Download

1 / 18

180 likes | 306 Views

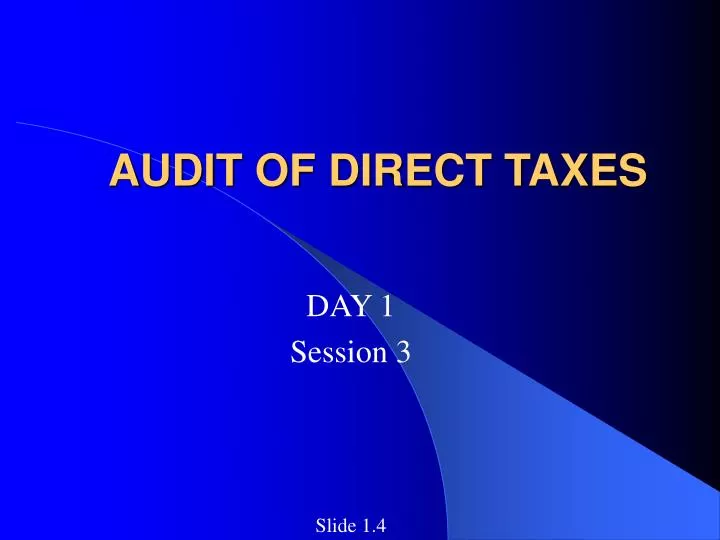

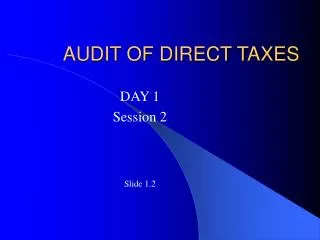

AUDIT OF DIRECT TAXES. DAY 1 Session 3 Slide 1.4. INCOME TAX DEPARTEMENT WEST BENGAL. CHIEF COMMISSIONER NoS-13. CIT/DIT RTI. DGIT INVESTIGATION. DGIT EXEMPTION. COMMISSIONER NOS-26 (Asst. Charges). CIT (AUDIT). CIT CENTRAL Nos-3. DIT INVESTIGATION (KOL,BHUB, GUAHATI).

E N D

AUDIT OF DIRECT TAXES DAY 1 Session 3 Slide 1.4

INCOME TAX DEPARTEMENT WEST BENGAL CHIEF COMMISSIONER NoS-13 CIT/DIT RTI DGIT INVESTIGATION DGIT EXEMPTION COMMISSIONER NOS-26 (Asst. Charges) CIT (AUDIT) CIT CENTRAL Nos-3 DIT INVESTIGATION (KOL,BHUB, GUAHATI) DIT EXEMPTION CIT/DIT FT CIT CIB CIT (APPEALS) Nos-48 CIT (COMPUTER OPERATIONS) Add. CIT/JCIT (RANGE-CENTRAL) Total Nos-6 Add.CIT/JCIT (INVESTIGATION) UNITS-4 Nos Add. CIT/JCIT (RANGE) NoS-3 SECRETARY (SETTLEMENT) AC/DCENTRAL CIRCLE Nos-4 TO 7 AC/DC INV. UNIT Nos-4to5 MEMBER (APPROPRIATE AUTHORITY) NoS-2 AC/DC DIT (SETTLEMENT COMMISSION) ITO CIT JUDICIAL DIT (VIGILANCE) ITO CIT ITAT Nos-4 ITO DIT (SC-DR) Nos-2 ITO CIT (TDS) TRO

Filing of Income Tax Returns by the assessees Assessment of the Returns by the Assessing Officer of the Income Tax Department Assessment Order Audit of the Assessment Orders by the Revenue Audit Parties of ITRA wing LOCAL AUDIT REPORT (LAR) for the Assessment Unit Audit Para Yes No No Further action on the case Objections Found Submitted To ITRA HEADQUARTERS F1: A Simplified flow diagram explaining the genesis of a paragraph and the Local Audit Report (LAR)

Object of Receipt Audit • The main object of Receipt Audit is to satisfy itself that the Income-tax Department has provided sufficient checks and safeguards against errors and fraud, and that the procedures prescribed are calculated to give effect to the requirements of law Slide 1.4

Function of Receipt Audit • An important function of Receipt Audit is to see that adequate regulations and procedures have been framed by the Department to secure an effective check on the assessment, collection and proper allocation of taxes and to satisfy itself that such regulations and procedures are, in fact, being observed. Slide 1.4

Aspects of Receipt Audit Scrutiny 1. The general circulars or instructions of CBDT, or its orders in specific cases, may be seen as to whether such orders are in accordance with the plain meaning of law. Similarly notifications issued by the CBDT may be scrutinised to check if they are issued under proper authority of law. Slide 1.4

Cont… 2. The quasi-judicial orders of the CsIT under section 263 and 264 of the I.T. Act and corresponding provisions of the other direct tax laws, may be seen to check any patent misinterpretation of law or any general departure from the plain meaning of law. Similarly, orders passed under section 273A of the IT Act and Section 18B of the Wealth-tax Act may, in addition, be seen to ensure that they are in conformity with the CBDT’s Instructions. Slide 1.4

Cont… 3. Penalty orders passed by Commissioners and other instructions issued by them to ITOs may also be seen to check if they are in conformity with the provisions of law and the department instructions. 4. Appellate orders may be brought into questions only if they raise a general issue wherein Appellate Authorities view is against the plain meaning of law or against the procedure that has been followed on the basis of authoritative decision of the Government or a court of law. Slide 1.4

Cont… 5. In regard to Assessing Officer’s assessment work, Receipt Audit would see:- a. Whether the assessment made is in accordance with the provisions of the Government, the Finance Act and the Rules framed under the Act. b. Whether the procedures prescribed by the CBDT/CIT have been followed ; and c. Whether the instructions or orders issued by the higher authorities i.e. the CBDT, the D.I., the CIT, the IAC have been complied with. Slide 1.4

Cont… 6. Receipt Audit would also scrutinise orders passed by Assessing Officer’s in other ancillary proceedings regarding advance tax, re-assessment, provisional assessment, rectification, appeal effect, registration of firms, penalty, refund, relief u/s. 89 of I.T. Act etc 7. In regard to collection of taxes, Receipt Audit would verify that the same are duly recovered and are shown as such against corresponding demands and are credited to the proper Head of Account Slide 1.4

Cont… 8. Receipt Audit will also test check entries in the Registers maintained by the Income-tax Department with a view to seeing that no irregularities occurred in assessment, collection and adjustment of taxes due to improper maintenance or failure to keep the prescribed Registers 9. Receipt Audit will also see cases earlier checked by the Internal Audit Parties/ Special Audit Parties to verify the effectiveness of Department’s Internal Audit. Slide 1.4

Cont… 10.Receipt Audit will also point out cases of over assessment as readily as cases of under assessment, since over-assessments also constitute an irregularity and departure from the plain provisions of law. 11.Receipt Audit would also audit files relating to Acquisition proceedings.However, such audit will be taken up only with the prior approval of the DAG/Sr.DAG and the objections, if any, would be raised only if the DAGs/Sr.DAGs are satisfied, and under their signature only. Slide 1.4

Cont… 12. The procedure in respect of the Audit of cases completed under the Summary Assessment Scheme has been revised by the C&AG , which was communicated by the Board vide its D.O. Letter F.No. 237/5/84-A&PAC-II dated 18.4.86 and was circulated by the DI(A) to all CsIT vide Circular dated 29.4.86. Henceforth, consolidated reports regarding audit objections on Summary Assessment cases would be communicated to the concerned CsIT every 6 months and an Annual Report would be sent to the Board. Slide 1.4

Types of Audit Reports Two types of Audit Reports in the area of audit of Direct Taxes. They are: - 1. Audit Report reflecting the results of local test audit of assessment and other records of the income tax department (AR No.12) 2. Report of the Systems appraisals (AR No.13)(previously 12A) Slide 1.4

Audit approach The audit approach involves examination of – a. Assessments through test check b. Rationale for issue of instructions and circulars c. Decisions taken in particular cases and d. Efficacy and adequacy of systems and procedure of tax collection, appeals and overall tax administration. Slide 1.4

Cont… The audit approach in this regard usually involves: - a. Collecting / preparing data base for each subject b. Selection of sample/s for test checks (both units and assessments) c. Exercising audit checks intelligently d. Communicating audit observations to assessing officers e. Consolidating audit findings f. Forwarding the same to the Direct Taxes Wing along with prescribed ‘key’ documents Slide 1.4

CAG’s AUDIT REPORT • Direct Taxes wing of the Comptroller and Auditor General of India has over the last 10 years commented upon • deficiencies in tax laws and • also in tax administration in the form of special studies or system appraisals / reviews covering about 45 subjects in the Audit Reports. Slide 1.4

Cont… • Early and effective planning, timeliness, accuracy of data, adequacy of coverage and correctness of audit findings are crucial to successful completion of the systems appraisals. Slide 1.4

![OVERVIEW OF FINANCE BILL, 2010 [DIRECT TAXES ONLY]](https://cdn3.slideserve.com/7062934/overview-of-finance-bill-2010-direct-taxes-only-dt.jpg)