2010

Major Countries Click here

Industry Characteristics---Major Cost • Labour & Pension plans**** • N.A companies face a large amount of pension cost----approx. $1500 per vehicle • Jap companies have none pension cost • Material • Hundreds of pieces purchased from suppliers • Automakers absorb only part of the increase in material cost • Advertising

Highly sensitive to aggregate economic performance U.S economy will slow down from 3.2% GDP growth to about 2% The effect of democratic victory in congress?? Industry Characteristics---Sales cycle

Industry characteristics---M/A, Alliance • Technology, R/D • Market penetration • Global cooperation

Industry characteristics---M/A, Alliance • GM:---200 Garage Car makers in early days ---SAAB, Daewoo ---Isuzu, Subaru, Suzuki • Ford---Jaguar, Land Rover, Volvo, ----Mazda • Benz---Chrysler • Renault---Nissan

Threat of New entrants • Emergence of foreign competitors with Capital, technology and management skills • Chinese & India brands within their own countries

Suppliers • Had little power before • Been hit hard in Major Automaker cost cutting • Globalization • merger and acquisition • Increased tension b/w suppliers and Automakers

Supply Chain (traditional) Tier 3 Raw Material Tier 2 Small parts Tier 1 components OEM Design& assemble

Supply Chain (emerging) Raw Material Supplier Global Standardized–Systems Manufacturer Component specialist Systems Integrator

Outsourcing production---to more suppliers Percent of Car Value outsourced

Suppliers --Cost cutting requirement of Automakers

Suppler (cont) • A major suppler Collins & Aikman halted delivery to Ford on Oct 19th • Caused temporary shut down of one of the biggest assembly line of Ford • Foreseeable---

One of the largest supplier Dana has been added to the list (April 2006)

Substitutes • Public transportation on the rise

Rivalry • Fierce competition • High competition cost • Low return • Historically avoid price competition • More and More price competition

Buyers • Historically, the automaker power went unchallenged • As the market saturate, more options made available, buyers have significant amount of power

Regulation • Regulations • Emission standard*** • Safety standard

European Union: “ACEA agreement” seeks 25% reduction in vehicle CO2 emissions levels by 2008 (from 1995 levels). Agreement may be extended an additional 10% by 2012. • Japan: requires 23% reduction in vehicle CO2 emissions by 2010 (from 1995 levels). • Australia: voluntary commitment to improve fuel economy by 18% by 2010. • Canada: has proposed a 25% improvement in fuel economy by 2010. • China: Introduced new fuel economy standards in 2004; weight-based standards to be introduced in 2 phases (2005 and 2008). • California: CARB approved GHG emissions reductions for automobiles, currently under legislative review. • New York: Clean Cars Bill proposing to follow California standards is currently in committee. Several other NE states have indicated they will follow CA’s lead.

Comparison of Fuel Economy and GHG Emission Standards An and Sauer, 2004 for the Pew Center on Global Climate Change

Aggregate Value ExposureEstimated cost per vehicle to meet “most likely” carbon constraint scenarios in US, EU and Japan 8 25x difference in Value Exposure across the industry

Management Capacity for Low-Carbon TechnologiesMeasure of OEMs’ capacity to develop and commercialize main low-carbon technologies: hybrids, diesels & fuel cells 9

In addition • Political issues • Trade barrier • tariff • Energy crisis • OPEC • Political & Natural reasons • Technology development • Hybrid, Fuel cells, Hydrogen, Electronic, ethanol. Etc • System feature & design

Key success factors • Pension fund management • How well the company digest what’s been eaten • Supplier relationship management • Risk management (i.e. exchange exposure risk, commodity price risk) • design, marketing of new models • New technology development

General Motors Symbol: GM Exchange(s): NYSE Industry: Consumer Products (Automotive)

As of Nov 7, 2006 Dividends Per Share: 1.00 Number of Shares: 565,610,000

Company Profile • The world's largest automaker • has been the global industry sales leader for 75 years • employs about 327,000 people around the world • manufactures its cars and trucks in 33 countries • Engaged in automotive production and marketing and financing and insurance operations • largest operating presence in North America

EXECUTIVE PROFILES G. Richard Wagoner, Jr.GM Chairman & Chief Executive Officer • Since June 2000 • BA in economics from Duke University • MBA from Harvard Business School Frederick (Fritz) A. HendersonGM Vice Chairman and Chief Financial Officer • BBA from the University of Michigan • MBA from Harvard Business School Robert A. LutzGM Vice Chairman, Global Product Development • BA in production management from the University of California-Berkeley • MBA from the University of California-Berkeley • degree of doctor of management from Kettering University

Buick Cadillac Chevrolet Fleet & Commercial Operations Holden Vauxhall GMC GM Daewoo HUMMER Pontiac Saturn Saab Opel Brands

GMAC Financial Services • A finance company • offers automotive, residential and commercial financing and insurance

GM's OnStar subsidiary • a provider of vehicle safety, security and information services • use (GPS) satellite and cellular technology to link the vehicle and driver to the OnStar Center • advisors offer real-time, personalized help 24 hours a day, 365 days a year

Global Partnerships • majority shareholder in GM Daewoo Auto & Technology Co. of South Korea • Product, powertrain and purchasing collaborations with Suzuki Motor Corp. and Isuzu Motors Ltd. of Japan • Advanced technology collaborations with • DaimlerChrysler AG • BMW AG of Germany • Toyota Motor Corp. of Japan • Vehicle manufacturing ventures with • Toyota • Suzuki • Shanghai Automotive Industry Corp. of China • AVTOVAZ of Russia • Renault SA of France