Download

1 / 16

160 likes | 312 Views

Implications of Exchange Mergers on Post-Trade Infrastructures. Buenos Aires November 2011. Agenda. Trades and post-trade infrastructures Case studies The LSE – Borsa Italiana Merger The MICEX and RTS Merger MILA Conclusions. Trade and Post-trade Infrastructures.

E N D

Implications of Exchange Mergers on Post-Trade Infrastructures Buenos Aires November 2011

Agenda • Trades and post-trade infrastructures • Case studies • The LSE – BorsaItaliana Merger • The MICEX and RTS Merger • MILA • Conclusions

Trade and Post-trade Infrastructures • There is a high level of dependency between the exchanges and the post-trade infrastructure entities: • Financial: • Ownership: Most stock exchanges have some stake in the local infrastructure entities (central counterparties (CCPs), central securities depositories (CSDs), clearinghouses (CHs), etc). In the case of vertical silos, the exchanges and CSDs/CCPs are part of the same group. • Revenues: Income for CSDs, CHs and CCP s can be correlated with trading activity. • Operational: • Stock exchanges maintain a link to the CSDs/CCPs/ CHs to transfer transaction data for clearing and settlement. • In many markets, the exchanges and CSDs share or outsource their data back-up centres and business continuity offices to each other. • System capacity: Increase in trading volumes may impact on the CSD’s and CCP’s system performance.

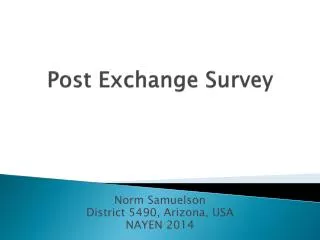

Case Studies LSE – Borsa Italiana

LSE – Borsa Italiana Merger Details: • Merger took place in June 2007. • LSE acquired BorsaItaliana for EUR 1.63 billion. • BorsaItaliana Group included the equities stock exchange (BorsaItaliana), the government bond exchange (MTS), the clearinghouse/CCP – CCG and the CSD – Monte Titoli. • Companies remain as separate legal and regulatory entities. • The listing of 79.5 million new shares in London Stock Exchange Group plc was published on 25 September 2007. • LSE Group also owns Turquoise – an MTF. • LSE Group is currently in the process of acquiring LCH.Clearnet.

LSE – Borsa Italiana LSE – BorsaItaliana BI-Trades LSE Trades

LSE – Borsa Italiana • Implications for market infrastructures: • Borsa Italiana had to introduce Tradelect following the merger and will now introduce Millenium IT, which could be expensive for the exchange and brokers. • CCG and Monte Titoli in stand by for three years while other markets in Europe were developing fast • Had to adjust to LSE’s company policies • No major changes to clearing and settlement procedures

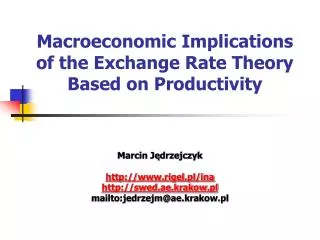

Case Study MICEX – RTS Merger

MICEX - RTS Merger Details: • Merger agreement signed in May 2011. • RTS shares (including preferred shares) were valued at RUB 34.5 billion; while MICEX shares were valued at RUB 103.5 billion;. • Both MICEX and RTS are vertical silos. MICEX Group includes the stock exchange (MICEX), the clearing house and CCP (NCC) and the depository (NSD). RTS Group includes the stock exchange (RTS), the cash settlement bank and clearinghouse (RTS Settlement Chamber) and the securities depository (DCC). • Clearance from Federal Anti-monopoly Service (FAS) was obtained in September 2011 . • Merger expected to be completed in 2012. • An IPO is expected in 2013.

MICEX - RTS MICEX - RTS Pre-Merger Arrangements

MICEX - RTS MICEX - RTS Post-Merger Arrangements

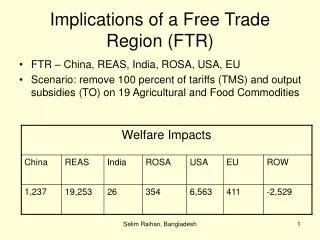

Case Study MILA Alliance

Integration Details: • Agreement signed by the three stock exchanges and the three CSDs in September 2009. • Securities market regulators from Chile, Colombia and Peru sign MoU to harmonise regulations in order to launch MILA. • Each depository opens an account at the other two CSDs in order to settle securities traded through MILA. • MILA is launched in November 2010. • MILA starts operations in May 2011.

MILA MILA Arrangements Chile Colombia Peru

MILA Implications CAVALI DCV DECEVAL

Conclusions • The implications of the exchanges merger on post-trade infrastructures may vary depending on the type of merger (cross-border or in-country) and the market conditions (i.e if there is vertical integration or not). • In general, CSDs are less affected by merger exchanges if they part of a vertical silo. • In the case of LSE with Borsa Italiana, have not been any changes to the post-trade processing, but Borsa Italiana had to adjust some of its policies to LSE’s policies and stayed on hold for three years while other markets developed. • In the case of MICEX and RTS, it is expected that the exchanges will continue running separate trading systems for some time (not known yet) but consolidation at the post-trade level is expected to take place sooner. NSD is expected to become the CSD in Russia and take over the operations from DCC. • In the case of MILA, the post-trade processing has not changed. There were several operational and legal changes required for the CSDs in order to support the exchanges’ integration.