Download

1 / 56

560 likes | 710 Views

The Master Budget and Responsibility Accounting. Chapter 23. Identify the benefits of budgeting. Objective 1. Benefits of Budgeting. requires managers to plan. promotes coordination and communication. helps managers evaluate performance. motivates employees to achieve company goals.

E N D

Identify the benefits of budgeting. Objective 1

Benefits of Budgeting requires managers to plan promotes coordination and communication helps managers evaluate performance motivates employees to achieve company goals

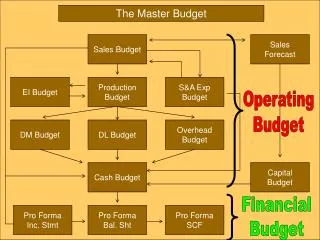

Components of the Master Budget Inventory Budget ____ ____ ____ ____ ____ ____ ____ ____ ____ ____ Sales Budget ____ ____ ____ ____ ____ ____ ____ ____ ____ ____ Purchases Budget ____ ____ ____ ____ ____ ____ ____ ____ ____ ____ Cost of Goods Sold Budget ____ ____ ____ ____ ____ ____ ____ ____ Operating Expenses Budget ____ ____ ____ ____ ____ ____ ____ ____ Budgeted Income Statement ____ ____ ____ ____ ____ ____ ____ ____ Operating Budget

Components of the Master Budget Cash Budget _____ _____ _____ _____ _____ _____ _____ _____ _____ _____ Budgeted Income Statement _____ _____ _____ _____ _____ _____ _____ _____ _____ _____ Capital Expenditures Budget _____ _____ _____ _____ _____ _____ _____ _____ _____ _____ Financial Budget Budgeted Statement of Cash Flows _____ _____ _____ _____ _____ _____ _____ _____ _____ _____ Budgeted Balance Sheet _____ _____ _____ _____ _____ _____ _____ _____ _____ _____

Preparing the Master Budget • Suppose that J.J. manages Plantation Sporting Store No. 13. • Selected parts of the master budget will be prepared for Store No. 13 for April, May, June, and July.

Preparing the Master Budget • Sales are 60% cash and 40% on credit. • Credit sales are collected in the month following the sale. • Accounts receivable on March 31 amounted to $19,200. • How much were total sales in March? • $19,200 ÷ .40 = $48,000

Preparing the Master Budget Projected Sales April …………… $50,000 May …………… $80,000 June …………… $60,000 July …………… $50,000

Preparing the Master Budget • Plantation maintains inventory equal to $10,000 plus 40% of the budgeted cost of goods sold for the following month. • Cost of goods sold averages 70% of sales. • Target ending inventory on July 31 is $32,000.

Preparing the Master Budget • What is the ending inventory on March 31? • $10,000 + (0.40 × 0.70 × April sales of $50,000) • What is the beginning inventory? • $10,000 + (0.40 × 0.70 × $48,000) = $23,440

Preparing the Master Budget • Plantation pays for inventory as follows: 50% during the month of purchase and 50% during the next month. • March purchases were $34,160. • How much was paid in March for March’s purchases? • $34,160 × 50% = $17,080

Prepare an operating budget. Objective 2

Sales Budget (Schedule A) • Sales revenue is the key measure of business activity. • The budgeted total sales revenue for each product is the sales price multiplied by the expected number of units sold.

AprilMayJuneJuly Cash sales 60% $30,000 $48,000 $36,000 $30,000 Credit sales 40% 20,000 32,000 24,000 20,000 Total $50,000 $80,000 $60,000 $50,000 Total sales April through July = $240,000 Sales Budget (Schedule A)

Purchases, Cost of Goods Sold,and Inventory Budget • Cost of goods sold = 70% × sales • How much are the cost of goods sold for May? • 70% × $80,000 = $56,000 • What is the desired ending inventory for April? • $10,000 + (40% × $56,000) = $32,400

Purchases, Cost of Goods Sold,and Inventory Budget Beginning inventory + Purchases – Ending inventory = Cost of goods sold Cost of goods sold + Ending inventory – Beginning inventory = Purchases

AprilMayJuneJuly Cost of goods sold (70% × sales) $35,000 $56,000 $42,000 $35,000 Desired ending inventory 32,400 26,800 24,000 32,000 Total required $67,400 $82,800 $66,000 $67,000 Beginning inventory 24,000 32,400 26,800 24,000 Purchases $43,400 $50,400 $39,200 $43,000 Schedule B

Schedule B How much is the cost of goods sold for the four-month period? April……………… $ 35,000 May………………. 56,000 June………………. 42,000 July………………. 35,000 Total $168,000

Operating Expenses Budget • Assume that Plantation Sporting Goods incurs $4,000 of fixed expenses every month and that commissions and other variable expenses equal 20% of sales. • What is the operating expenses budget (Schedule C)?

AprilMayJuneJuly Variable expenses (From Schedule A) 20% of sales $10,000 $16,000 $12,000 $10,000 Fixed expenses 4,000 4,000 4,000 4,000 Total $14,000 $20,000 $16,000 $14,000 Operating Expenses Budget(Schedule C) Total operating expenses: $64,000

Budgeted Income Statement Plantation Sporting Goods Store No. 13 Budgeted Income Statement Four Months Ending July 31, 20xx AmountSource Sales $240,000 Schedule A Cost of goods sold 168,000 Schedule B Gross margin $ 72,000 Operating expense 64,000 Schedule C Net income $ 8,000

Prepare the components of a financial budget. Objective 3

Preparing the Financial Budget • The financial budget includes: Cash budget Budgeted balance sheet

Preparing the Cash Budget • The cash budget has the following major parts: • cash collections from customers (Schedule D) • cash disbursements for purchases (Schedule E) • cash disbursements for operating expenses (Schedule F) • capital expenditures (not illustrated in this chapter)

Cash Collections from Customers (Schedule D) From Schedule A AprilMayJuneJuly Cash sales $30,000 $48,000 $36,000 $30,000 Collections of last month’s credit sales 19,200* 20,000 32,000 24,000 Total $49,200 $68,000 $68,000 $54,000 Total collections: $239,200 *19,200 = March 31 accounts receivable

Cash Disbursements for Purchases (Schedule E) From Schedule B AprilMayJuneJuly Payment of last month’s purchases $17,080 $21,700 $25,400 $19,600 Payment of this month’s purchases 21,700 25,200 19,600 21,500 Total $38,780 $46,900 $45,000 $41,100 Total disbursements: $171,780

Cash Disbursements for Operating Expenses (Schedule F) From Schedule C AprilMayJuneJuly Payment of last month’s expenses $ 6,800 $ 7,000 $10,000 $ 8,000 Payment of this month’s expenses 7,000 10,000 8,000 7,000 Total $13,800 $17,000 $18,000 $15,000 Total disbursements: $63,800

Cash Budget Plantation Sporting Goods Store No. 13 Cash Budget Four Months Ending July 31, 20xx Budgeted cash receipts $239,200 Budgeted cash disbursements Purchases $171,780 Operating expenses 63,800 235,580 Budgeted cash increase $ 3,620

Preparing the Budgeted Balance Sheet • Assets, liabilities, and owners’ equity are projected based upon the previous schedules. • Assume that the cash balance on March 31 was $15,000. • What is the budgeted cash balance on July 31? • $15,000 + $3,620 expected increase = $18,620

Use sensitivity analysis in budgeting. Objective 4

Budgeting and Sensitivity Analysis • Sensitivity analysis helps managers plan for different courses of action. • This type of “what if” analysis shows the result of changing an underlying assumption in the budgeting process. • Sensitivity analysis may affect very specific plans.

Distinguish among different types of responsibility centers. Objective 5

Responsibility Accounting... • is a system for evaluating the performance of managers and the activities they supervise. • A responsibility center is a part, segment, or subunit of an organization whose manager is accountable for specific activities.

Responsibility Center Cost center Revenue center Profit center Investment center

Prepare a performance report for management by exception. Objective 6

Management by Exception Northern California District Manager San Francisco Branch Manager San Jose Branch Manager Oakland Branch Manager Sacramento Branch Manager Geary Store Manager Beale Store Manager Wharf Store Manager Other Managers

Management by Exception • Performance reports show differences between budgeted and actual amounts. • Management by exception is the practice of focusing on important variances so that managers can direct their attention to areas that need improvement.

Management by Exception Plantation Sporting Goods Store No. 13 Monthly Responsibility Report (Budget) MonthYTD Revenues $50,000 $388,000 Cost of goods sold 35,000 271,600 Wages 6,700 51,992 Repairs 2,000 15,520 General 1,300 10,088 Fixed costs 4,000 28,000 Operating income $ 1,000 $ 10,800

Management by Exception Plantation Sporting Goods Store No. 13 Monthly Responsibility Report (Actual) MonthYTD Revenues $55,000 $408,000 Cost of goods sold 37,400 277,440 Wages 7,370 54,672 Repairs 550 8,160 General 900 8,160 Fixed costs 4,000 28,000 Operating income $ 4,780 $ 31,568

Management by Exception Plantation Sporting Goods Store No. 13 July 20xx, Responsibility Report BudgetActualVariance (F/U) Revenues $50,000 $55,000 $5,000 (F) Cost of goods sold 35,000 37,400 2,400 (U) Wages 6,700 7,370 670 (U) Repairs 2,000 550 1,450 (F) General 1,300 900 400 (F) Fixed costs 4,000 4,000 --- Operating income $ 1,000 $ 4,780 $3,780 (F)

Management by Exception • J.J., manager of Plantation Sporting Goods Store No. 13, will investigate why cost of goods sold and wages were more than budgeted. • Cost of goods sold was originally budgeted to be 70% of sales. • Wages was budgeted to be 67% of total operating variable expenses or 13.4% of sales.

Management by Exception • Management will determine that cost of goods sold were 68% of sales instead of the 70% originally budgeted. • $37,400 ÷ $55,000 = 68% • Pleasant news!

Management by Exception • Management may investigate why wages were 84% of total variable operating expenses instead of the 67% originally budgeted, although in total they remained 13.4% of sales. • $7,370 ÷ $8,820 = 84% • It will be determined that other variable operating expenses were less than anticipated.

Management by Exception Broward County Branch Manager Plantation Sporting Stores July 20xx, Responsibility Report BudgetActualVariance (F/U) Branch manager office expense $20,000 $25,000 $ 5,000 (U) Income: Store 13 1,000 4,780 3,780 (F) Others 80,000 95,220 15,220 (F) Operating income $61,000 $75,000 $14,000 (F)

Management by Exception South Florida District Manager Plantation Sporting Stores July 20xx, Responsibility Report BudgetActualVariance (F/U) District manager office expense $ 95,000 $ 99,000 $ 4,000 (U) Income: Broward county 61,000 75,000 14,000 (F) Other counties 280,000 325,000 45,000 (F) Operating income $246,000 $301,000 $55,000 (F)

Allocate indirect costs to departments. Objective 7

Allocation of Indirect Costs • Indirect costs are allocated to departments or responsibility centers using the following steps: • Choose an allocation base for the indirect cost. • Compute an indirect cost allocation rate. • Allocate the indirect cost.

Choose an Allocation Base Cost or ExpenseBasis Indirect labor Time spent Building depreciation Square feet Heat, lights, etc. Square feet Janitorial services Square feet Payroll and personnel # of employees Purchasing # of purchase orders placed

Choose an Allocation Base • Lets consider the Healthy Clinic, a provider of Ear, Nose, and Throat (ENT) plus Audiology services. • Rent for the year is $120,000. • Total square footage occupied by the clinic is 12,000. • What is the rent per square foot? • $120,000 ÷ 12,000 = $10

Compute a Cost Allocation Rate • Other expenses amounted to $100,000 and are allocated on the basis of professional services expenses. • Total professional services expenses amounted to $250,000. • ENT accounted for $175,000 of these expenses and Audiology for $75,000.