Download

1 / 53

550 likes | 849 Views

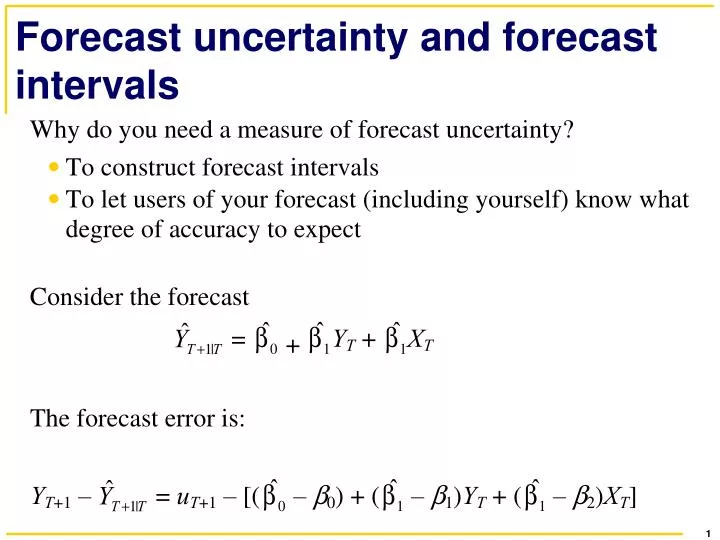

Forecast uncertainty and forecast intervals . Mean Squared Forecast Error. Three ways to estimate the RMSFE . Pseudo out-of-sample forecasting. Constructing forecast intervals . Example #1: the Bank of England “ Fan Chart ” , 11/05 .

E N D

Example #2: Monthly Bulletin of the European Central Bank, Dec. 2005, Staff macroeconomic projections

Log Japan gdp (smooth line) and US inflation (both rescaled), 1965-1981

Log Japan gdp (smooth line) and US inflation (both rescaled), 1982-1999

Nonstationarity from breaks (changes) in regression coefficients

The Quandt Likelihod Ratio (QLR) Statistic (also called the “sup-Wald” statistic)

Assessing Model Stability using Pseudo Out-of-Sample Forecasts