Download

1 / 15

150 likes | 234 Views

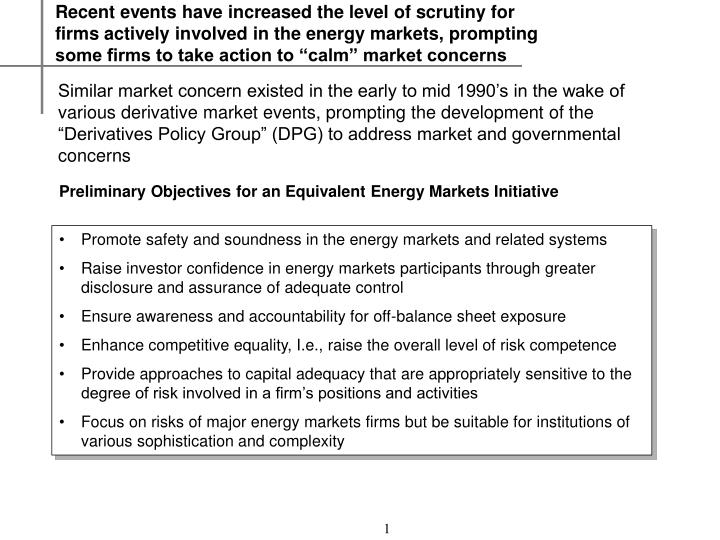

Recent events have increased the level of scrutiny for firms actively involved in the energy markets, prompting some firms to take action to “calm” market concerns.

E N D

Recent events have increased the level of scrutiny for firms actively involved in the energy markets, prompting some firms to take action to “calm” market concerns Similar market concern existed in the early to mid 1990’s in the wake of various derivative market events, prompting the development of the “Derivatives Policy Group” (DPG) to address market and governmental concerns Preliminary Objectives for an Equivalent Energy Markets Initiative • Promote safety and soundness in the energy markets and related systems • Raise investor confidence in energy markets participants through greater disclosure and assurance of adequate control • Ensure awareness and accountability for off-balance sheet exposure • Enhance competitive equality, I.e., raise the overall level of risk competence • Provide approaches to capital adequacy that are appropriately sensitive to the degree of risk involved in a firm’s positions and activities • Focus on risks of major energy markets firms but be suitable for institutions of various sophistication and complexity

Significant benefits will accrue to the companies which seize the opportunity in this self regulatory initiative • Improved Investor Perception: Create positive investor perception increasing desirability for investing in the company • Lower Capital Cost: Greater ease in accessing the capital markets at lower cost • Improved Credit Ratings: More favorable perceptions from the rating agencies leading to improved rating or growth opportunities associated with excess capital • Reduced Undesirable Public Scrutiny: Investor, rating agency and regulatory scrutiny will be diverted to less leading edge firms • Greater Market Stability: Creates a more stable and consistent playing field for all market participants, e.g., credit is consistently recognized as a cost associated with doing business • Increased Business Opportunity: Market will perceive company as being a more desirable counterparty, increasing its market share of profitable deals • Reduced Need for Credit Margining: Ensuring high standards for risk management and market intermediation for market participants will facilitate the creation of a clearing consortium freeing up additional capital

The Derivatives Policy Group (DPG) was formed as a result of public concern over unregulated OTC derivatives activities Overview of Participation and Framework Regulatory Involvement Group of Six Chairman of SEC (Arthur Levitt1) Chairman of CFTC ( Mary Shapiro1) Morgan Lehman First Boston Merrill Goldman Salomon Compliance Required Independent Verification and Best Practice Approaches Framework was Voluntary and Rigorous • Voluntary framework targeting risk management practices and OTC derivatives • Focuses on • Capital adequacy: evaluation of market and credit risks in relation to capital • Governance and controls: oversight, monitoring and measuring of activities and risk; standards for professional intermediaries • Disclosure and reporting: confidential SEC and CFTC quantitative reports addressing positions and related risks • Institutions adopt DPG Framework by defining details in “Authorizing Guidelines” • Attestation of compliance by independent auditors • Periodic private disclosure to SEC / CFTC • Compliance requires high level of sophistication, e.g., best practice approaches 1 – Arthur Levitt of the SEC and Mary Shapiro of the CFTC were the head of their respective organizations at the DPG’s inception in 1994

The DPG framework was devised based on several key and interrelated factors DPG Key Factors • Is an ongoing process not a one time event • Continuing evolution of policies and practices: Framework will be refined and adapted to evolving market conditions • Set standards for being a professional market intermediary • Built based on critical interrelated components: Capital, Process and Control, and Disclosures • Sensitive to the competitive environment in which the group of six participated DPG Framework Capital Adequacy Governance, Process and Control Reporting and Disclosure • Meet standards of professional intermediary, e.g., credit worthiness, supervision, controls, record keeping, appropriate skills • Process and controls for timely monitoring/ measuring risks • Established process for managing exceptions from risk guidelines and assessing materiality of impact • Timely access of position and risk data • External audit and verification process • Guidelines for establishing market risk limits • Independence of monitoring/measuring of risk • Senior management involvement in risk management process • Capital adequacy must be ties to levels of market and credit risk • Capital measurement models must meet minimum standards: • - Capture material sources of risk • - Provide capital at risk and results of • various scenarios • - Credit capital based on current and • potential exposures • Submit periodic reports to SEC & CFTC • New quantitative reports covering credit name and concentration exposures • Consistent measure of risk reporting • Enable SEC & CFTC to make informed assessments

Each “Group of Six” company defined specific guidelines consistent with the framework, which are independently verified DPG Governance and Management Model SEC/CFTC Group of Six and “Regulators” DPG Framework Individual Company Board of Directors/Risk Committee Firm Specific Authoritative Guidelines External Audit Business Unit Self Assessment Risk Committee and Risk Management Group Agreed Upon Procedures Exceptions and Exemptions Management Assertions Examination Opinion Internal Audit Confirmation of BU Assessment • Policies and Controls • Capital adequacy and validation

The DPG framework was defined within six months, and key elements implemented during the following year Key Events and Milestones Market concern of unregulated OTC derivatives >1996 <1994 1994 - 1996 • First Boston withdrew from G6 after merger with Credit Suisse • Various aspects of DPG used to suggest best practice and influence regulatory requirements • Glass Stegal Reform Act • Derivative losses & scandals increases market concern • Bankers became aware of need to • act • Establish and Implement DPG DPG Key Events & Milestones 1994 August 1995 January March June October 1996 January • DPG formed at the suggestion of Chairman Arthur Levitt of the SEC in August, 1994 • Work begins on the creation of framework • Initial “Framework for Voluntary Oversight” is completed • Initial work begins at G6 companies to comply • Initiate comprehensive review of management controls in relation to guidelines • Credit and market risk filings provided to SEC and CFTC • Audit report addressing risk in relation to capital provided to SEC and CFTC • First annual audit verification of compliance with DPG guidelines Initial Enhanced Disclosure Capital Adequacy Compliance Initial Audited Compliance Formulation Stage Assessment Development and Implementation

Key lessons from the DPG experience can be applied to the energy markets Lessons Learned • Limited window of opportunity to react and favorably influence process, i.e., act quickly and decisively • Response must be sufficient and significant, i.e., significant market share addressed by the right participants (represent significant market share) • Participants should not be exclusionary, i.e., need to include large participants not necessarily viewed favorably in market • Framework should be rigorous and focused on the market concerns • Approach must be taken seriously by all firms, i.e., not just a press release • Involvement of senior management • Commitment to invest where capabilities are lacking • Agreement to run the firm by the DPG Framework and principles • Clearly defined scope and objectives to address the “hole”, e.g., DPG concern was unregulated OTC derivatives

While much can be borrowed from DPG, critical differences need to be considered while devising the overall approach for energy Financial Markets (DPG) Energy Markets Differences: “Hole” was well defined as unregulated OTC derivatives • “Hole” not localized: • Limited off balance sheet disclosure • Involvement in energy markets • Trading against limited assets • Limited enterprise risk integration Concern of making participants less competitive Required to make participants competitive Similarities: Narrow window of opportunity Concern over pending regulation Perception problem with investment community Precipitated by market events Despite narrow scope of DPG concern, framework was applied by companies across many or all activities

A strategy to develop an equivalent policy group for energy markets needs to be defined Key Strategy Development Questions • Who should participate in this group? • What regulators should participate in the process? • What role should various regulatory bodies play in its development and deployment? • What are the key short and long term milestones to establishing this group? • What are the key steps necessary to establish this group?

Major energy and financial firms with significant market share should be participants • Risk Management & Market Sophistication • Willingness to invest • Selection Criteria: • Positive Market Perception for some leading participants • Large Market Share Major Energy Market Players and Potential Participants: • Top Power Traders1 • AEP • Duke • Mirant • Aquila • Reliant • Williams (15-Gas) • Dynegy • El Paso • PG&E • Constellation • Top Natural Gas Traders2 • Reliant • AEP • Duke • Mirant • BP (14-Power) • Aquila • Dynegy • Sempra (26-Power) • Coral (22-Power) • El Paso • Largest Energy3 • ExxonMobil • Royal Dutch/Shell • BP • ChevronTexaco • Duke Energy • El Paso • AES • Exelon • Conoco • Williams Largest Non-Energy1 Morgan Stanley Merrill Lynch 1 – Power Markets Week, Mar 25, 2002 2- Natural Gas Week, Nov 19, 2001 3- Active in US Markets, Business Week, Jul, 9, 2001

While a critical goal of this self regulatory structure would be to address market and investor concerns, appropriate regulatory bodies need to be brought into the process Regulatory Involvement Assessment Process Involvement Seek Framework Guidance Communicate Intentions External Involvement Rational Regulatory Bodies: SEC CFTC FAS FERC Local PUC/PSC’s Non-Regulatory: Rating Agencies Analysts/Investors • Oversees disclosure for all public companies • Involved in DPG process • Oversees exchange commodity trading activity • Involved in DPG process • Experience with reporting disclosure • Framework should incorporate upcoming revisions • Already focused on regulated parts of business • Limited insight into market/credit risk mgmt • Focused on regulatory issues at local level • Awareness of framework will provide educational benefit • Would want to incorporate elements that lead to more favorable ratings assessments • Awareness to promote transparency of performance, and sources of risk Highest InvolvementLowest 1 – Source???

An equivalent group of companies involved in the energy markets should establish milestones Potential Milestones • Near-Term: • Develop goals • Define participant criteria and guidelines • Define framework outline • Long-Term: • Define reporting and disclosure standards • Develop and implement framework • Identify independent attestation criteria

Creation of the appropriate group of companies and beginning discussions with regulators are critical next steps Key Next Steps • Establish group of appropriate and interested market participants • Define desired role and interaction with regulatory bodies • Begin senior level dialogues between companies and regulatory bodies with a focus on • - Establishing the scope of activities to be addressed • - Determining the desired outcome • Establish working teams within the companies and regulatory bodies to establish framework for capital determination, process and control, and enhanced public and confidential disclosure • Communicate intentions and milestones of group for addressing market concerns and issues

Deloitte & Touche can provide assistance in several ways • Develop Consortium White Paper • Rationale • Who would gain • What the downside is for not participating • Success factors • Straw model for consortium • Next steps • Assist in determination of a company’s value proposition • First mover and prime founder status • Market and regulatory intelligence and preference discovery • Create key component of a company’s corporate risk preparedness plan • Develop initiating communication plan • Presentations • Invitations • Facilitations • Assistance for individual companies • Readiness assessment • Development planning • Implementation assistance • Independent attestation of compliance

Voluntary Regulatory Framework for the Energy Business May 21, 2002