Download

1 / 7

70 likes | 83 Views

When considering buying life insurance, many people often get confused between a term plan and whole life insurance. Many also tend to opt for term plans initially as these are generally more affordable. They may later wonder whether they should have instead opted for whole life insurance. Do you find yourself having similar doubts? If so, this article is just for you. Read on to learn about the coverage you can expect from term plans and whole life insurance.

E N D

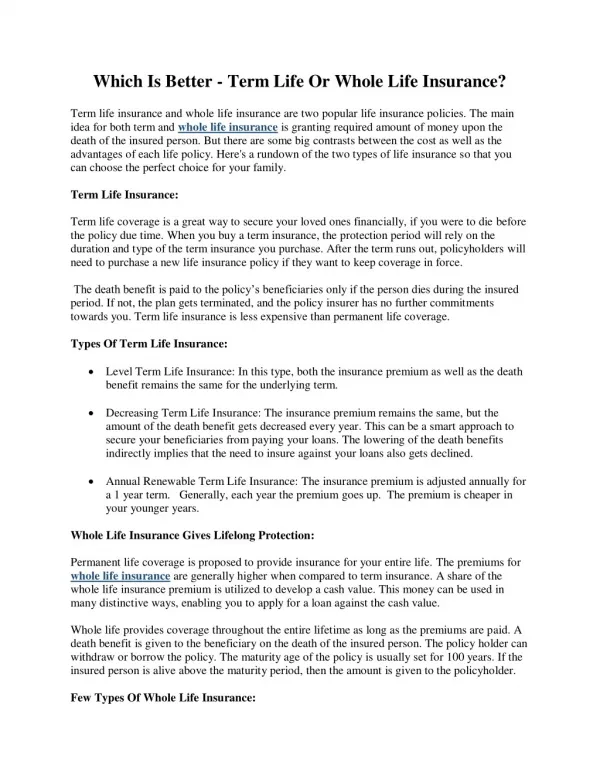

What Is The Difference Between Term Life And Whole Life Insurance?

When considering buying life insurance, many people often get confused between a term plan and whole life insurance. Many also tend to opt for term plans initially as these are generally more affordable. They may later wonder whether they should have instead opted for whole life insurance. Do you find yourself having similar doubts? If so, this article is just for you. Read on to learn about the coverage you can expect from term plans and whole life insurance.

Let’s Start With The Basics – What Gets Covered In Life Insurance? You get two main options when purchasing life insurance – term life insurance and whole life insurance. Let’s quickly see how each of these covers you – • Term life insurance covers you for a certain duration (term) selected by you when you start the plan. You get coverage against death, terminal illness, and total permanent disability. • Whole life insurance covers you for your whole life against death, terminal illness, and total permanent disability. Since term plans only cover you for a fixed period, the premiums for these are generally more affordable. Whole life insurance is relatively costlier; however, it does come along with its own share of offerings such as cash value upon surrender. Moreover, whole life insurance plans cover you for the entirety of your life – you do not need to renew coverage after a certain period. That kind of lasting protection can truly give peace of mind. At the same time, a term plan can prove more affordable and help you quickly come under the umbrella of life insurance despite all other financial obligations you may have.

Seeing as term plans and whole life insurance each have their own unique benefits, which one is better? Honestly, there is no single answer to that. The choice between the two really depends on what you uniquely expect from life insurance.

So, how do term plans and whole life insurance plans work for different people? Let’s answer that question with the help of a few scenarios – Scenario 1 – Sandra’s daughter is now in school. In a few years, she will go abroad to attend university. Sandra wants to ensure that her daughter will be able to complete her higher studies no matter what. She takes a term plan for 15 years to fully cover the entire period from now till the year when her daughter will complete university. If something unfortunate happens to Sandra, her daughter will still be able to afford her studies with the term plan payout. In this case, Sandra does not necessarily need to opt for whole life insurance as the term plan covers her for the exact purpose she needs it for, at an affordable price. Scenario 2 – Eric is 30 years old and getting married this year. He has taken a term plan for 30 years in his 20s as it fit his budget back then. However, he is now thinking of extending his coverage for more years (preferably for his entire lifespan) so that his spouse stays financially covered if he passes away before her. Eric might want to switch over to a whole life insurance plan. While the premiums might be higher, he will have peace of mind knowing his partner will be financially secured in her senior years. The payout will help her run her home when she is retired and ensure she does not need to ask anyone for financial support.

Scenario 3 – Claire is in her early 20s and has just started working. She took a term plan for a period of 10 years as the premiums were affordable and she wanted to bring herself under the protection of life insurance. Claire also harbours dreams of going abroad later and settling down. Once her term plan ends, she might want to consider opting for whole life insurance. A whole life insurance plan will offer Claire cash value if she has to surrender it when she leaves the country. Moreover, a whole life insurance plan will cost her a lot less when she is young and will be easier to pay for before she starts a family.

In conclusion… As we can see, term insurance and whole life insurance each have their own unique benefits to offer. The choice you make really depends on your unique need and expectations from life insurance. If you need a bit of help in making the right decision, you can reach out to a professional financial consultant. All the best!