Download

1 / 1

0 likes | 4 Views

NPS Scheme: Government-backed plan offering flexibility, tax benefits, and long-term security.<br><br>Visit - https://www.utipension.com/why-nps-national-pension-scheme-india?utm_source=infographic&utm_medium=organic&utm_campaign=info_key_reasons_to_invest_in_nps

E N D

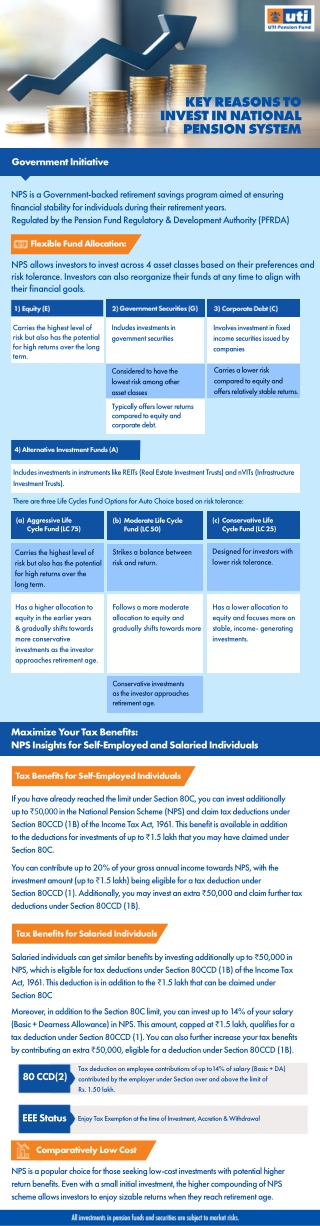

KEY REASONS TO INVEST IN NATIONAL PENSION SYSTEM Government Initiative NPS is a Government-backed retirement savings program aimed at ensuring financial stability for individuals during their retirement years. Regulated by the Pension Fund Regulatory & Development Authority (PFRDA) Flexible Fund Allocation: NPS allows investors to invest across 4 asset classes based on their preferences and risk tolerance. Investors can also reorganize their funds at any time to align with their financial goals. Includes investments in government securities Carries the highest level of risk but also has the potential for high returns over the long term. Involves investment in fixed income securities issued by companies Carries a lower risk compared to equity and offers relatively stable returns. Considered to have the lowest risk among other asset classes Typically offers lower returns compared to equity and corporate debt. 4) Alternative Investment Funds (A) Includes investments in instruments like REITs (Real Estate Investment Trusts) and nVITs (Infrastructure Investment Trusts). There are three Life Cycles Fund Options for Auto Choice based on risk tolerance: (c) Conservative Life Cycle Fund (LC 25) (a) Aggressive Life Cycle Fund (LC 75) (b) Moderate Life Cycle Fund (LC 50) Designed for investors with lower risk tolerance. Strikes a balance between risk and return. Carries the highest level of risk but also has the potential for high returns over the long term. Has a higher allocation to equity in the earlier years & gradually shifts towards more conservative investments as the investor approaches retirement age. Follows a more moderate allocation to equity and gradually shifts towards more Has a lower allocation to equity and focuses more on stable, income- generating investments. Conservative investments as the investor approaches retirement age. Maximize Your Tax Benefits: NPS Insights for Self-Employed and Salaried Individuals Tax Benefits for Self-Employed Individuals If you have already reached the limit under Section 80C, you can invest additionally up to ₹50,000 in the National Pension Scheme (NPS) and claim tax deductions under Section 80CCD (1B) of the Income Tax Act, 1961. This benefit is available in addition to the deductions for investments of up to ₹1.5 lakh that you may have claimed under Section 80C. You can contribute up to 20% of your gross annual income towards NPS, with the investment amount (up to ₹1.5 lakh) being eligible for a tax deduction under Section 80CCD (1). Additionally, you may invest an extra ₹50,000 and claim further tax deductions under Section 80CCD (1B). Tax Benefits for Salaried Individuals Salaried individuals can get similar benefits by investing additionally up to ₹50,000 in NPS, which is eligible for tax deductions under Section 80CCD (1B) of the Income Tax Act, 1961. This deduction is in addition to the ₹1.5 lakh that can be claimed under Section 80C Moreover, in addition to the Section 80C limit, you can invest up to 14% of your salary (Basic + Dearness Allowance) in NPS. This amount, capped at ₹1.5 lakh, qualifies for a tax deduction under Section 80CCD (1). You can also further increase your tax benefits by contributing an extra ₹50,000, eligible for a deduction under Section 80CCD (1B). Tax deduction on employee contributions of up to14% of salary (Basic + DA) contributed by the employer under Section over and above the limit of Rs. 1.50 lakh. 80 CCD(2) EEE Status Enjoy Tax Exemption at the time of Investment, Accretion & Withdrawal Comparatively Low Cost NPS is a popular choice for those seeking low-cost investments with potential higher return benefits. Even with a small initial investment, the higher compounding of NPS scheme allows investors to enjoy sizable returns when they reach retirement age.