Download

1 / 22

220 likes | 360 Views

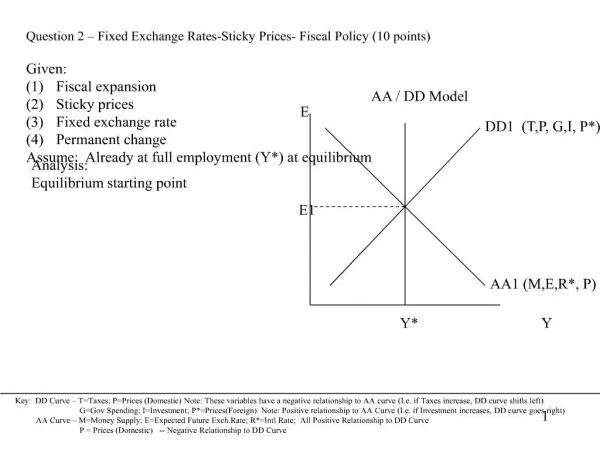

THE SEASONALITY IN THE ITALIAN TOURISM SECTOR. www.reag-aa.com. The Italian tourism sector: some ways to correct seasonal adjustment. Elena Zanlorenzi, Head of Research European R&D Office REAG 23-26.06.2010 Milan, Italy. INDEX. 1. SEASONAL ADJUSTMENT.

E N D

THE SEASONALITY IN THE ITALIAN TOURISM SECTOR www.reag-aa.com

The Italian tourism sector: some ways to correct seasonal adjustment Elena Zanlorenzi, Head of Research European R&D Office REAG 23-26.06.2010 Milan, Italy

INDEX 1. SEASONAL ADJUSTMENT 2. THE ITALIAN TOURISM SECTOR 3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT 4. CONCLUSIONS

1. SEASONAL ADJUSTMENT Tourism seasonality = monthly fluctuation of the number of tourist nights • Tourism is a seasonal phenomenon: • natural causes: climatic seasons • institutional causes: school holidays, time off • social causes: public or religious holidays • Tourism seasonality affects the entire tourism industry: • tour operators • travel agencies • hotels • transports • Seasonality losses: • additional costs for the PA (ex. parking) • greater incidence of the fixed costs in the hotels turnover • decrease of the revenues • growth of the average room rate • tourist overcrowding in the high season • temporary employment

1. SEASONAL ADJUSTMENT The Italian tourist sector is historically affected by seasonal criticalities • in many locations the tourist season lasts only for 4-5 months per year • for the remaining 7-8 months hotels and leisure activities are forced to close • in these months of low season expenses could be higher than revenues • Italian seaside tourist areas are the most affected by seasonal adjustments • even for this reason return on investment could not be so attractive for the main international brands • during the last years some operators tried to get round this matter diversifying the offer: SPA, • wellness centres, business centres, etc. • these are only local and segmented operation that do not lead to a resolution of the problem • Some evidences about seasonality: • the balanced use of touristic structures does not exclude monthly fluctuations but these are of low intensity • different tourism typologies present different seasonality • cultural tourism is the less affected by seasonality • seaside tourism is typically affected by seasonality (summer) • mountain tourism could have 2 seasons (summer and winter) • wellness tourism could last for 4 seasons • business tourism is affected by seasonality during holidays

2. THE ITALIAN TOURISM SECTOR The tourism economic impact • tourism contributes to GDP for 9,6% • tourism contribute is equal to 152 billion of euro • direct tourism industry contributes to GDP for 3,9% • total overnight stays: 860 mln (of which 358 mln in hotel and extra-hotel accommodation) • total Italian overnight stays: 546 mln (of which 204 mln in hotel and extra-hotel accommodation) • tourists expenditure: 75.862 mln of euro (of which 49.495 mln in hotel and extra-hotel accommodation) • Italian tourists expenditure: 44.049 mln of euro (of which 24.900 mln in hotel and extra-hotel accommodation) TOURISTS EXPENDITURE BY TYPOLOGY (2009) Source: Reag work-out on OsservatorioNazionale del Turismo data

2. THE ITALIAN TOURISM SECTOR OVERNIGHT STAYS BY DESTINATION (% - 2009) Source: Reag work-out on OsservatorioNazionale del Turismo data (2009) TOURISTS EXPENDITURE BY DESTINATION (% - 2009) Source: Reag work-out on OsservatorioNazionale del Turismo data

2. THE ITALIAN TOURISM SECTOR HOTELS TURNOVER Source: Reag work-out on AICA data HOTELS TURNOVER BY ROOM Source: Reag work-out on AICA data

2. THE ITALIAN TOURISM SECTOR ROOM OCCUPATION RATE (% - 2009) Source: Reag work-out on AICA data AVERAGE REVENUE PER AVAILABLE ROOM (% - 2009) Source: Reag work-out on AICA data

2. THE ITALIAN TOURISM SECTOR ITALIANS OVERNIGHT STAYS (%) Source: Reag work-out on different sources FOREIGNERS OVERNIGHT STAYS (%) Source: Reag work-out on different sources

2. THE ITALIAN TOURISM SECTOR OVERNIGHT STAYS IN CULTURAL DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data OVERNIGHT STAYS IN SEASIDE DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data

2. THE ITALIAN TOURISM SECTOR OVERNIGHT STAYS IN MOUNTAIN DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data OVERNIGHT STAYS IN NATURALISTIC DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data

2. THE ITALIAN TOURISM SECTOR OVERNIGHT STAYS IN LAKE DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data OVERNIGHT STAYS IN SPA DESTINATIONS (% - 2007) Source: Reag work-out on OsservatorioNazionale del Turismo data

2. THE ITALIAN TOURISM SECTOR Seasonality indexes • seasonality rate: maximum overnight stays (Smax)/minimum overnight stays (Smin) • seasonal peak factor (S’): Smax/average overnight stays (Sm) • maximal utilization constrained by seasonality (MUS): 100/S’ • seasonality underutilization factor (SUF): 100 - MUS

3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT During the last years some operators tried to get round this matter diversifying the offer • Some structures provide their clients with : • SPA • wellness center • business center • golf • etc. Thesedevices are onlylocal and segmentedoperationthat do notlead to a resolutionof the problem Identify some categoriestillnowignoredby the tourismsector: could the investment in thesegroupsof people help the renewalof the sector?

3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT Children (< 6 years old) tourism CHILDREN OVERNIGHT STAYS (%) Source: Reag work-out on various sources • number: 3.400.719 (2019: 3.255.338; -4,3%) • household income: € 35.432 (+20,9% respect • Italian average income) • the 31% of the households falls within the 2 • classes with the higher income • tourism propensity: 34,3% • % on total overnight stays: 4,1% • overnight stays: 6,7 mln • potential demand: 12,9 mln of overnight stays • potential demand: 7,9% on total overnight stays • increase in tourism expenditure: +12,0% (direct • 2,2 bln of euro; indirect 3,6 bln of euro) • seasonality rate: 4,0 (before 4,3) • seasonal peak factor: 2,0 (before 2,1) • MUS: 49,5 (before 48,0) • SUF: 50,5 (before 52,0) OVERNIGHT STAYS (%) Source: Reag work-out on various sources

3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT Elderly people (> 65 years old) tourism ELDERLY PEOPLE OVERNIGHT STAYS (%) Source: Reag work-out on various sources • number: 11.457.143 (2019: 13.184.101; +15,1%) • household income: € 21.117 (-27,9% respect • Italian average income) • the 31% of the households falls within the 2 • classes with the higher income • tourism propensity: 13,5% • % on total overnight stays: 5,5% • overnight stays: 8,9 mln • potential demand: 57,3 mln of overnight stays • potential demand: 35,1% on total overnight stays • increase in tourism expenditure: +53,0% (direct • 9,9 bln of euro; indirect 16,0 bln of euro) • seasonality rate: 3,3 (before 4,3) • seasonal peak factor: 1,9 (before 2,1) • MUS: 52,8 (before 48,0) • SUF: 47,2 (before 52,0) OVERNIGHT STAYS (%) Source: Reag work-out on various sources

3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT Singles tourism SINGLES OVERNIGHT STAYS (%) Source: Reag work-out on various sources • number: 6.910.716 (2019: 8.389.609; +21,4%) • household income: € 17.546 (-40,1% respect • Italian average income) • the 48% of the households falls within the 2 • classes with the higher income • tourism propensity: 35,0% • % on total overnight stays: 8,6% • overnight stays: 14,0 mln • potential demand: 26,0 mln of overnight stays • potential demand: 15,9% on total overnight stays • increase in tourism expenditure: +24,2% (direct • 4,5 bln of euro; indirect 7,3 bln of euro) • seasonality rate: 3,7 (before 4,3) • seasonal peak factor: 2,0 (before 2,1) • MUS: 50,8 (before 48,0) • SUF: 49,2 (before 52,0) OVERNIGHT STAYS (%) Source: Reag work-out on various sources

3. SOME WAYS TO CORRECT SEASONAL ADJUSTMENT Groups tourism GROUPS OVERNIGHT STAYS (%) Source: Reag work-out on various sources • household income: € 29.308 • the 40% of the households falls within the 2 • classes with the higher income • % on total overnight stays: 5,2% • overnight stays: 8,5 mln • potential demand: 6,2 mln of overnight stays • potential demand: 3,8% on total overnight stays • increase in tourism expenditure: +5,8% (direct • 1,1 bln of euro; indirect 1,7 bln of euro) • seasonality rate: 4,1 (before 4,3) • seasonal peak factor: 2,0 (before 2,1) • MUS: 50,8 (before 48,8) • SUF: 51,2 (before 52,0) OVERNIGHT STAYS (%) Source: Reag work-out on various sources

THANK YOU FOR YOUR ATTENTION! for any other info, please contact rdo@reag-aa.com No part of this presentation may be reproduced or trasmitted in any form or by any means, whitout written permission of REAG (Real Estate Advisory Group S.p.A.). For any information please contact: marketing@reag-aa.com