Download

1 / 17

170 likes | 266 Views

John B. Taylor Under Secretary for International Affairs United States Treasury Central Bank of Peru Lima, Peru September 6, 2004. Challenges and Successes in Treasury Engagement on Monetary Policy. Iraqi Monetary Policy. Iraq faced variety of monetary problems at end of war:

E N D

John B. Taylor Under Secretary for International Affairs United States Treasury Central Bank of Peru Lima, Peru September 6, 2004 Challenges and Successes in Treasury Engagement on Monetary Policy

Iraqi Monetary Policy Iraq faced variety of monetary problems at end of war: • Legacy of monetary policy mismanagement and inflation • Lack of central bank independence • Lack of unified, stable currency: • 2 currencies in circulation, with limited denominations • Absence of security features on “Saddam” dinar • Sharp depreciation of “Saddam” dinar relative to “Swiss” dinar

Monetary Policy Achievements Post-War: • Established independent central bank • Conducted currency exchange: • Ran from October 15, 2003 to January 15, 2004 • Introduced new currency with 6 denominations, based on designs from old Iraqi dinars • Exchange went remarkably well • Value appreciated about 25% • Provided technical assistance to: • Develop daily currency auction • Establish new central bank law • Create monetary framework • Introduce new monetary instruments • Produce necessary monetary data

Afghanistan Initial Currencies: • Official Afghani • Duplicate Afghanis from Government in Exile • Warlord-Issued Counterfeits • Foreign Currencies

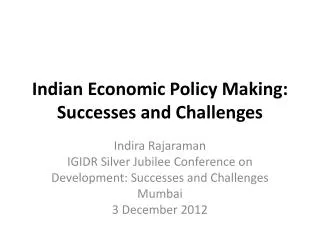

Finance Minister Ashraf Ghani, Treasury President Ehsan Assadi, U/S Taylor and Amb. Paul Speltz. Explaining existing manual payroll procedures at the Finance Ministry.

Monetary Policy Issues • Choice of Currency • Objective – Price Stability • Exchange Rate Regime • Monetary Target

Argentina: Quasi-Currencies • Origins • Fiscal constraints = resort to creative financing • 12 of 24 provinces issued own currencies; federal government issued its own quasi-currency (lecop) • At peak, quasi-currencies were 1/2 of all currency in circulation and 1/3 of monetary base • Consequences • Central bank loses ability to control entire monetary supply • Demand for official currency that central bank does control because unpredictable. Interest rates and exchange rates become unpredictable. • Fragmentation of monetary space = fragmentation of market for goods/ services. Fluctuating internal ex-rates. No reliable medium of exchange • Difficulty in launching IMF program as difficult to predict money demand and set monetary targets • Solving the Problem • IMF transitional program launched in January 2003 • Argentine government initiates buyback that virtually eliminate quasi-currency stock by end-2003 • 2003 inflation is 4% vs. 2002 inflation of 42%

Uruguay: Run on Dollar Deposits • Context • 90% dollarized financial system • History of macro stability, offshore banking sector • Crisis • Inflows of deposits from Argentina. Inadequate reserve backing • Withdrawals by Argentine depositors after imposition of deposit freeze in Argentina. Spread to non-residents, given concerns about inadequate dollar reserves & questions about government fiscal sustainability • Policy Response • IMF loans to build reserves in spring/early summer insufficient to stop run • Mobilization of IMF/WB/IDB money to provide full backing for certain categories of deposits. USG short-term bridge loan to re-open banks. • Results • Guarantee stopped run and prevented collapse of payment system • Fiscal measures restored confidence in government finances • Return to robust economic growth