Download

1 / 13

130 likes | 212 Views

MONEY MARKET ORGANIZATIONS, INSTRUMENTS, FUNCTIONING & ITS REGULATIONS. CA PRATAP VISHNOI. MONEY MARKET :.

E N D

MONEY MARKET ORGANIZATIONS, INSTRUMENTS, FUNCTIONING & ITS REGULATIONS CA PRATAP VISHNOI

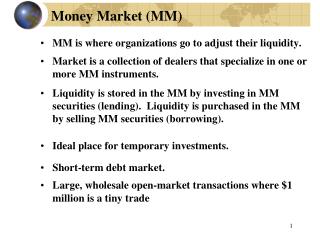

MONEY MARKET: The money market is a key component of the financial system as it is the fulcrum of monetary operations conducted by the central bank in its pursuit of monetary policy objectives. It is a market for short-term funds with maturity ranging from overnight to one year and includes financial instruments that are deemed to be close substitutes of money.

FUNCTIONS OF MONEY MARKET: • It provides an equilibrating mechanism for demand and supply of short-term funds. • It enables borrowers and lenders of short-term funds to fulfill their borrowing and investment requirements at an efficient market clearing price. • It provides an avenue for central bank intervention in influencing both quantum and cost of liquidity in the financial system, thereby transmitting monetary policy impulses to the real economy.

MONATORY POLICY TRANSMISSION THROGH INTEREST RATE CHANNEL Monetary Policy Operations ( Reserve Requirements, Refinance) Change in Reserves Short-term Interest RateMonetary Base Money Supply Market Interest Rate Real Interest Rate Interest Rate Channel Aggregate Demand

PLAYERS • Reserve Bank of India • SBI DFHI Ltd (Amalgamation of Discount & Finance House in India and SBI in 2004) • Acceptance Houses • Commercial Banks, Co-operative Banks and Primary Dealers are allowed to borrow and lend. • Specified All-India Financial Institutions, Mutual Funds, and certain specified entities are allowed to access to Call/Notice money market only as lenders • Individuals, firms, companies, corporate bodies, trusts and institutions can purchase the treasury bills, CPs and CDs.

PRYMARY DEALERS: • The system of Primary Dealers (PDs) in the Government Securities Market was introduced by Reserve Bank of India in 1995 to strengthen the market infrastructure of Government Securities • DFHI was set up by RBI in March 1988 to activate the Money Market. • It got the status of Primary Dealer in February 1996. Over a period of time, RBI divested its stake and DFHI became a subsidiary of State Bank of India (SBI). • SBI had also set up a subsidiary in 1996 for doing PD business namely SBI Gilts Limited. • Both these companies were merged in 2004 to become the largest Primary Dealer in the country • Primary Dealers can also be referred to as Merchant Bankers to Government of India as only they are allowed to underwrite primary issues of government securities other than RBI

CONT….. • PDs are allowed the following activities as core activities:1. Dealing and underwriting in Government securities. 2. Dealing in Interest Rate Derivatives.3. Providing broking services in Government securities.4. Dealing and underwriting in Corporate / PSU / FI bonds/ debentures.5. Lending in Call/ Notice/ Term/ Repo/ CBLO market.6. Investment in Commercial Papers.7. Investment in Certificates of Deposit.8. Investment in debt mutual funds where entire corpus is invested in debt securities.

CALL MONEY MARKET • The call money market is an integral part of the Indian Money Market, where the day-to-day surplus funds (mostly of banks) are traded. The loans are of short-term duration varying from 1 to 14 days. • The money that is lent for one day in this market is known as "Call Money", and if it exceeds one day (but less than 15 days) it is referred to as "Notice Money".

CONT… Banks borrow in this market for the following purpose • To fill the gaps or temporary mismatches in funds • To meet the CRR & SLR mandatory requirements as stipulated by the Central bank • To meet sudden demand for funds arising out of large outflows.

CERTIFICATE OF DEPOSITES: • CDs are negotiable money market instruments and are issued in dematerialized form or a promissory note, for funds deposited at a bank or other eligible financial institution for a specified time period. • They are like bank term deposits accounts. Unlike traditional time deposits these are freely negotiable instruments and are often referred to as Negotiable Certificate of Deposits

ELIGIBILITY FOR ISSUE OF CD: • The tangible net worth of the company, as per the latest audited balance sheet, is not less than Rs. 4 crore; • The working capital (fund-based) limit of the company from the banking system is not less than Rs.4 crore • The borrowable account of the company is classified as a Standard Asset by the financing bank/s. • All eligible participants should obtain the credit rating for issuance of Commercial Paper • The minimum credit rating shall be P-2 of CRISIL or such equivalent rating by other agencies

CONT… • Banks, financial institutions, primary dealers, mutual funds and co-operative banks, who are members of NDS, are allowed to participate in CBLO transactions. Non-NDS members like corporate, co-operative banks, NBFCs, Pension/Provident Funds, Trusts etc. are allowed to participate by obtaining Associate Membership to CBLO Segment.