Download

1 / 37

370 likes | 542 Views

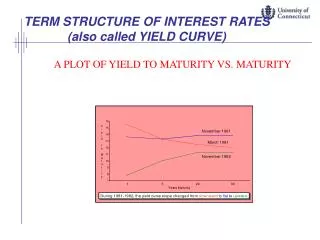

Chp.19 Term Structure of Interest Rates. 报告人:陈焕华. 2012 年 12 月 19 日. Main Contents. Some Basic Definitions; Yield Curve and Expectation Hypothesis; Term Structure Models-A Discrete Time Introduction; Continuous Time Term Structure Models; Three Linear Term Structure Models; Some Comments.

E N D

Chp.19 Term Structure of Interest Rates 报告人:陈焕华 2012年12月19日

Main Contents • Some Basic Definitions; • Yield Curve and Expectation Hypothesis; • Term Structure Models-A Discrete Time Introduction; • Continuous Time Term Structure Models; • Three Linear Term Structure Models; • Some Comments

Definition and Notation • Bonds: • Zero-Coupon Bonds(the simplest instrument): • Coupon Bonds : portfolio of zero coupon bonds. • Bonds with Default Risk: such as corporate bonds. • In this chapter, we only study the bonds without default risk. And since coupon bonds can be regarded as portfolio of zero-coupon bonds, the main research is done to zero coupon bonds.

Zero Coupon Bonds • Price: • Log price: • Log yield: • Log holding period return: • Instantaneous return: • Forward rate: • Instantaneous forward rate:

Some proof(1) Log yield:the yield is just a convenient way to quote the price • Or

Remark • Holding Period Returns

Some proof(2) • Instantaneous return: • Remark: hpr is the time value, dP/P is the total value, the second item in right equation is the term value. Total value equals the time value plus the term value.

Some proof(3) • Forward rate: • Consider a zero cost investment strategy: • Buy one N-period zero ; • sell N+1 period zero. • The cost is zero. • The payoff is 1 at time N, and at time N+1;

Some proof(3) According to no arbitrage condition,

Some proof(4) • Instantaneous forward rate:

Some extensions Forward rates have the lovely property that you can always express a bond price as its discounted present value using forward rates,

Some extensions Since yield is related to price, we can relate forward rates to the yield curve directly. Differentiating the definition of yield y(N , t ) = −p(N , t)/N

Log(Net) return: consistent • EH1: • EH2: • EH3: • When risk premium equals zero, this is PEH.

Proof of consistence(1) • By EH(1) and suppose risk premium is zero, • By EH(3),

Proof of consistence(2) • By EH(2),

Level (Gross) Return: Self-contradiction • EH(1): • EH(3):

Discrete Time Model • Term Structure Models: • specify the evolution of short rate and potentially other state variables. • The prices of bonds of various maturities at any given time as a function of short rate and other state variables. • A way of generating term structure model: write down the process for discount factor, and prices of bonds as conditional mean of the discount factor. This can guarantee the absence of arbitrage.

Properties of the Term Structure Properties of the Term Structure Chen, Huanhua Dept. of Finance, XMU

Other term structure model • Model yields statistically. • Run regressions; • Factor analysis. • Trouble: reach a conclusion that admits the arbitrage opportunity, which will not be used for derivative pricing. • Example: Level factor will result in the co-movement of all yields. This means the long term forward rate must never fall.

a model based on EH • Suppose the one period yield follows AR(1), • Based on EH(1), • Remark: not from discount factor and may not be arbitrage.

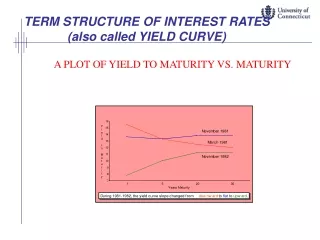

implications • If the short rate is below its mean, • Long term bond yields are moving upward. yield curve is sloping upward. • If the short rate is above its mean, we get inverted yield curve. • The average slope is zero. • But we can not produce humps or other interesting yield curve.

Implications(2) • All bond yields move together.

Implication(3) • AR(1) may result in negative interest rate.

Direction for generalization • More complex driving process than AR(1), such as hump-shape conditionally expected short rate and multiple state variables. The short rate should be positive in all states. • Add some market price of risk to get average yield curve not to be flat. • Term structure literature: specify a short rate process and the risk premium, and find the price of long term bonds.

The Simplest Discrete Time Model • Log of the discount factor follows AR(1) with normal shocks. • Log rather than level so that the discount factor is positive to avoid arbitrage. • Log discount factor is slightly negative. • Unconditional mean

An example • Consumption-based power utility model with normal errors:

Remark • It is not a very realistic term structure model. • The real yield curve is slightly upward. this model gets the slightly downward yield curve if the noise term piles up. • This model can only produces smoothly upward or downward yield curve. • No conditional heteroskedasticicy. • All yields move together, one factor and perfectly conditionally correlated. • Possible solution: more complex discount factor process.

Thank you for listening andComments are welcome. 2012年12月19日