Download

1 / 17

170 likes | 398 Views

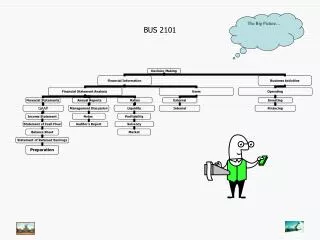

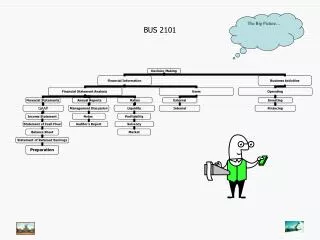

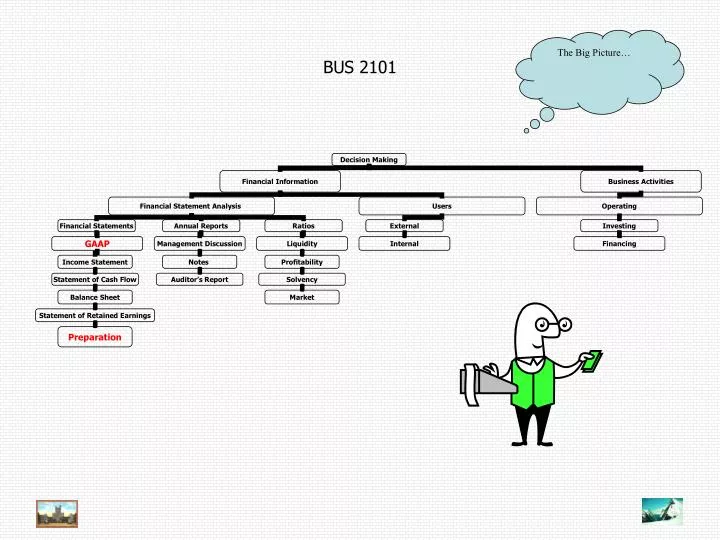

BUS 2101. The Big Picture…. Accrual Accounting Concepts. Cash basis accounting Accrual basis accounting Matching principle Adjusting entries Prepayments Accruals Adjusted trial balance Closing entries Accounting cycle. Cash basis accounting. Revenue recorded when cash is received

E N D

BUS 2101 The Big Picture…

Accrual Accounting Concepts • Cash basis accounting • Accrual basis accounting • Matching principle • Adjusting entries • Prepayments • Accruals • Adjusted trial balance • Closing entries • Accounting cycle

Cash basis accounting • Revenue recorded when cash is received • No revenue if customer doesn’t pay at time of transaction • Expenses recorded when they are paid • No expense unless payment made in period • Advantage • Simple • Disadvantage • Useful information??? • Often used by small businesses • Used by individuals for income tax purposes

Accrual basis accounting • Revenue recognition principle: Revenue is recorded when service is performed or goods are delivered • May not be in the same period cash is received • Matching principle: Expenses are recorded in the period they help generate revenue • May not be in the same period payment is made • Adjusting entries: Needed based on revenue recognition and matching principles

Adjusting entries • Prepayments • Prepaid expenses • Purchased supplies on 1/10/10 of $680 • As of 1/31/10, only $100 of supplies in closet

Adjusting entries • Prepayments • Prepaid expenses • Paid $4,800 for 2010 insurance policy on 1/5/10 • As of 1/31/10, used one month of insurance coverage

Adjusting entries • Prepayments • Depreciation • Paid $480,000 on 1/2/10 for building expected to last 20 years • $480,000 / 20 years = $24,000 depreciation expense • As of 1/31/10, need to record one month’s depreciation expense

Adjusting entries • Unearned revenue • Received $600 on 1/2/10 to fly customer to L.A. on 2/16/10 • As of 2/16/10, need to record revenue

Adjusting entries • Accrued revenue: revenue earned but no cash received • On 2/12/10, performed surgery on patient. Sent patient bill for $73 on 2/17/10. • As of 2/28/10 no payment has been received

Adjusting entries • Accrued expenses: expense incurred but not paid • On 1/01/10, borrowed $100,000 at 6%. Interest is payable on 2/1/10. • As of 1/31/10, no interest has been paid

Adjusting entries • Never an entry to cash • Either • Dr. Expense or • Cr. Revenue • Other side of entry is to an asset or liability account

Adjusted Trial Balance • See page 177

Closing Entries • Must reset income and expenses to zero before next accounting period • Income summary is the basket used to do this

Closing Entries • Debit Revenue, dump into Income Summary (Credit) • Revenue • Income Summary • Credit Expenses, dump into Income Summary (Debit) • Income Summary • Expenses

Closing Entries • Dump Net Income into Retained Earnings • Income Summary (if revenue > expenses) • Retained earnings • Dump Dividends into Retained Earnings • Retained Earnings • Dividends

BUS 2101 The Big Picture…