Download

1 / 12

120 likes | 202 Views

By: Tyler Gowans, Andro Batinic , and Josh Clark. Home Buying Case Study. John Berka. Credit Score: 551 Assets: $1,200 in checking $4,050 in savings $5,000 in CDs (4.9%) $89,000 in 403(b) plan $26,482 in an IRA $ 18,000 in his car

E N D

By: Tyler Gowans, AndroBatinic, and Josh Clark Home Buying Case Study

John Berka • Credit Score: 551 • Assets: $1,200 in checking $4,050 in savings $5,000 in CDs (4.9%) $89,000 in 403(b) plan $26,482 in an IRA $18,000 in his car $15,028 in 3 growth mutual funds $190,000 in his house $50,000 in personal property • His total net worth is $353,760.

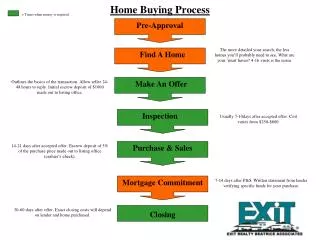

Liabilities: $45,000 in debt Monthly expenses average $4,000 Mortgage payment is $1,228 Car payment is $529 Monthly child support of $420 He also deposits $650 in his 403(b) monthly • He has no will and a $250,000 term life policy that still names his deceased wife as the beneficiary. • Based on his assets and liabilities John can afford a monthly payment ranging from $1,750-$2,450

Housing Option #1 Pros and Cons Pros: Walking distance to “best areas of the city”, owners remodeled the home and replaced most of the problems in the home that come with age. Cons: Built in 1912, commute to work could be long.

Housing Option #2 Pros and Cons Pros: Small, meets John’s needs, affordable, easy commute. Cons: Older building (built in 1940), small

Housing Option #3 Pros and Cons Pros: Easy commute Cons: No information on website, Expensive for John’s needs.

Housing Option #4 Pros and Cons Pros: Affordable for John’s current situation, privacy, safety, jetted tub, built in 2001, very low crime rate (we checked), he could pay for a large portion of it just by selling the place he is in now. Cons: John doesn’t need that much space.

Buying Housing Option #4 • Down Payment: $33,180 – if he sells his house he is currently living in (worth $190,000) he would have enough for the down payment plus some. • Maximum Mortgage John could qualify for would be around $300,000 based on a 30 year fixed with an option to refinance once his credit score increases.

Needs and Wants • Needs: Shelter, Privacy, and Safety. • Wants: Jetted Tub, 4 bedrooms and 4 bathrooms, low crime rate.

Paying it off • If he pays the minimum monthly payment of $1,217.32 John will pay the house off in 30 years unless he decides to refinance. • The total John would pay in interest is $10,617.60

Conclusion • The best choice for John would be to stay in the house he is currently residing in since the home is already close to being paid off. • John would be likely to live there until retirement age where he could move into a retirement community.