Download

1 / 10

100 likes | 253 Views

Cost Merchandise Inventory. Chapter #8 8.1 & 8.4. Introduction. Merchandise= Current Asset Merchandise is what you plan to be selling there for it can be converted into cash today.

E N D

Cost Merchandise Inventory Chapter #8 8.1 & 8.4

Introduction • Merchandise= Current Asset • Merchandise is what you plan to be selling there for it can be converted into cash today. • In manufacturing you have raw materials and goods in process in addition the inventory of finished goods. • We will continue with merchandise as it relates to what we learned in Chapter 7.

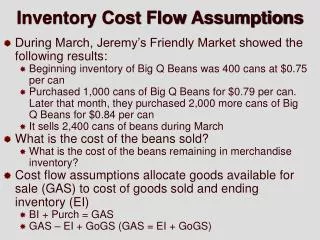

Inventory Measurement • Three Methods approved by GAAP (General Accepted Accounting Principles) • FIFO: First-In-First Out • LIFO: Last-In-First Out • Weighted Average

First-In-First-Out • When you use this method you are assuming that the goods are sold in the order in which they are purchased. • For example at a Grocery store the hope is that you sell off the older inventory and replace it with newer inventory as it comes in. • Most widely used inventory method of the ones we will learn.

Last-In-First-Out • When using this method you are assuming that the most recently purchased items are to be first ones sold and the remaining inventory would be the earliest items purchased. • Reduces income tax in times of inflation.

Weighted Average • Also know as Average Cost Valuation • This method is based on the average cost of inventory. • It spreads to cost of goods available for sale equally among all the units.

In Class End Inventory for FIFO End Inventory for LIFO End Inventory for Weighted Average. Work on this for the remained of class. I am available for any questions. I will pass out the homework which is due at the beginning of class tomorrow.