Download

1 / 0

0 likes | 126 Views

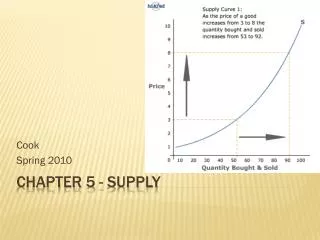

Chapter 5 SUPPLY. I. WHAT IS SUPPLY?. The energy crisis of the 1970s encouraged countries to look to nuclear reactors, fueled by

E N D