Download

1 / 15

E N D

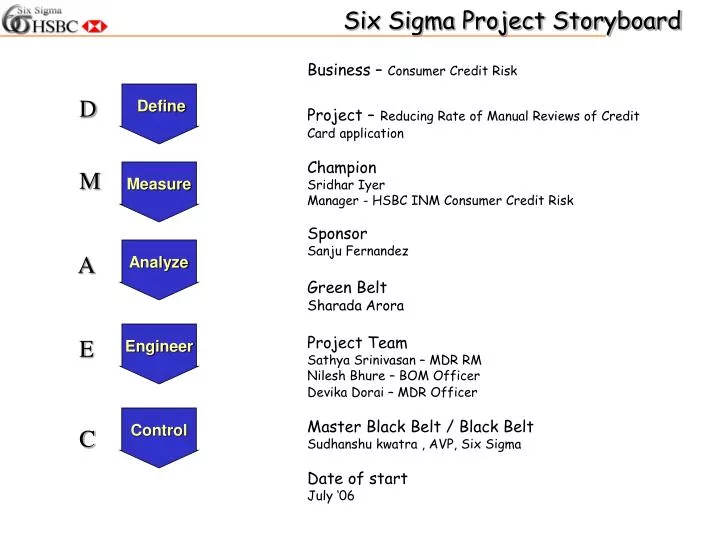

D M A E C Six Sigma Project Storyboard Business –Consumer Credit Risk Project –Reducing Rate of Manual Reviews of Credit Card application ChampionSridhar IyerManager - HSBC INM Consumer Credit Risk SponsorSanju FernandezGreen BeltSharada AroraProject TeamSathya Srinivasan – MDR RMNilesh Bhure – BOM OfficerDevika Dorai – MDR OfficerMaster Black Belt / Black BeltSudhanshu kwatra , AVP, Six SigmaDate of startJuly ‘06 Define Measure Analyze Engineer Control

D M A E C What and why we need to do it now… Question to ask ! Are we (people & systems) geared up for this volume surge ? 2006 – End Monthly CC apps – 100,000 Total Cards Base – 2 M Manual Rate – 75% FTE’s Involved – 20 Approval Rate – 44.91% B&D Ratio – 4.5% 2007 – Beyond.. Monthly CC apps – 200,000 Total Cards Base – 1 M per year Manual Rate – 75% FTE’s Involved – 26… Approval Rate – 44.91%… B&D Ratio – 4.5% 2006 – August Monthly CC apps – 77,000 Total Cards Base – 1.5 M Manual Rate – 75% FTE’s Involved – 16 Approval Rate – 44.91% B&D Ratio – 4.5% Benchmark - - - - ICICI bank is working on a model where 85% of Credit Card apps are actioned straight through… Intelligent Decisioning !!!! Six Sigma Deployment Six Sigma Project Challenge : Real success of the project will be if we can reduce manual review rates while keeping the Bad debt % at levels at start of the project and ensure approval rate does not drop.

D M A E C Business Case:Credit Card is a growing business with '06 AOP target of 2 M cards from the current of 1.55 M. Benchmarking study shows that top banks like ICICI have moved to a automated model of Credit Card review process to handle surge in volumes though their delinquency % remains a bit higher than the market average.To meet the aggressive target of 2 M cards and keeping the operation cost within limits it becomes imperative in finding a suitable solution to optimize credit card app. manual review rate without negatively affecting the B&D ratio and approval rate Problem Statement:On an average 90,000 CC apps are sourced/month of which 68,000 apps go through manual review. MR is done for 75% of the total apps sourced. Project Goal:Reduce % of manual review of credit applications by 25% from the current of 75% (75-25) keeping B&D within agreed AOP limits (13.5% of receivables as per AOP ‘06) and current approval rate of 44.91% (Or the prevailing approval rates) • Start Point : Credit Card application received by customer by mail or in digital format • End Point – Quality check of manual review applications Project Scope Define – 21th Aug ’06 Measure – 25th Aug ’06 Analyze – 25th Sep ’06 Engineer – 30th Nov ’06 Control – Mar ‘07 Primary Metric - % of MR Secondary Metric –B&D ratio Estimated $ Benefit • Benefit : $ 200,000 • Reduction in TAT : 1 Day • Reduction in Error % - 1% Secondary Metric –Approval rate Output Process Supplier Input Customer CC Applicant, Satyam Infoway DSA’s/ DSF’s Credit Card Application CC application submitted to DSF Accepted / Rejected CC app Credit Card Welcome Kit Credit Card Applicant DSF submits to DSA. DSA Courier’s to TBS Chennai Data Entry done by TBS Application checked against Compliance policy. Verifications are initiated Verification outcome is posted on a grid, grid result is posted on FEPS Application is either rejected / approved / referred Apps referred go to MR review desk App is accepted / rejected

D M A E C Measure Summary Unit of Measurement As Is Process Map : Output – Credit Card Application Status Accepted/Rejected Unit – Each Credit Card Application received at TBS Sample Size : Specifications / Defect Definition Metric is Rate of manual review Frequency - Daily Spec limit - 50% Unit - Each day Opportunity - 1 per unit or 1 per day Defect - Any day the MR rate exceed 30% (As either that day will have MR rate higher than 30% or lower than 30%, making that unit defective or not) Current Process Capability : Operational Definition Manual Review Application – Any credit card application Which does not get approved directly through SW system and goes through Manual review desk(Manual intervention) Attribute Gage Study : GRR not required as Manual Review count / processing is Pulled / done on SW(Strategy System) automated System. > Short Term DPU Sigma – -3.39 DPU > DPMO – 999,997 > Mean – 75% > Std Dev – 5.45 > USL – 50% > Normality – Data is normal > N – 52 (Sample Size)

D M A E C Analyze Summary Potential X’s identified through root cause analysis : • Compliance declines • SE • UV • SEUV • Exception hits with SE&UV • Exception Hits without SE or UV • Exception hits with only UV • Exception hits with SE Pareto analysis to be done to identity critical X’s

D M A E C Exception hit top categories : Strategy Ware(SW) rule top categories : Exception hit with SW top categories : SE-EH-SW top categories : SE-UV-EH-SW top categories : UV-EH top categories : Analyze Summary

D M A E C Analyze Summary EH-SW top categories : SE-EH top categories : SE-SW top categories : SE-UV-EH top categories : Top 18 MR categories contributes 53% of total reasons for app going to Manual reviews

D M A E C Engineer Summary 23% reduction in MR % 3% of Apps Compliance declines > BPO/Call Centre applicants can be sourced only under ‘OBC/OBL’ surrogate. Else Income documents with Income >5 Lakhs p.a should be submitted (irrespective of the designation) > No visiting card sourcing allowed. b.) Profile: Clerical cadre > Govt. Clerical only with OBC/OBL in Bangalore, Chandigarh, Chennai, Cochin, Indore, Calcutta, Mumbai, Jaipur and Pune. Profile: Sales Designations > In Mumbai, Delhi, Bangalore and Pune All Sales Profiles (TC & Non TC) with income >= 4 lakhs p.a can be sourced with Income docs. > For other cities all Sales Profiles (TC & Non TC) with income >= 2.5 Lakhs p.a can be sourced with Income docs. 6% of Apps • Exception hits • Following value need to be coded in Overdraft O/s of DG13 screen, to decline the applications which are duplicates or blacklist match or Not OK for second HSBC cards. • 40000- To decline applications where it is match with HUB Blacklist • 50000- To decline duplicate applications from same DSA • 60000- To decline duplicate applications from different DSA • 70000-To decline duplicate applications from different sources • 26000-To decline existing card which does not meet the Second Card Issuance Policy 12% of Apps • Exception hit with UV, SEUV and SE &UV • Code entered in Loan Monthly installment field before verification ; • 81000- To decline applications where designation mismatch between application and verification report. • 82000- To decline applications where there mismatch in address between application and verification report. Coded SW(Strategy Ware) system with certain codes using existing (blank) fields on the system to decline applications directly by the system !!!

D M A E C Engineer Summary Improve – Pilot results

D M A E C Control Summary Pre Improve – Process Capability / Process Distribution Post Improve – Process Capability / Process Distribution Pre Improve – Individual & Moving Range chart ( MR% daily) Post Improve – Individual & Moving Range chart ( MR% daily)

D M A E C 44% 44% 44% Approval % 999,997 631,479 499,998 DPMO 75% 53% 50% MR % Baseline Target Achieved Control Summary Graph shows comparison of total CC applications processed Vs daily MR% (Post improve) Vs Approved % Project Performance – Baseline Vs Target Vs Achieved Six Sigma Benefit - -$180,000

Establish CTQ Characteristics Project Scope & Elevator Speech In Scope • Manual Review desk • Any system changes on SW (Strategy Ware)system • Desk involved upstream Out of Scope • Desk involved post Manual Review desk • Change in Bank Policies for Credit Cards • PIL Processing desk Elevator Speech On an average 90,000 credit card applications are processed in a month of which 66,000 applications goes through manual review. Manual Review is done for 75% of the total application processed. Target of the project is to reduce/optimize Manual Review % by 25% thereby bringing down the overall % of applications going through manual review to 50%

Establish CTQ Characteristics Arriving at the Internal CTQ CTQ Drill Down Tree – Reduce / Optimize rate of manual reviews of credit card application process Business CTQ Customer CTQ Project CTQ Process CTQ Reduction in manual intervention Automation / Low Operations Costs Reduction in Operational cost Faster processing of Credit card applications Operational cost reduction & optimize rate of manual reviews Reduction in rate of manual reviews of CC applications Quicker TAT for customer’s Streamlined Process / Reduced work load General Specific

Target Validation Target of 50% reduction is statistically valid as P value < 50%