Download

1 / 6

0 likes | 17 Views

Being a freelancer or self-employed comes with its own set of challenges, and one of the most important considerations is insurance.

E N D

3 Types of Insurance Policies for Freelancers and Self-Employed Being a freelancer or self-employed comes with its own set of challenges, and one of the most important considerations is insurance. Whether you’re a freelance writer, graphic designer, or consultant, having the right insurance policies can provide peace of mind and protect your business from unforeseen events. But with so many options available, it can be overwhelming to determine which insurance policies are essential for your specific needs. Luckily for you, I’ve been a full-time personal finance freelance writer for the past 6 years, so you can say I have some knowledge on this topic. Let’s get started. To begin, let’s define what self-employed and freelancer mean Self-employed individuals and freelancers are a growing and diverse group in the workforce. Being self-employed means that individuals work for themselves and are responsible for their own earnings and business operations. Freelancers, on the other hand, are individuals who are hired for temporary or short-term work without being employed on a long-term basis. Both self-employed individuals and freelancers have the flexibility to work on their own terms, set their own schedules, and choose their clients or projects.

However, they also face the challenges of managing their own businesses, finding clients, and handling their own finances. Understanding the definitions and distinctions between self-employment and freelancing is important for anyone considering a career in this type of work. I will also use the terms freelancer and self-employed interchangeably from her, so take note. Types of insurance policies freelancers and self-employed individuals need It’s important for freelancers to carefully assess their specific risks and needs to determine which insurance policies are most appropriate for their individual circumstances. Professional Liability Insurance Professional liability insurance, also known as errors and omissions insurance, is crucial for professionals who provide services and advice to clients. This type of insurance helps protect individuals and businesses from bearing the full cost of defending against a negligence claim made by a client, as well as damages awarded in such a civil lawsuit. For those in professions such as accounting, architecture, law, real estate, and healthcare, professional liability insurance is essential in safeguarding their finances and reputation in case of a lawsuit alleging errors, omissions, or negligence in their services. Professional liability insurance covers legal expenses, damages, and settlements that may arise from allegations of negligence, errors, or omissions in the services provided. For freelance professionals, professional liability insurance is crucial as it provides coverage for claims related to personal injury, property damage, and financial losses. Protecting your business and personal assets in case of a lawsuit or claim is important. Who Should Consider this Coverage? Independent workers such as freelancers, consultants, and contractors face specific risks in their jobs that vary based on the type of work performed. For specific professions, such as lawyers, financial advisors, and real estate agents, professional indemnity insurance is usually compulsory before you begin your practice. Freelancers in creative fields, for example, may face intellectual property disputes or copyright infringement claims, while consultants may be at risk for professional liability lawsuits. Additionally, some larger businesses may require freelancers to have professional liability insurance in place before they can work with them. This is because it protects both parties in case of any disputes or legal issues.

Overall, it’s important for independent workers to carefully consider the specific risks associated with their type of work and to ensure they have the appropriate business insurance to mitigate those risks. Benefits of Professional Liability Insurance Professional liability insurance offers a range of benefits for professionals in various fields. One of the main advantages is coverage for legal expenses and judgments in the event of a lawsuit over the quality of professional services. This means that if a client sues over errors, omissions, or negligent acts, the insurance can help cover the costs associated with defending the claim and any potential settlements or judgments. This insurance is particularly important for freelance professionals, as they may not have the same level of protection as employees of larger companies. It can also provide peace of mind and financial security for independent contractors who work directly with clients. Health Insurance Health insurance is a vital form of coverage designed to help individuals and families manage healthcare costs. From routine doctor visits to emergency surgeries, health insurance can provide financial protection and peace of mind during times of illness or injury. What is Health Insurance? Health insurance covers various healthcare expenses, including doctor’s visits, hospital stays, surgeries, prescription medications, and medical tests. This insurance aims to help individuals manage the high costs associated with healthcare and medical treatment. Health insurance can be particularly valuable for freelancers or self-employed individuals as it provides a safety net for unexpected medical expenses. Depending on the country, health insurance can typically be obtained through private insurance companies, employers, or government-run health programs. In some countries, freelancers may have access to government-subsidized health insurance options that provide affordable medical expense coverage. Regardless, self-employed individuals should consider health insurance beyond what governments offer, and a private health insurance plan is your answer.

Benefits of Private Health Insurance Private health insurance provides valuable coverage for individuals, including wellness visits, preventative care, and major medical bills. This type of insurance ensures that policyholders can afford routine check-ups and preventative screenings, reducing the likelihood of more serious health issues in the future. In the event of a major medical event or unexpected illness, health insurance offers financial protection by covering a significant portion of the costs, preventing individuals from facing exorbitant medical bills. For small business owners and freelancers, private health insurance offers crucial protection against incurring large debts due to healthcare costs. Without the safety net of employer-provided health insurance, self-employed individuals are particularly vulnerable to the financial burdens associated with medical treatment. Health insurance allows small business owners and freelancers to access necessary healthcare services without putting their livelihoods at risk. It provides peace of mind knowing that they can afford to seek medical care when needed without facing overwhelming expenses. Pre-Existing Conditions and Medical Bills If you have pre-existing conditions, such as diabetes or high blood pressure, it may impact your medical bills and insurance coverage. You might not receive coverage or be excluded for some conditions, depending on the insurers’ underwriting process. To navigate insurance coverage for these conditions, you may need to provide detailed medical records and work closely with your healthcare provider to ensure that your treatments and medications are covered. Specific medical bills related to pre-existing conditions can include prescription medications, specialist visits, and ongoing treatments. To manage medical expenses related to pre-existing conditions, consider negotiating with healthcare providers for extra loading or exclusions, as coverage is better than no coverage. Additionally, access community resources such as free clinics or support groups that may offer assistance with medical expenses. It’s important to be proactive in seeking out financial assistance and exploring all available options to manage these costs.

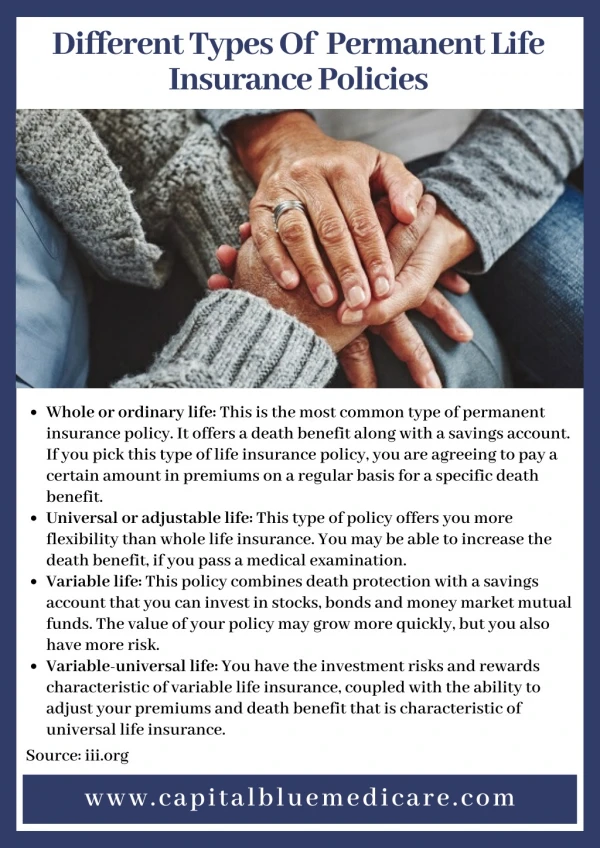

Life Insurance Life insurance is another type of insurance policy that freelancers and self-employed individuals must consider. What is Life Insurance? Life insurance, also known as income protection insurance, provides financial protection to your beneficiaries in the event of your death. It is a contract between you and the insurance company, where you pay regular premiums in exchange for a lump sum payment, known as the death benefit, to be paid out to your beneficiaries upon your (unfortunate) death. Life insurance aims to provide financial support to your loved ones, such as your spouse, children, or other dependents, to help cover expenses like funeral costs, mortgage payments, or ongoing living expenses. Life insurance can be particularly important for freelancers and self-employed individuals who may not have access to employer-provided life insurance benefits. Types of Life Insurance You can choose from two main types of life insurance policies: term life insurance and whole life insurance. Term life insurance provides coverage for a specific period of time, such as 10, 20, or 30 years. It is generally more affordable and straightforward compared to whole life insurance. If the policyholder passes away during the term, their beneficiaries receive a death benefit. However, if the policyholder outlives the term, the coverage ends and there is no payout. On the other hand, whole life insurance provides coverage for your entire lifetime. It includes a death benefit and a cash value component that grows over time. This cash value can be accessed by you during your lifetime, either through withdrawals or loans. Whole life insurance is more expensive than term life insurance, but it offers lifelong coverage and potential cash value accumulation. When deciding which type of life insurance to choose, freelancers and self-employed individuals should consider their specific needs and financial goals. Term life insurance may be suitable for those who want coverage for a specific period, such as until their children are financially independent or until their mortgage is paid off.

On the other hand, whole life insurance can provide lifelong coverage and the potential for cash value accumulation, making it a good option for those looking for long-term financial protection and potential investment growth. Conclusion: Navigating Insurance as a Freelancer or Self-Employed Individual In conclusion, navigating the world of insurance as a freelancer or self-employed individual is a crucial aspect of safeguarding your financial future and ensuring the stability of your business. The complexities and unique challenges that come with freelance and self-employment make it essential to have a well-thought-out insurance strategy. Professional liability insurance stands out as a fundamental necessity, offering protection against potential legal claims arising from your professional services. This coverage is not just a safety net but a vital aspect of maintaining your professional reputation and financial security. Health insurance is equally important, providing a buffer against high healthcare costs. As a freelancer or self-employed individual, having access to medical care without the burden of overwhelming expenses is not just a matter of health, but also of financial prudence. Life insurance, often overlooked, plays a critical role in ensuring the well-being of your dependents. Whether you opt for term life or whole life insurance, the peace of mind that comes with knowing your loved ones are financially protected cannot be overstated. As you chart your course in the dynamic and often unpredictable world of freelancing or self- employment, remember that the right insurance policies are not just expenses; they are investments in your business, your health, and your family’s future. By carefully assessing your needs and choosing the appropriate coverage, you can focus on what you do best, secure in the knowledge that you are well-protected against the uncertainties of life. Visit - https://profinanceblog.com/