Download

1 / 42

430 likes | 626 Views

Topic 3: Demand, Supply, & Pricing. Buyers demand goods, sellers supply those goods, and the interactions between the two groups lead to an agreement on the price and the quantity traded. Warm-Up: What is your most important consideration when you consider buying something?

E N D

Topic 3: Demand, Supply, & Pricing Buyers demand goods, sellers supply those goods, and the interactions between the two groups lead to an agreement on the price and the quantity traded. Warm-Up: What is your most important consideration when you consider buying something? What are five things that you couldn’t live without? Would you still buy these items if they doubles or tripled in price?

Rules To Remember • DWAP: desire, willingness, ability to purchase • Demand dips • Law of Demandinverse Price(P) & Quantity(Q) • Demand = Quantity Demanded (D = Qd) • Price only changes quantity demanded • 5 shift factors of the demand curve that are not related to price

Law of Demand • The law of demand holds that other things equal, as the price of a good or service rises, its quantity demanded falls. • Inverse relationship: as the price of a good or service falls, its quantity demanded increases. • Demand is important because it shows how people are willing to allocate resources

Example Pizza: • If a slice of pizza costs $1, would you buy it? • How many slices would you buy? • If a slice of pizza cost $3, would you buy it? • How many slices would you now buy? • This shows us the law of demand…as price increases you will buy less

Demand Schedule: • A demand schedule is a table that lists the quantity of a good that an individual in a market will buy at each different price. • A market demand scheduleis a table that lists the quantity of a good all consumers in a market will buy at each different price.

Demand Curve • Shows how much consumers will demand at given prices in graph form

Change in quantity demanded (Qd) • refers to movement along the curve; a change in quantity based on price

Consider This: • What might happen to sales of a particular type of car if its producer announced that its new engine emitted no pollution, was more powerful than previous engines, had better gas mileage than ALL other vehicles, and would cost the same?

Shifts in Demand • A willingness to buy different amounts at the same prices

Shift in the Quantity DemandedA willingness to buy different amounts at the same prices • The following five things cause a shift in the demand curve (SPITE): • Substitution:complimentary goods used to replace or with a good or service • Population:population increases, demand tends to increase • Income:more $, more willing to pay more or buy more quantity • Tastes & Preferences: trends, values/ beliefs • Expectations:what they expect

How the Demand Curve Changes • When we have an INCREASE in demand the curve will shift to the RIGHT because at the SAME price we are demanding more • When we have a DECREASE in demand the curve will shift to the left because at the SAME price we are demanded less

Demand Elasticity Warm-Up: • Give 3 examples of goods that can affect demand for another good because of price change.

Demand Elasticity • Small change in price = great (large) change in quantity demanded • The extent in which changes in price cause changes in the quantity demanded • It is the way consumers respond to price changes • Elasticity of a good varies at every price level

Consider This: • What is essential to me? • What goods must I have even if the price rises greatly?

Elastic Demand • Consumers care about changes in the price of products with elastic demand • Example: • The current price of a donut is $.75. Dunkin Donuts hold a promotion for their coffee, and in the meantime lower the price of a donut to $.50. • What is the effect on quantity demanded? • How is this related to elasticity?

Determinants of Demand Elasticity • Urgency of need (Necessity v. Luxury) • if it is not a necessity it is elastic • if it is a need, it is inelastic • Relative Importance • Ex. Clothing: if you currently spend ½ of your budget on clothing, an increase in the cost of clothing will cause a large reduction in the quantity you purchase.- Elastic • Ex. Shoelaces: if the price doubled, would you cut back? Probably not because you may not even notice the difference b/c it is only a small part of your budget-Inelastic

Determinants of Demand Elasticity (Continued) • Substitution availability • If substitutions are available- elastic • Ex. Butter/ margarine • Change over time • Can’t react quickly to price increase so it takes time to find substitutes; so demand is inelastic for a short time until they find substitutes • Income portion to buy • If goods/services are expensive-elastic

Inelastic Demand • A small change in price causes a very little change in quantity demanded • A demand for a good you keep buying despite a price increase • Examples: • Gas • Milk at the grocery store costs $3.79 per gallon. Price Chopper has a weekly sale and lowers the price to $3.39 per gallon. • What is the effect on quantity demanded? • How is this related to inelasticity?

Supply Warm-Up:

Rules of Supply (Producer) • S = Supply (Think about what’s already on the store shelves available for purchase and not what the manufacturing potential is). • Supply to the sky (Curve) • Law of Supply- direct relationship (P Q ) • Price = change in Quantity Supplied • 8 factors that shift supply

Law of Supply • holds that other things equal, as the price of a good rises, its quantity supplied will rise, and vice versa. P Q OR P Q Direct Relationship • Producers produce more output when prices rise so they can cover higher marginal costs of production

What is a Supply Schedule? • Shows the relationship between price & quantity supplied

What is a Supply Curve? • A graphical representation of the supply schedule • Horizontal axis measures the quantity of good supplied • Producer's supply curve shows the quantity of an item that producers will supply for given prices.

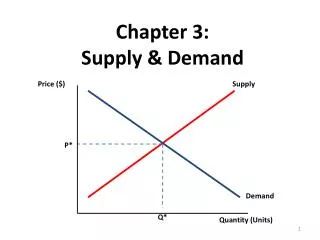

Equilibrium • In economics, an equilibrium is a situation in which: • there is no inherent tendency to change, • quantity demanded equals quantity supplied Equilibrium occurs at a price of $3 and a quantity of 30 units.

Shifts in Supply • A change in any variable other than price that influences quantity supplied produces a shift in the supply curve or a change in supply (GETSTIPS). • Government Regulation • Expectations • Technology • Subsidies • Taxes • Input (Cost Of) • Productivity • Sellers (number of)

Elasticity of Supply • Measure of the way suppliers respond to a change in price • If supply is ELASTIC it means that changes in price will have a large impact on Quantity supplied • If supply is INELASTIC, it means price does little to change Quantity Supplied

Time In the long run, firms are more flexible, so supply can become more elastic. What Affects Elasticity of Supply? • In the short run, a firm cannot easily change its output level, so supply is inelastic.

Supply Elasticity vs. Demand Elasticity • If quantities are being purchased, the concept is demand elasticity • If quantities are being sold, concept is supply inelasticity

Government Influences on Supply Subsidies A subsidy is a government payment that supports a business or market. Subsidies cause the supply of a good to increase. Taxes The government can reduce the supply of some goods by placing an excise tax on them. An excise tax is a tax on the production or sale of a good. Regulation Regulation occurs when the government steps into a market to affect the price, quantity, or quality of a good. Regulation usually raises costs.

Costs Total Cost Variable Costs Fixed Costs Sum of fixed & Variable costs Costs that don’t change with output Costs that change with Output Ex. Wage workers, Raw materials, electricity

Definitions Marginal Costs: • Costs incurred by making one more unit Marginal Product: • Extra output made by adding one more unit of input Theory of Production: • Deals w/ relationship between Factors of Production and output; it looks at how output changes when input changes Law of Variable Proportions: • output will change as one input is changed

Pricing As Signals: The role of prices is to act as signals for buyers and sellers in the market. Advantages of Prices: • Standard form of measure for g/s Measure of Value • for excess or shortage: suppliers inc/dec production for profit; consumers inc/dec spending Signal • can decrease price to get rid of a surplus • Can increase price to alleviate shortage problem Flexible • no administrative cost b/c supply and demand determine price Cost • variety of prices for each g/s Choice of g/s • FOPS adjust based on demand • Easily understood (universal language) Efficient

Allocation without Prices: • Rationing: • Government decides everyone’s fair share • Ex. WWII/ OPEC 1973 Oil Embargo • Problems with Rationing • Fairness: small shares for everyone • Diminished incentives: no motivation to work • Can lead to BLACK MARKET

How Prices are Determined? • The Economic Model • Analyzes behaviors • Predicts outcomes • When Quantity Demanded = Quantity Supplied, we have a market equilibrium

Surplus • When Qs>Qd • Effects: • cause Price to decrease • Qd to increase • Qs to decrease

Shortage Shortage • Qs < Qd EFFECTS of a Shortage (how to return to Eq): • Increase price • Quantity Supplied increase

What happens when prices are fixed? • Price Ceilings • Maximum legal price charged b/c the gov’t thinks price is too high • Effect: SHORTAGE • Example: rent control • Price Floors • Minimum legal price charged b/c the gov’t thinks it is too low • Effect: SURPLUS • Example: minimum wage

$2.00 Price Ceiling $1.00 $.50

$2.00 $1.00 Price Floor $.50